DHL

17

min read

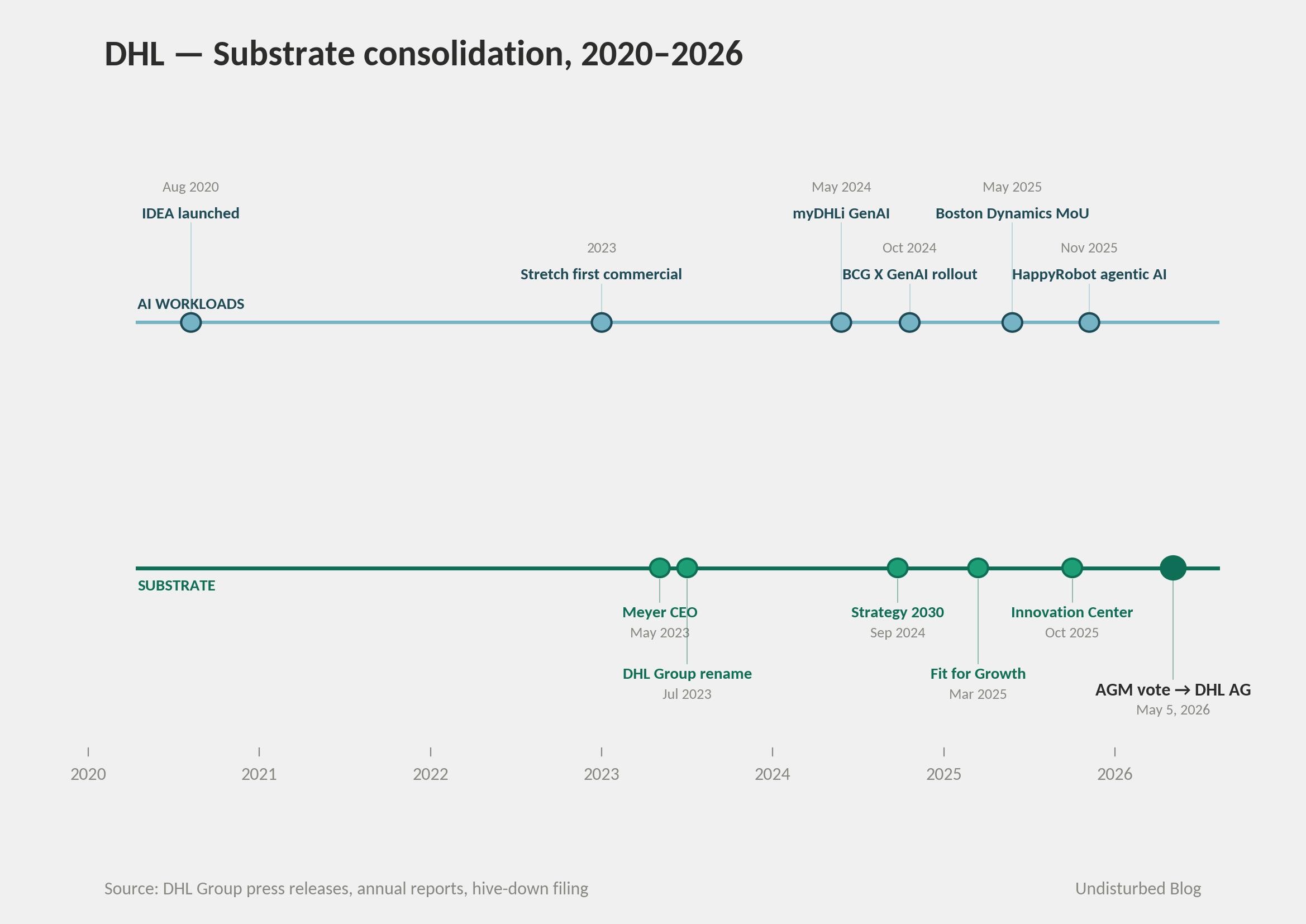

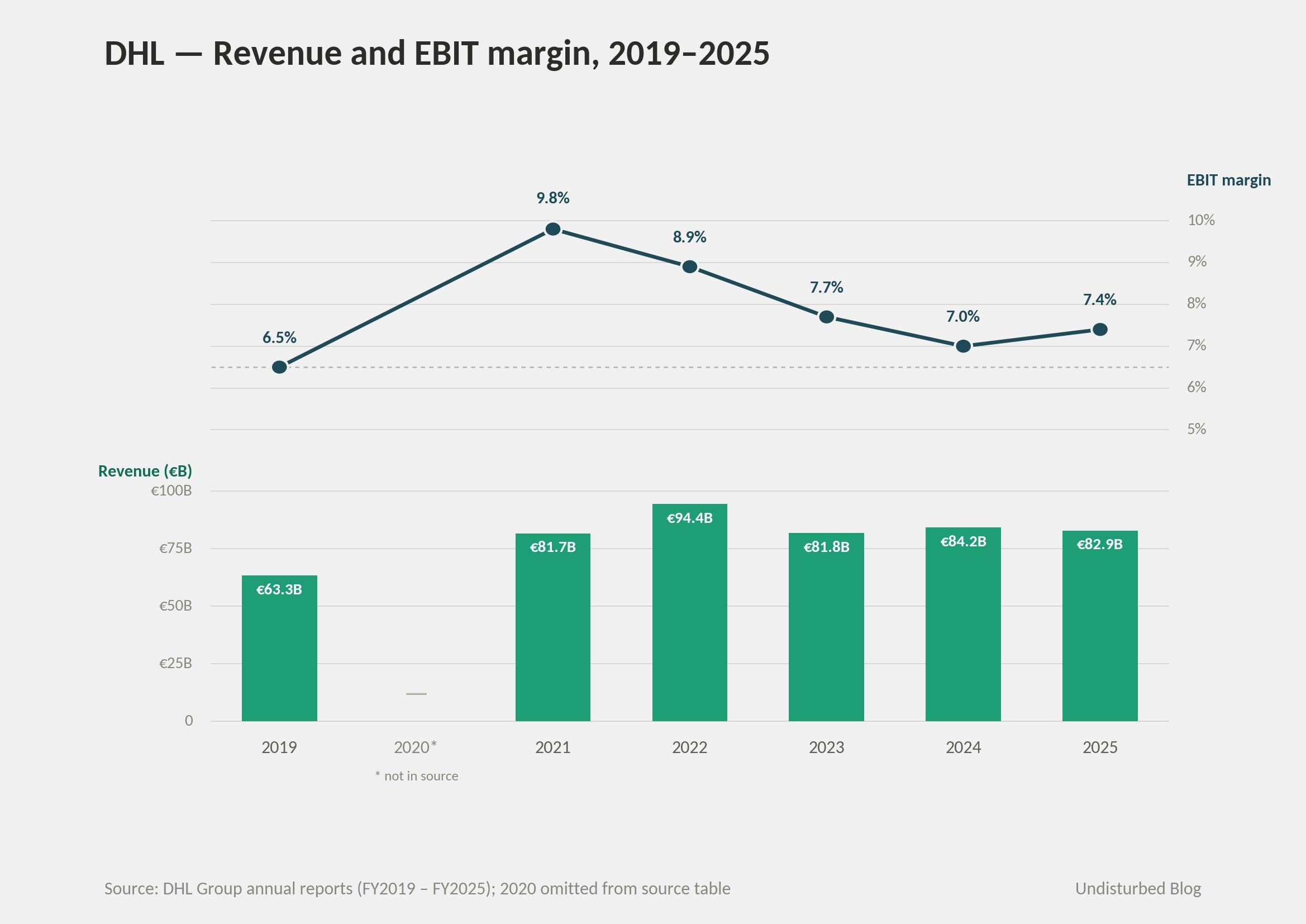

DHL Group ended FY2025 with €82.9B in revenue, €6.1B EBIT, and roughly 600,000 employees across 220 countries. Most logistics companies that size spent the year defending margin. DHL spent it collapsing five historically separate divisions — Express, Global Forwarding-Freight, Supply Chain, eCommerce, Post & Parcel Germany — onto one data substrate, one brand, and one legal entity, with AI work piled on top in deliberate sequence. The 2023 group rename to "DHL Group," the 2024 Strategy 2030 announcement, the 2025 "Fit for Growth" €1B cost program, and the May 5, 2026 hive-down vote that renames the listed parent to DHL AG are all running on a single timeline under one CEO — Tobias Meyer, in the role since May 2023 and just extended to March 2031.

The interesting question isn't what DHL is doing with AI. It's the order in which it's doing things. IDEA warehouse optimization, Boston Dynamics Stretch (1,000+ robots committed by 2030), HappyRobot agentic AI, GenAI in myDHLi, and Everstream Analytics — the Resilience360 spin-off DHL still owns equity in — are not the strategy. They are workloads sitting on a substrate the company has been building for fifteen years and is now finishing in public. In businesses that grew by acquisition, AI strategy without a data-layer strategy is a sequence of demos. What transfers from DHL isn't tooling. It's sequencing: brand and legal unification first, data and integration layer second, AI workloads third. Companies that get this order right earn compounding returns. The ones that invert it discover, two years in, that they're trying to run quarterly-cadence AI on an annual-cadence organism that isn't actually one organism.

