Tesco

16

min read

On 13 February 1995, every Tesco store in the UK closed for the weekend, dressed itself for a single launch, and re-opened to a national TV campaign and 16 million pre-printed loyalty cards. Within two weeks, seven million Clubcards had been distributed; within days, more than 70% of all sales were matched to a cardholder; within a year, Tesco had overtaken Sainsbury's. The analytical engine behind the launch — a six-year-old consultancy called dunnhumby — had been refining customer-data science for paying clients since 1989.

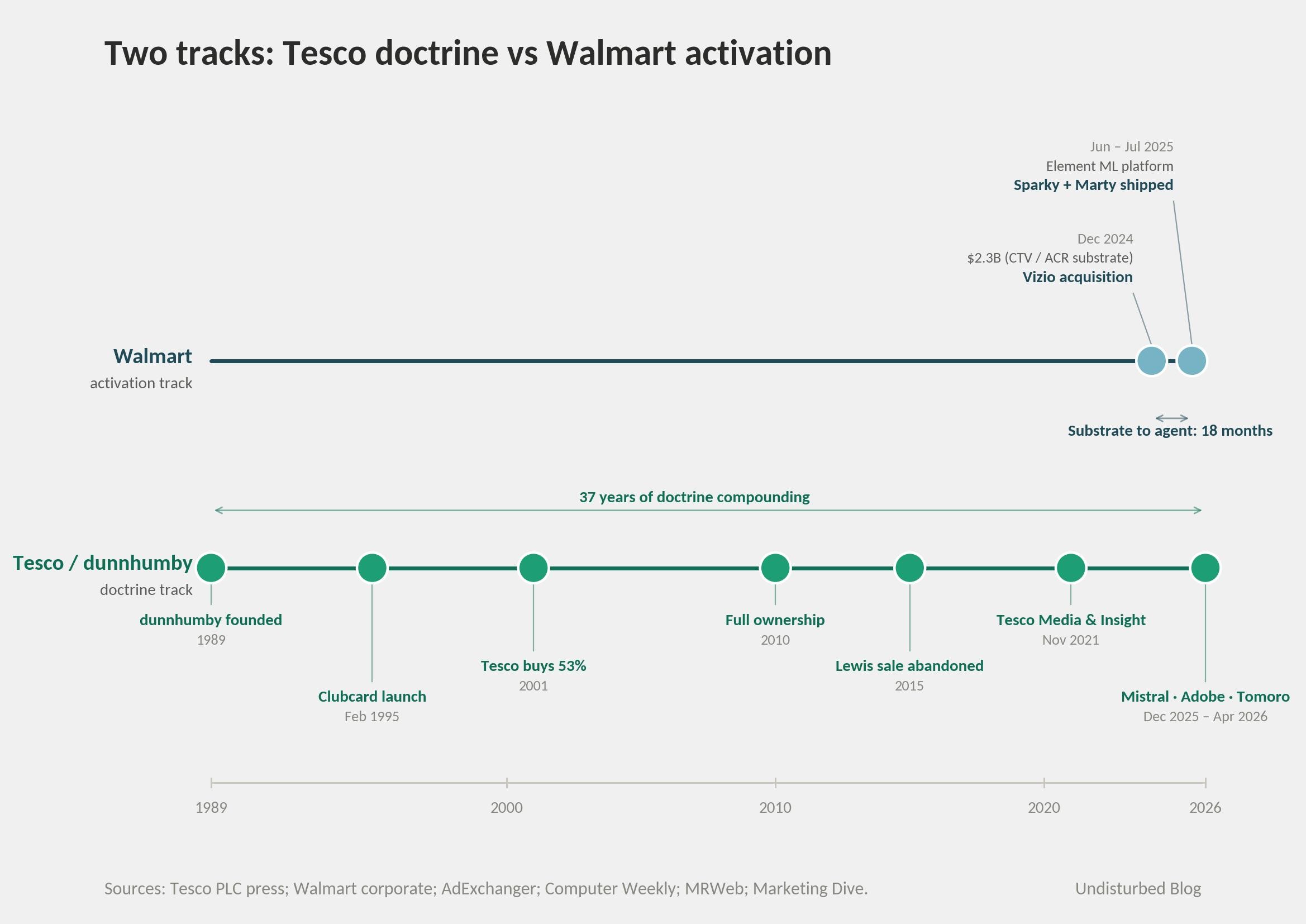

That sequence is the founding act of a pattern that has since defined modern retail: incumbents capturing operational transaction exhaust, refining it through a productized data layer, and selling access back to the brands whose goods sit on the shelves. Walmart Connect, now a $6.4B advertising business growing 46% year-over-year, is the largest contemporary version. Tesco's version is older by twenty-six years, structurally multi-client where Walmart's is first-party only, and licensed across thirty countries through dunnhumby. Doctrine compounds. But it does not guarantee velocity: as of May 2026, Walmart has shipped consumer-facing AI agents to its customers; Tesco's equivalent is still in colleague beta. The architecture moat and the activation moat are both real, and they are not held by the same company.

Pattern definition

In October 1994, Edwina Dunn and Clive Humby presented Clubcard pilot results to Tesco's board. Sir Ian MacLaurin, then chairman, broke the silence with a sentence that became the founding doctrine: that the consultants knew more about his customers after three months than he had known after thirty years. The board approved the national rollout. Four months later, on 13 February 1995, Tesco closed every UK store for the weekend, dressed them with Clubcard promotional materials, ran national TV ads, and mailed 16 million pre-printed cards. Within two weeks, seven million cards had been distributed; within days, more than 70% of all sales were matched to a cardholder; within a year, Tesco overtook Sainsbury's. Edwina Dunn's later estimate: Clubcard and dunnhumby produced an extra £60 billion in sales over the first decade.