The Strategy in One Picture

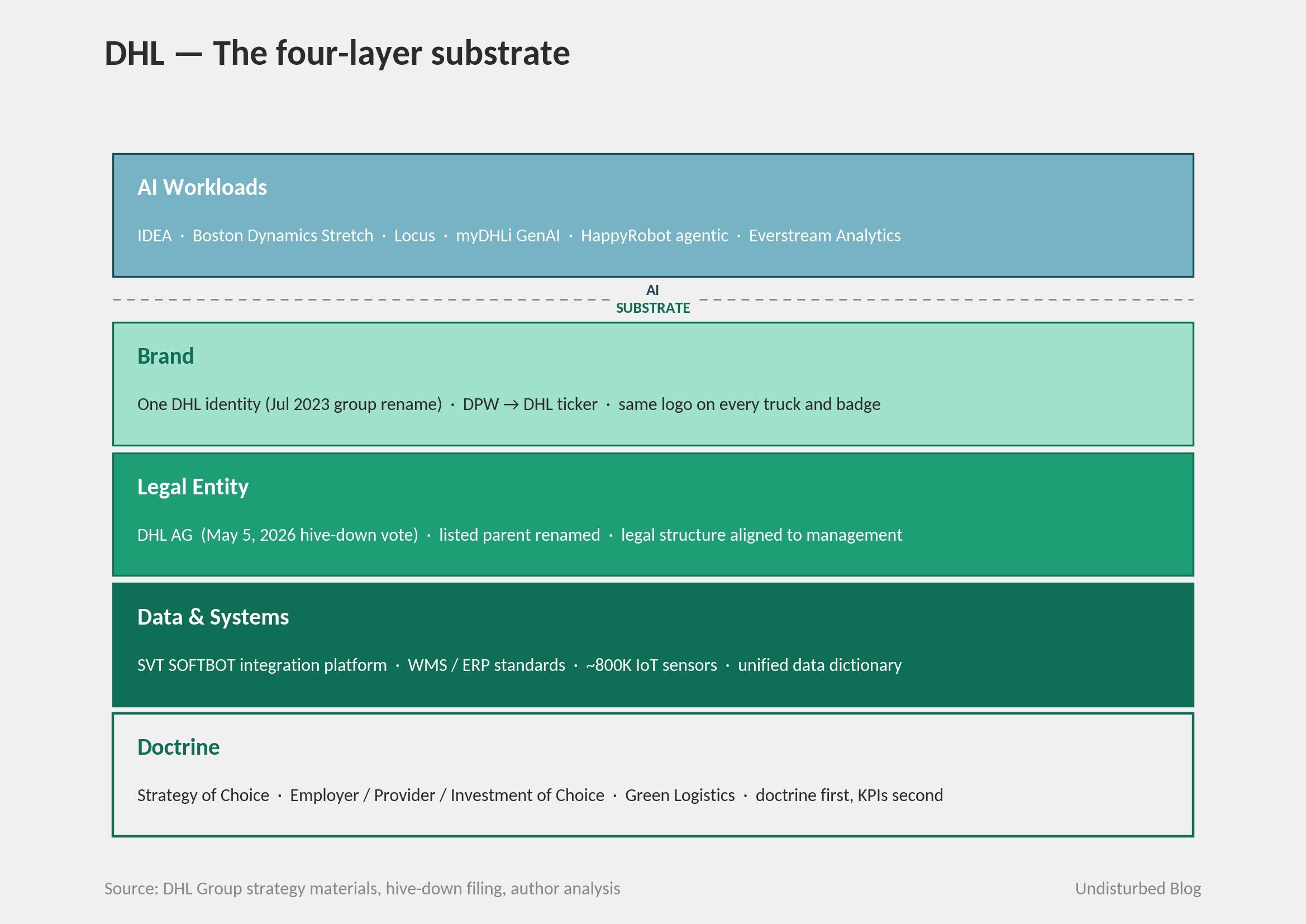

DHL itself doesn't frame its strategy this way. The official label is "Strategy 2030 — Accelerate Sustainable Growth," with "Fit for Growth" as the cost program and "Accelerated Digitalization" as the technology agenda. The more interesting reading is that brand, legal, data, and doctrine are being treated as one substrate — and AI is being placed on top of it, deliberately, in that order.

Read the timeline top to bottom and the pattern reads itself. The substrate is not just a database. It's a brand, a legal entity, a robotics-integration layer, and a doctrine running together. Each was politically blocked before 2023; each is now being executed under one CEO on one timeline.

The naive reading is "build a data lake, then put AI on it." The DHL reading is broader. The substrate has four layers — brand, so customers experience one company; legal, so the same accountability flows everywhere; data and systems, so the same record means the same thing across divisions; and doctrine, so people across divisions interpret the same data the same way. All four have to move together, or the data layer is just expensive plumbing.

The reason most "AI transformation" programs fail in mature companies isn't model quality. It's that the brand still says "BU 1," the legal entity still has its own GL, the data dictionary still has three definitions of "customer," and the doctrine still rewards local optimization. AI deployed into that architecture amplifies the inconsistencies rather than resolving them. DHL's bet is that the four layers get fixed first.

The three AI workloads on top are real. IDEA optimizes warehouse picking across 2,000+ Supply Chain operations. myDHLi gives 20,000+ forwarding customers a unified portal, with a GenAI assistant added in 2024. Everstream Analytics — what Resilience360 became after its 2021 spin-off — processes 20+ billion supply-chain risk data points a day and feeds DHL customers (Apple, Disney, Goodyear, and Campbell's are publicly disclosed users). All three would be feasible on a fragmented substrate; none would compound. The pattern only works if the substrate work is genuine. Bolt AI onto five disconnected divisions and the demos work in isolation but don't aggregate. The thing most companies get wrong about substrate-first strategy isn't the AI investment — it's discovering, two years in, that they skipped the substrate.

How It Actually Works — Three Workloads on One Substrate

Loop 1 · IDEA and the robotics integration layer

IDEA was launched in August 2020 by DHL Supply Chain — a software solution that uses operations-research clustering to optimize warehouse picking and labor allocation across high-SKU, small-order e-fulfillment sites. Algorithmic knowledge transferred from DHL's transportation routing. It plugs into existing WMS/ERP environments without replacement. Early commercial deployments reported up to 50% reduction in employee travel distance and up to 30% productivity gains. Built and owned in-house by a 350-person team.

In 2024–2025, IDEA stopped being the headline. The headline became the integration layer underneath the robots. By mid-2025, DHL Supply Chain runs 7,500+ robots globally — Boston Dynamics Stretch, Locus assisted-picking, AutoStore, Geek+, Fox Robotics, RobustAI Carter, 6 River Systems — alongside 200,000+ smart handheld devices and roughly 800,000 IoT sensors. Locus alone surpassed 500 million picks at DHL by June 2024, with the last 100 million taking 154 days versus 2.5 years for the first 10 million — a power-law learning curve.