What's structurally distinctive isn't the pattern itself — Walmart Connect runs the same playbook a quarter-century later — but the corporate sequence. dunnhumby was a six-year-old external company at the time of the 1994 pilot. Tesco's stake purchase in 2001 didn't create the productized layer — it bought and protected one that already existed. dunnhumby had clients before Tesco — Cable & Wireless, BMW, Booker Cash & Carry, Mercury Communications. The productization was already a multi-client SaaS; Tesco simply made it the largest single account.

This matters for the comparison. Walmart Connect was renamed from Walmart Media Group in January 2021; Walmart Data Ventures was formed the same year. dunnhumby was founded in 1989, working with Clubcard data from 1994, monetising customer-data-science as a paid service throughout the 1990s. Walmart is the largest US-scale version of the pattern — $6.4B in FY26 ad revenue is not a number Tesco's retail-media line can rival. But Tesco is the first global version, and dunnhumby is the multi-client SaaS template that even Walmart's Scintilla doesn't yet match.

MacLaurin's 1994 reaction is the founding doctrine, not the launch. The doctrine — knowing customers better than the chairman knew them — committed Tesco to treating customer data as a board-level asset before "data is the new oil" had been coined (Humby coined that phrase in 2006, eleven years later). Walmart's $2.3B Vizio acquisition in 2024 is the attempt to manufacture an equivalent inflection: buying 18 million households of ACR data. Tesco's inflection cost £750,000 — the original Clubcard trial budget against the £40-50M Tesco's own technologists had quoted for an in-house build. The acquisition cost ratio is roughly 3,000:1. The time-to-doctrine ratio is reversed.