The substrate-first move is visible in the framing. Tim Tetzlaff, Global Head of Digital Transformation at DHL Supply Chain, has put it this way: every provider used a unique interface and data format, every project was custom, rollouts were slow. The fix is the SVT Robotics SOFTBOT Platform plus DHL's modular standards — what Tetzlaff calls "the glue between our warehouse management system and our digitalization agenda." DHL now reports it integrates new robotic solutions up to 12× faster than before, with replication across sites in as little as three hours.

This is where substrate-first becomes operational. The robots are commodity. The data and integration layer between WMS, robots, and AI workloads is the moat.

GenAI followed the same logic. In October 2024, working with BCG X, DHL Supply Chain rolled out two production GenAI applications — data cleansing for Solutions Design, and proposal-development for sales — through what Sally Miller (Global CIO, DHL Supply Chain) calls a "product funnel approach" rather than horizontal rollout. In November 2025, agentic AI extended further through HappyRobot: appointment scheduling, driver follow-up, transport status calls, high-priority warehouse coordination. The deployment targets hundreds of thousands of emails and millions of voice minutes annually.

The closed loop runs like this: site telemetry from sensors and robots feeds orchestration via SOFTBOT, IDEA and GenAI and agentic decisions are produced from it, outcomes flow back into the layer. The loop is what makes substrate consolidation worth the cost.

Loop 2 · myDHLi and Everstream — the data asset DHL kept after spinning out

Resilience360 was incubated inside DHL's Global Innovation Center in 2014, after the 2011 Tōhoku earthquake and Thai floods made supply-chain risk visibility a board topic. Architect: Katja Busch, DHL's Chief Commercial Officer. It was originally a tool DHL sold to its own forwarding and contract-logistics customers.

In 2018 it became standalone. In 2020 it merged with Riskpulse, a U.S. weather-and-risk specialist. On March 2, 2021 the combined entity rebranded as Everstream Analytics, with Julie Gerdeman as CEO from June 2021. DHL retained equity. Subsequent funding: $24M Series A in 2022 (Morgan Stanley Investment Management, Columbia Capital, StepStone, with DHL participating) and $50M Series B in April 2023.

What Everstream demonstrates is the advanced version of the substrate move — separating a data asset that needs independent investor capital and an industry-neutral commercial proposition, while keeping the customer-relationship feed. Everstream processes 20+ billion data points daily across 220 countries; many Fortune 500 companies (Apple, Disney, Goodyear, and Campbell's are publicly disclosed) depend on it. DHL keeps commercial integration and equity, so the data substrate stays connected after the ownership separation.

The 2020–2024 polycrisis stress-tested the model. COVID (2020–22), Ukraine invasion (2022), Suez blockage (2021), Red Sea / Houthi disruption (2023–24), Panama Canal drought (2023–24), U.S. tariff turbulence (2025). DHL's customer-facing risk-and-resilience products were repeatedly cited in quarterly commentary as the reason customers continued to invest in DHL contract logistics even when freight rates were soft.

myDHLi is the parallel customer-facing data asset on the forwarding side: launched 2020, by 2024 carrying 20,000+ active customers and 450,000+ shipments tracked monthly. The GenAI virtual assistant was added in May 2024.

The pattern across both: own the data-layer customer interface, then either keep the algorithm in-house (myDHLi GenAI) or spin it out while keeping commercial reach (Everstream). Either way, the substrate stays connected.

Loop 3 · Brand and legal hive-down — the substrate becomes physical

The third "loop" isn't an AI system. It's the physical infrastructure that makes all the AI systems coherent.

July 1, 2023: "Deutsche Post DHL Group" became "DHL Group." The stock ticker moved from DPW to DHL on the Frankfurt exchange. Over 90% of group revenue already traded under the DHL brand at that point — the rename made physical what was already economically true. September 23, 2024: Strategy 2030 commits to "align complex legal structures with proven management structure" and a "lean divisional set-up." March 2025: Fit for Growth program announced, targeting more than €1B in structural cost savings by FY2027. October 2025: DHL Europe Innovation Center opens in Troisdorf. March 17, 2026: the hive-down report formally proposes renaming the listed parent from Deutsche Post AG to DHL AG. May 5, 2026: AGM vote.

This is the part that doesn't show up in conventional AI strategy decks. The brand on every truck, the legal name on every contract, the org chart on every job posting — these aren't decorative. They're the UI layer of the substrate. When all three say "DHL," the data dictionary inside has a fighting chance of converging too. When two of them still say "Deutsche Post," it doesn't.

This loop closes more slowly than the others — multi-year, AGM-gated, regulatorily complex. But once it closes it's permanent. A legal hive-down can't be rolled back the way a software deployment can.

The Numbers

DHL Group's P&L through the substrate-build period.

The pandemic super-cycle is over. What remains is structurally higher profitability than pre-pandemic — 7.4% EBIT margin in FY2025 versus 6.5% in FY2019 — which DHL attributes in its own commentary to capacity management, yield discipline, and the digitalization agenda. Margins, not volumes, are doing the work. That's exactly what would be expected when a company is running its existing assets harder via better data, rather than adding a new asset class.