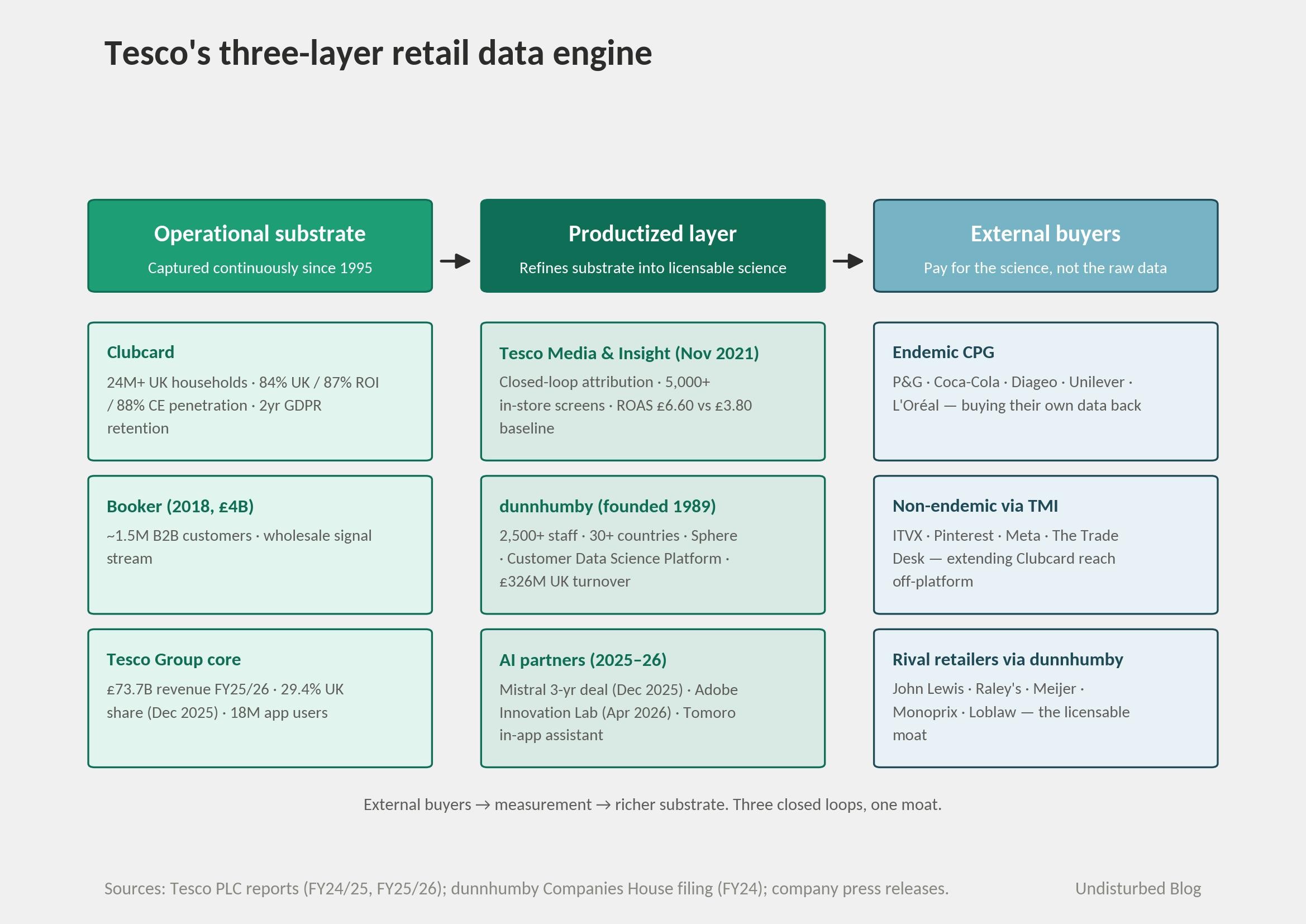

The strategy in one diagram

Two reads matter. First, every productized line on the right side rides on a substrate the core retail business has been paying to operate for thirty years — a longer compounding period than any other retail version of this pattern globally. Second, dunnhumby is the only piece in the architecture that licenses outward to non-Tesco retailers. Walmart Connect cannot license against Walmart's data to Kroger or Aldi. dunnhumby does the equivalent every working day.