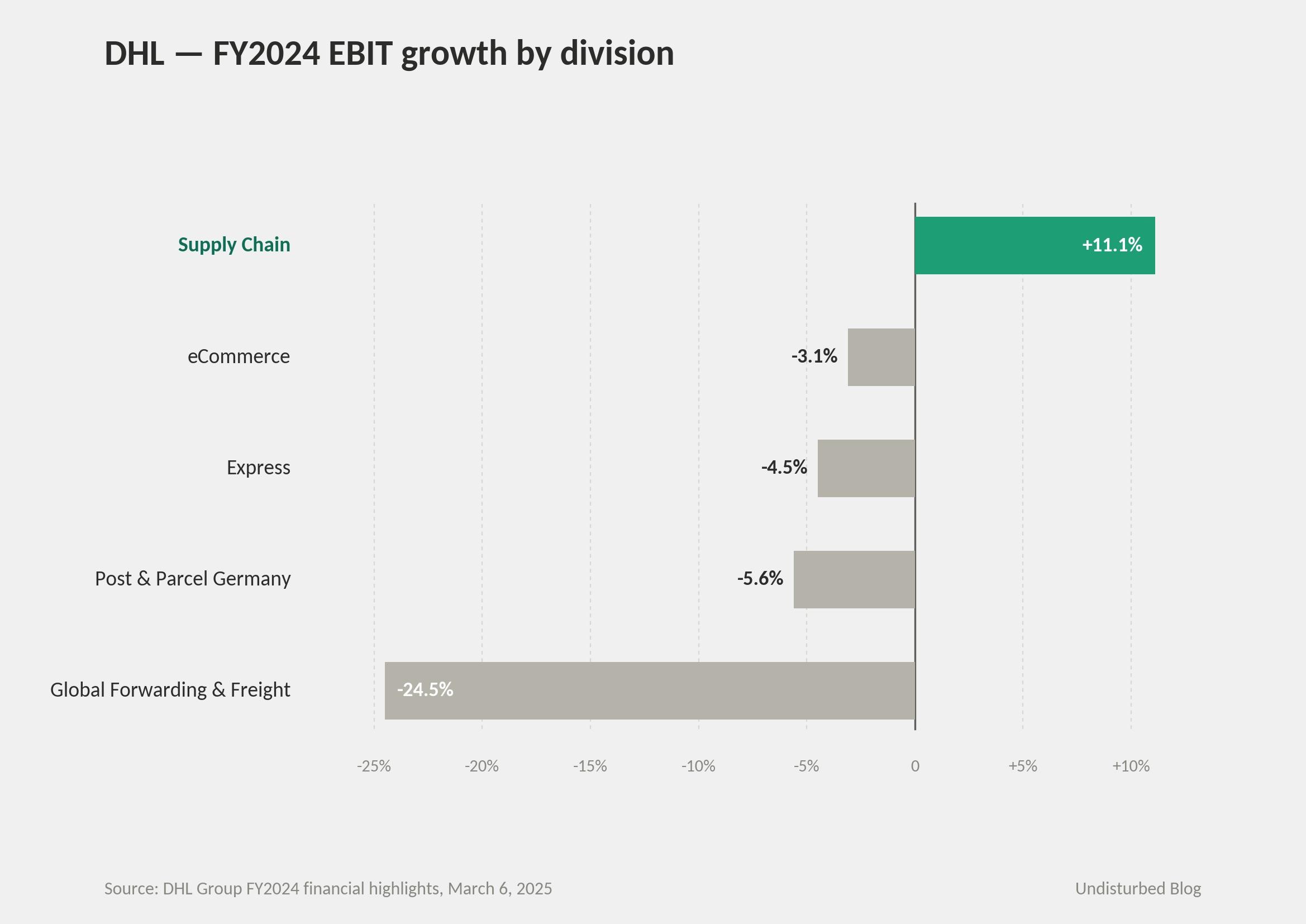

The most legible signal is divisional. Supply Chain — the most digitalized division — was the only one to grow EBIT in 2024 in a soft macro.

That's the substrate dividend, showing up where the substrate work is most complete. The cleanest diagnostic for whether substrate-first strategy is working is to ignore the loudest division and watch the longest-integrated one. Supply Chain's +11.1% EBIT growth in a soft 2024 macro, while every other division at DHL fell, is the truest read on whether IDEA, SVT integration, Locus, and Stretch are producing compounding returns. The other divisions follow if and only if their substrates catch up. If they don't follow within 18–24 months of substrate work, the diagnosis isn't that AI didn't deliver. The diagnosis is that the substrate work didn't actually finish — and companies that confuse the two often double down on AI when they should double down on the substrate.

Strategy 2030, announced September 23, 2024, targets 50% revenue growth versus 2023 by 2030 (roughly €122B), with a fourth bottom line — "Green Logistics of Choice" — committing to a 30% Sustainable Aviation Fuel blend by 2030 and decarbonization by 2050. About 80% of growth from divisional initiatives, 20% from cross-Group initiatives. Mid-term EBIT guidance was revised in November 2024 from the original €7.5–8.5B floor to more than €7B for 2026 — a quiet but important downgrade reflecting trade-policy turbulence.

Fit for Growth, announced in March 2025, targets more than €1B in structural cost reduction with full impact in 2027, including roughly 8,000 socially-responsible headcount reductions at Post & Parcel Germany, AI-enabled customer service, network optimization at Express, and "automation and digitization in operations across all divisions."

Capex: €2.95B FY2025, €3.1B FY2024, €3.4B FY2023. Within that, DHL Supply Chain has invested more than €1B in contract-logistics automation in the three years through May 2025. DHL Supply Chain UK & Ireland alone committed £550M (around €637M) in July 2025 for further automation through 2030. DHL Health Logistics has committed €2B in additional investment to 2030.

Each program has a named owner. Tobias Meyer (Group CEO, contract through March 2031). Melanie Kreis (CFO). Hendrik Venter (CEO Supply Chain, August 2025). Oscar de Bok (CEO Global Forwarding-Freight, August 2025; previously Supply Chain CEO). John Pearson (CEO Express). Mark Kunar (CEO Supply Chain North America, June 2025). Sally Miller (Global CIO, Supply Chain — the most-quoted operational owner of the AI agenda). Tim Tetzlaff (Global Head of Digital Transformation, Supply Chain — the public face of the integration-layer work). Katja Busch (Chief Commercial Officer, original Resilience360 architect).

Is AI a Norm Inside DHL?

The honest answer: deeply yes in Supply Chain, normalizing in the others.

DHL Supply Chain is the AI-native division. By mid-2025: 7,500+ robots, 200,000+ smart handheld devices, roughly 800,000 IoT sensors, 8,000+ collaborative robots. Roughly 10,000 automation and digitalization projects deployed across the network. More than 90% of warehouses globally have at least one automation or digital solution. The "Accelerated Digitalization" agenda is now organized around three priorities — orchestration, robotics, and AI — explicitly in that order. GenAI rolls out via a structured product funnel. Agentic AI (HappyRobot, November 2025) is already in production for hundreds of thousands of emails and millions of voice minutes per year. Lindsay Bridges, EVP HR DHL Supply Chain, frames the deployment in HR language: relieving teams from repetitive tasks, making roles more attractive — explicitly not a cost-cut narrative.

DHL Express uses ML for last-mile, load building, and customer interaction. Oliver Facey (SVP Global Network Operations, Express) describes AI publicly as enabling capacity-prediction in fractions of a second. But the public AI story for Express is still a set of discrete optimization tools, not a single substrate that runs the network the way ORION runs UPS.

DHL Global Forwarding-Freight runs myDHLi (20,000+ active customers, 450,000+ shipments tracked monthly, GenAI assistant added May 2024) and Smart ETA predictive analytics. Maturing, not yet at the level of Supply Chain.

DHL eCommerce and Post & Parcel Germany are at the early end. eCommerce's 2025 headline was network expansion (the Evri JV in the UK, September 2025). Post & Parcel Germany's 2025 headline was structural restructuring — the 8,000 socially-responsible headcount reductions over Fit for Growth's full impact period.

The doctrinal anchor across all five is "Strategy of Choice" — Employer of Choice → Provider of Choice → Investment of Choice — a framing DHL has held since Strategy 2015. The 2024 addition of "Green Logistics of Choice" as a fourth bottom line institutionalizes the same shape: doctrine first, KPIs second. AI is presented internally as serving Employer of Choice (relieving repetitive work) and Provider of Choice (faster onboarding, sharper customer responsiveness) — not as a cost-cut play. This is unusual, and it matters. It lets substrate-first be sold internally as "the floor that lets every employee work better," rather than "the floor that lets us replace you."

This is the part the data-lake-first reading misses. A unified data dictionary doesn't help if Division A interprets "active customer" as "billed in last 90 days" while Division B reads it as "logged in this quarter." The ETL can join the rows; the meaning still diverges. "Strategy of Choice" is not a values poster. It's the interpretive grammar that lets a Forwarding salesperson, a Supply Chain operator, and an Express dispatcher read the same data and act on it the same way. Without that grammar, the substrate reduces to expensive plumbing.

Brand unification is the organizational signal that makes all of this coherent. When the group renamed to DHL Group in mid-2023, when divisional structure was simplified in 2024, when the legal structure is being aligned to management structure in 2024–2026 toward DHL AG, employees receive the same physical daily reminder shareholders do: this is one organism. The same logo on every truck and badge is, in substrate terms, the UI layer on top of the data layer.

Why This Answer Fits DHL (and Won't Transplant Cleanly)

Three eras of historical DNA. Klaus Zumwinkel (1990–2008): aggressive M&A — Danzas in 1999, AEI in 1999, DHL in 1998–2002, Airborne in 2003, Exel in 2005 (£3.7B / €5.5B, integrating 111,000 Exel employees into 30,000 DHL Logistics employees, "one of the biggest integration projects ever carried out in the UK"). Frank Appel (2008–2023): digestion. The U.S.-domestic exit in 2008–09. Strategy 2015 / 2020 / 2025 framed at five-year cadence. Postbank deconsolidation. The four megatrends — globalization, digitalization, sustainability, e-commerce — institutionalized as the operating frame. Tobias Meyer (2023–): brand unification, Strategy 2030, Fit for Growth, AI acceleration, hive-down to DHL AG.

The pattern across all three eras is integration as continuous discipline, never the 18-month sprint that's normal in U.S. boardrooms. That's the part that sets up the substrate work.

The make-or-buy posture is consistent. Build the data layer and core algorithms (IDEA, the Resilience360 → Everstream-equity model, the myDHLi GenAI assistant, the integration platform with SVT Robotics). Buy or co-develop where the device or model is the commodity (Boston Dynamics Stretch, Locus, AutoStore, BCG X for GenAI use cases, HappyRobot for agentic AI). The data is sovereign; the hands aren't.