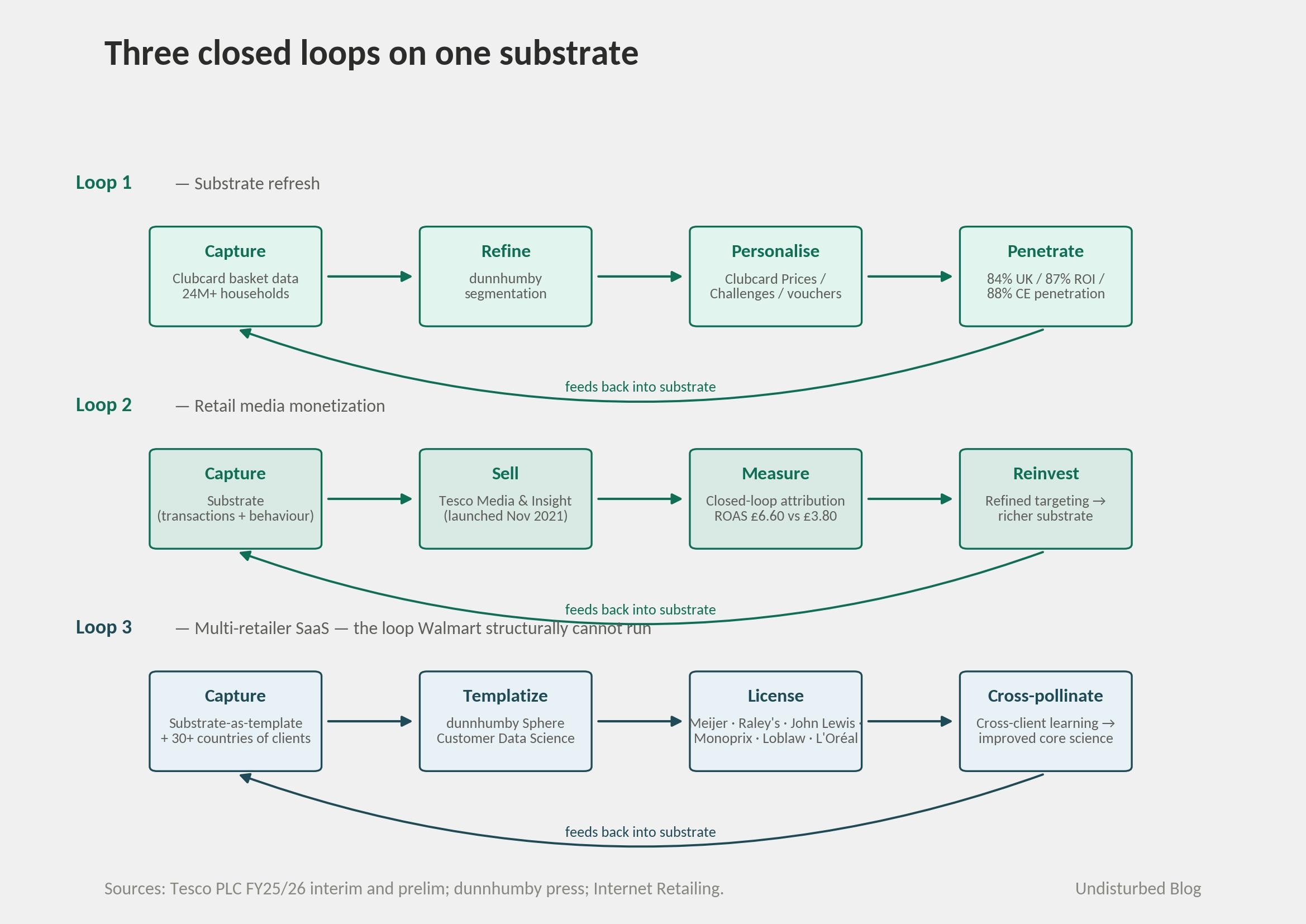

How it actually works — three closed loops

Loop 1: Clubcard → personalised offers → higher penetration → richer substrate.