What makes 2023–2026 the inflection point isn't any single pressure. Four arrived together, the way they did at FedEx in 2022 and UPS in 2020 — but in a configuration only Europe could produce. New leadership: Tobias Meyer's May 2023 arrival as the first internally-promoted CEO in the post-Appel era, with insider fluency across three of the five divisions. Cost-structure pressure: Fit for Growth at €1B, full impact 2027, including 8,000 socially-responsible headcount reductions in P&P Germany. Competitor displacement: DSV's €14.3B acquisition of DB Schenker, closed April 30, 2025, creating a forwarder larger than DHL Global Forwarding by air and ocean volume — combined with FedEx's Network 2.0 / DRIVE program and UPS's Network of the Future. DHL no longer leads on pure forwarding scale; substrate-first is its differentiated answer. Integration mandate, externalized: Brand unification (2023) plus the legal hive-down to DHL AG (May 5, 2026 AGM vote) make the substrate work board-level, regulator-visible, and irreversible.

That's the part that doesn't transfer. Three structural conditions make this configuration almost exclusively German-European.

First, Mittelstand governance. CEO contracts in five-year increments (Meyer's was just renewed to March 2031). Strategy cycles in five-year iterations. Supervisory boards thinking in 30-year sustainability horizons. A U.S. CEO running on a 4-year horizon with shareholder-return pressure cannot underwrite a five-year integration layer. The substrate work is structurally unfundable.

Second, GDPR essentially mandates substrate consolidation for European multinationals. EU data regulation — the right to be forgotten, data minimization, purpose limitation, cross-border transfer rules — makes "five different customer databases with five different definitions of consent" a legal liability, not just an architectural one. Companies operating primarily in less-regulated jurisdictions have far weaker forcing functions for substrate consolidation. In the EU, this pattern sits closer to compliance than to strategy; in the U.S. and most of Asia, it sits in optional-strategy territory.

Third, the 15-year prior integration period. Appel's 2008–2023 era was substrate-preparing work — divestitures, IT consolidation, cultural cohesion across acquired entities — that made Meyer's substrate-finishing work even thinkable. A company that hasn't done that 15-year prior work cannot start a substrate-first program in 2026 and expect to be where DHL is in 2030. Activation energy makes the moment possible; architecture makes the moment defensible. DHL has both, in a configuration that took 30 years to assemble.