Clubcard captures basket-level data → dunnhumby segments via the Customer Data Science Platform → personalised offers route back through Clubcard Prices (10,000+ products), Clubcard Challenges (10M targeted; "Best Global Loyalty Launch" at the 2025 International Loyalty Awards, powered by Eagle Eye/EagleAI), and personalised vouchers → Clubcard sales penetration reaches 84% UK / 87% ROI / 88% Central Europe in the FY25/26 interim → richer substrate for the next cycle. Christmas 2024 alone saw customers collect over half a billion extra Clubcard points through Challenges; Tesco called it its "biggest ever Christmas performance."

Loop 2: Substrate → retail media → external advertisers → measurement back to substrate.

Tesco Media & Insight Platform launched 30 November 2021, branded as the UK's largest closed-loop grocery media platform. Tash Whitmey (ex-Tesco Loyalty Director, ex-Havas Helia CEO) runs it as managing director; Lauren Bolles (ex-Walmart Connect Head of Business Operations) joined as COO in 2026 — a literal Walmart-to-Tesco talent transfer. The platform sells targeted reach across Tesco.com, the app (18M+ users), 5,000+ in-store digital screens (the UK's largest retail OOH network), partner channels (ITVX, Pinterest, The Trade Desk, Meta), and store wraps at up to 50 sites. Closed-loop attribution ties exposure to Clubcard purchase. Internet Retailing reports a Tesco Media ROAS of £6.60 versus £3.80 for non-retail-media digital advertising; Tesco's October 2025 supplier briefing positioned UK retail media as a £6.53B segment by end-2026 — large enough to surpass UK TV advertising.

Loop 3: Substrate-as-template → multi-retailer SaaS → external clients → cross-pollination.

This is the loop Walmart structurally cannot run. dunnhumby's Sphere platform, Customer Data Science Platform, Retailer Preference Index (annual), and Sciences-as-a-Service revenue come from selling capabilities developed against Tesco data — and against the data of dozens of other clients globally — to retailers that are not Tesco. Current named clients include Coca-Cola, Meijer (US grocery, ~500 stores), Procter & Gamble, Raley's (California), L'Oréal, Monoprix (France), and the John Lewis Partnership. The Kroger relationship that produced dunnhumbyUSA was restructured in April 2015: Kroger acquired the US assets to form 84.51° as an independent successor under a perpetual license. dunnhumby's US presence is now Meijer- and Raley's-shaped rather than Kroger-shaped. The pattern that survived the restructure is the multi-client one. Walmart Connect cannot do this — selling Walmart's data to Kroger would dissolve the moat. dunnhumby's data is dunnhumby's; selling it to Meijer is the moat.

The pattern in all three loops is the same. Tesco paid to capture data for itself. dunnhumby refined that data into productized science. The science is what external buyers actually want. The product is the science, not the data.

The numbers

Tesco's fiscal year ends in late February. FY25/26 results were presented on 16 April 2026.