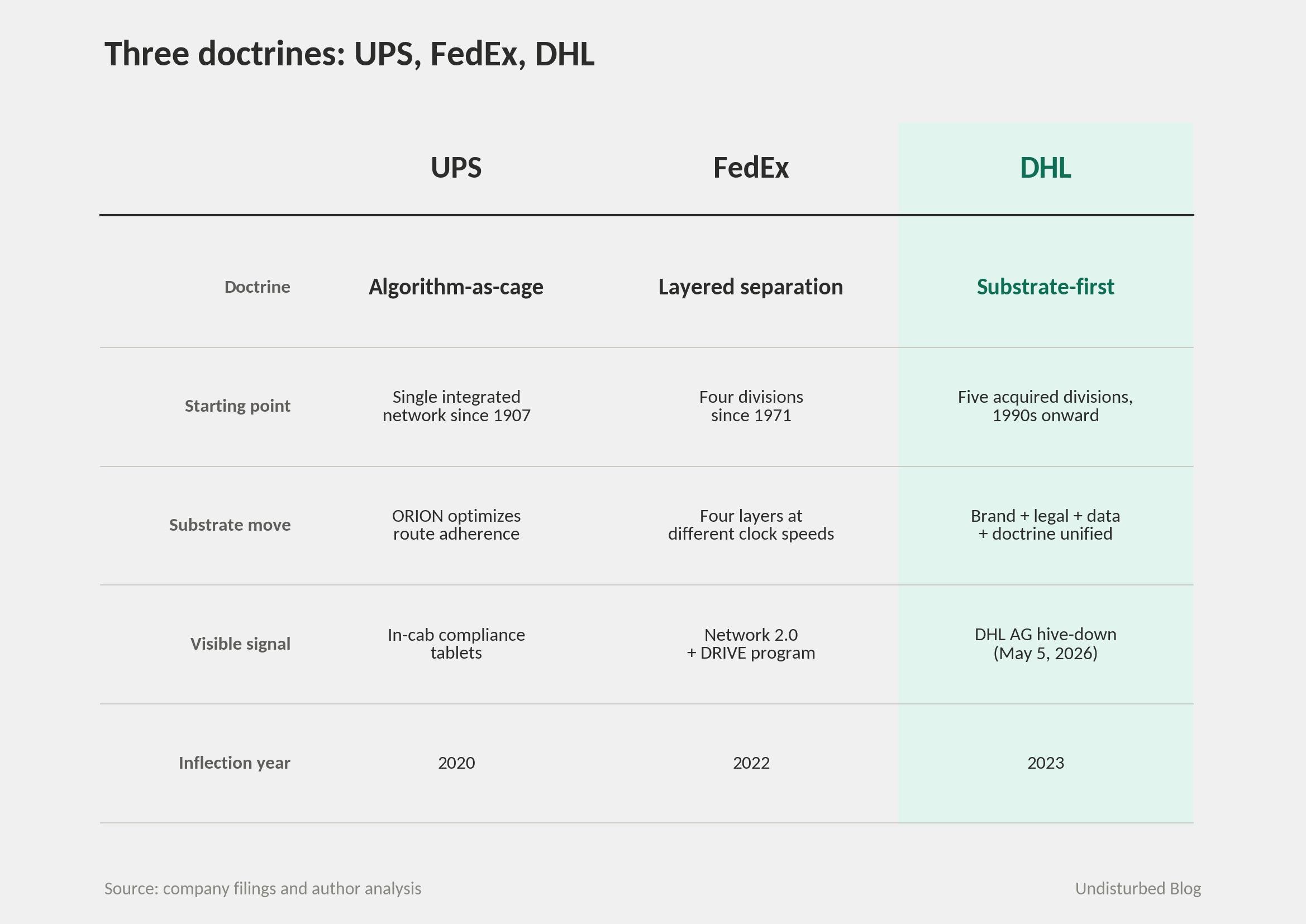

UPS, FedEx, and DHL have all reached the AI-strategy inflection. The interesting fact is that they've reached it from three different starting points and arrived at three different doctrines.

UPS inherited a single integrated network from 1907; the algorithm became the cage. FedEx ran four layers at different clock speeds since 2022; the separation became the strategy. DHL has spent fifteen years integrating five acquired divisions onto one substrate, with brand and legal hive-down as the visible signals. None of the three is copyable as architecture. What transfers is the recognition that AI strategy is downstream of substrate strategy — and that the right substrate depends on what the company already has. A U.S. parcel carrier shouldn't try to imitate DHL's five-division integration any more than DHL should try to imitate ORION. The doctrine, not the implementation, is the lesson.

Where It Goes Next

Three trajectories. First, the May 5, 2026 AGM vote on the hive-down to DHL AG — the substrate's physical completion. If it passes, and it almost certainly will, the substrate work has a hard endpoint and the AI layer has a clear runway. If it doesn't, the timeline slips by 12–18 months but the trajectory is unchanged.

Second, the divisional catch-up. Supply Chain is the AI showcase; the others are at varying stages of digital maturity. Express likely develops a group-level AI substrate equivalent to ORION at UPS — not because it copies UPS, but because the substrate readiness now permits it. Forwarding's myDHLi continues maturing toward agent-driven customer interaction. P&P Germany's 8,000-person headcount reduction (2025–2027) frees capital for AI deployment by 2028.

Third, the post-DSV-Schenker competitive landscape. DSV targets $1.4B in synergies by 2028. If DSV stumbles on integration — German labor relations, Schenker IT, contract-logistics culture — DHL Global Forwarding gets breathing room. If DSV executes well, DHL needs the substrate-and-AI play to be working at full effect by 2028 to defend forwarding margin.

The longer-tail bets. DHL Health Logistics scales toward roughly €2B/year by 2030. The Africa investment (€300M+, October 2025) extends substrate-first into a high-growth region. The North America data-center logistics build (10 sites, 7M+ sq ft, going live in 2026) is a substrate move into AI's physical infrastructure layer — the racks, the cooling, the deployment logistics that make AI possible elsewhere. There's a recursion to it: DHL is using its own substrate to build the logistics for everyone else's AI.

The risks are visible. Strategy 2030's 50% revenue growth target rests on global trade conditions normalizing; the November 2024 EBIT downgrade (€7.5–8.5B → more than €7B for 2026) suggests one revision has already been absorbed. Trade-policy exposure is exogenous and uncontainable. Most AI productivity claims (50% travel reduction with IDEA, 700 cases/hour with Stretch, 12× faster integrations with SVT) come from DHL's own materials and pilot deployments, not third-party audit. Division asymmetry is real — generalizing the Supply Chain story to the whole group overstates current reality.

The Diagnostic the Case Forces

The DHL case raises four diagnostics that map to the four pressures any substrate-first move depends on.

On the substrate. The first diagnostic is whether a single end-to-end view of one customer can be assembled from one query across acquired divisions, legal entities, and geographies. In most companies that grew by acquisition, that view requires more than three systems and surfaces contradictions on the first reconciliation. That's the substrate problem, and it sits underneath whatever AI investment is happening on top. DHL's answer to its own version of this question was a five-year program of brand, legal, and data unification — not an AI roadmap.

On the algorithm. The second diagnostic is whether margin improvement over the last three years came from substrate consolidation — one ERP, one CRM, one data model, one warehouse-management standard — or from discrete AI/automation projects. DHL Supply Chain's +11.1% EBIT growth in a soft 2024 macro is the test. When substrate consolidation isn't yet visible in margin, AI projects struggle to compound. They produce demos that don't aggregate.

On the doctrine. The third diagnostic is whether integration is a project — with a manager, a deadline, a steering committee — or a doctrine, present in every promotion conversation and every architectural decision. DHL's 15-year track record under Appel and Meyer answers the question with brand renames, legal hive-downs, and the Strategy of Choice framing carried across four five-year strategy cycles. A program team doesn't get a company to a finished substrate. A doctrine carried by the CEO and supervisory board does.

On the timing. The fourth diagnostic is whether the four pressures are present together — new internal leadership, cost-structure crisis, competitor displacement, and a clear substrate mandate, whether brand, legal, or both. DHL has had all four since 2023. With three of the four absent, this pattern doesn't get past committee. With all four present and the company still not moving, the window is closing faster than the boardroom thinks — and substrate work is what permits movement, not what slows it down.

References