FY | Group revenue | Adj. operating profit | UK share (Kantar) | Capex |

|---|---|---|---|---|

FY24/25 | £63.6B | £3.13B | 27.8% (Jan 2025) | £1.4B |

FY25/26 | £73.7B | £3.15B | 29.4% (4-wk Dec 2025) | £1.5B |

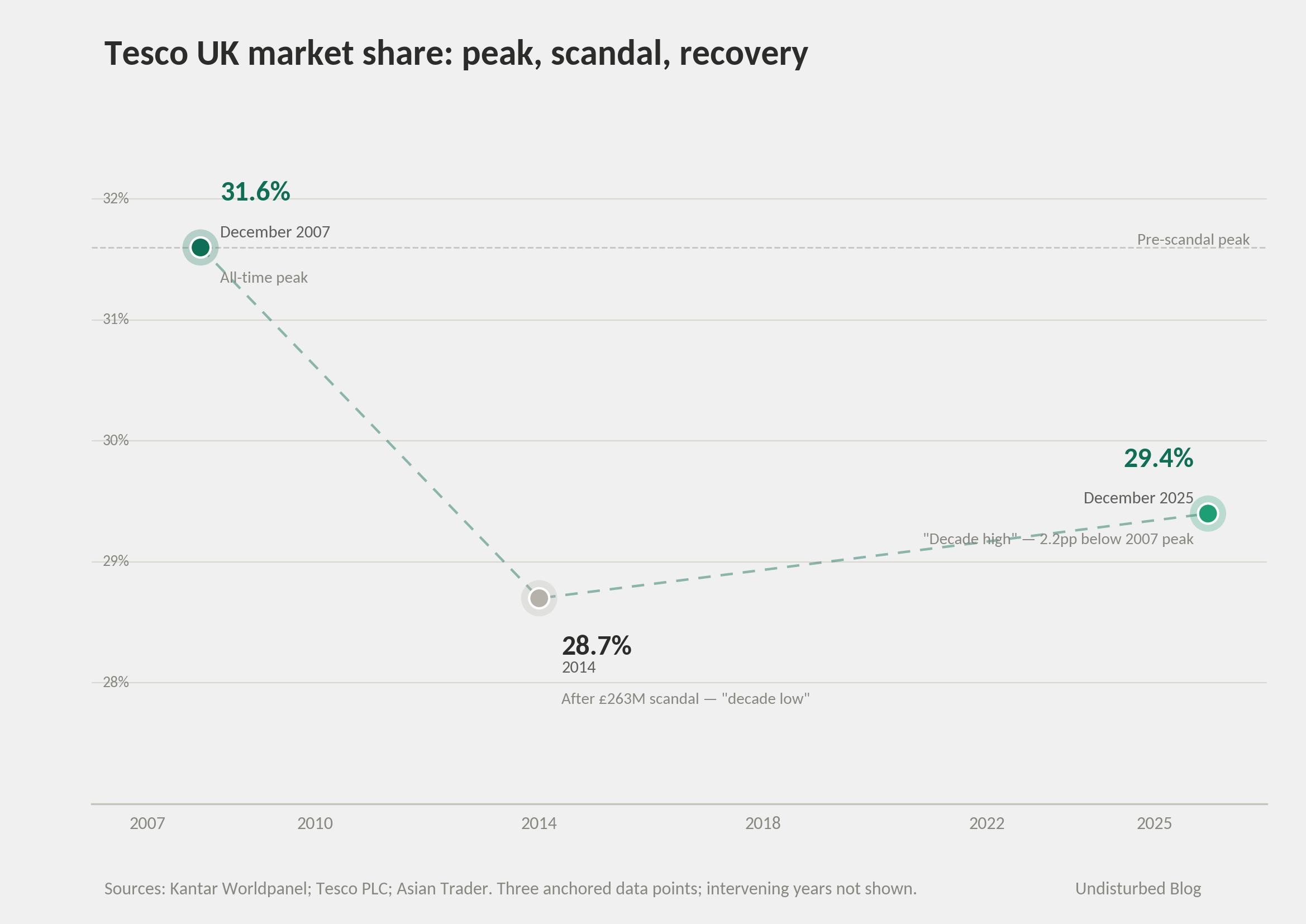

Tesco's UK share of 29.4% in the four weeks to 28 December 2025 is "the highest in over a decade" — but it is not an all-time peak. Tesco's historical maximum was approximately 31.6% in December 2007. The 2014 share, after the £263M accounting scandal, was 28.7% — described at the time as the lowest in a decade. The current "decade high" of 29.4% sits less than a percentage point above what was called "decade low" eleven years ago. The label changes; the underlying band barely moves. The structural read is that Tesco is recovering toward its pre-scandal scale — not surpassing it.

Substrate metrics (FY25/26 interim and prelim). Clubcard households: 24M+ (Adobe announcement, April 2026). Sales penetration: UK 84% / ROI 87% / Central Europe 88%. Tesco Group app users: 18M (+12% YoY); proportion of digital Clubcard scans in UK +11ppt to 63%. Whoosh rapid delivery: 1,500+ stores; +51% YoY. Tesco Marketplace: launched 4 June 2024 with 9,000 SKUs; now 400,000+ SKUs.

Retail-media revenue: undisclosed. Tesco does not break out Tesco Media revenue. Internet Retailing analysts estimate "hundreds of millions of pounds." This is not negligence; it is strategy. Walmart announces Connect revenue in every quarterly call because the announcement does business-development work — every CPG sees the growth rate and adjusts its retail-media budget upward. Tesco's silence does the inverse work: CPG buyers and their agencies do not know how big the inventory pool actually is, which preserves Tesco's pricing leverage. The same dynamic explains why dunnhumby's UK Ltd accounts (£326M, 795 staff) are the only public numbers — and why global group revenue and headcount have been stuck at "2,500+ in 30+ countries" in the official boilerplate for years. Disclosure here is a function of competitive game theory, not transparency norms.

dunnhumby Limited financials (UK legal entity, year ending Feb 2024). Turnover £326M, EBITDA £30M, 795 UK staff. The global group, across 30+ countries, employs 2,500+. The gap between UK-only filing and global group is structural — dunnhumby Inc. (US) and other regional entities have separate accounts. The defensible numbers are the Companies House filings.

Named program owners (May 2026).

Ken Murphy — Group CEO since 1 Oct 2020. Irish; ex-Walgreens Boots Alliance EVP/CCO; ex-P&G; UCC + HBS AMP.

Imran Nawaz — Group CFO since May 2021. Ex-Tate & Lyle CFO; 16 years at Mondelēz/Kraft.

Ashwin Prasad — UK CEO since 30 June 2025. Ex-Mars; 15+ years at Tesco.

Natasha Adams — Chief Strategy & Transformation Officer (newly created, June 2025).

Guus Dekkers — Group CTO since April 2018. Ex-Airbus CIO; ex-VW, Siemens, Continental.

Ruben Lara Hernandez — Director, Data, Analytics & AI. Mistral partnership owner.

Becky Brock — Group Customer Digital Transformation Director. Adobe partnership owner.

Tash Whitmey — MD, Tesco Media (since late 2023, sits inside dunnhumby).

Lauren Bolles — COO, Tesco Media (2026; ex-Walmart Connect).

Josh Bottomley — dunnhumby CEO since July 2023. Ex-CVC; ex-HSBC; ex-Google.

Tim Mason — Eagle Eye CEO; the Tesco marketing director who originally hired dunnhumby in 1993.

Tim Mason is the entry that matters. As Tesco marketing director in 1993, he commissioned the original dunnhumby trial; he is now CEO of Eagle Eye, the AI engine running Clubcard Challenges in 2025. The doctrinal continuity is literal. The same person who started the loop in 1993 is running its latest iteration thirty-two years later from a different company.

Succession and the AI deployment portfolio

The succession question is always the same: does the strategy survive a CEO transition? Tesco's answer is structurally yes — and weak on activation.

The succession arithmetic. Ken Murphy is 59, six years into the CEO role, share price near a 52-week high (508p), market share at decade high. He is not visibly on the way out. But the June 2025 reshuffle reads as preparation: Adams elevated to Chief Strategy & Transformation Officer (newly created); Prasad to UK CEO; Geoff Byrne to Tesco Ireland CEO. All three are internal; all three have spent careers inside the data-driven trading machine that MacLaurin and Leahy built. The substrate-as-doctrine is robust to a Murphy departure precisely because the doctrine is older than any of his predecessors.

The deployment portfolio. Mistral AI signed a 3-year agreement with Tesco on 17 December 2025 — first major UK retailer to partner with Mistral; full access to commercial models plus future releases; joint AI lab; explicitly EU-sovereign in data residency. Owner: Ruben Lara Hernandez. Adobe followed on 13 April 2026 with a Strategic AI Partnership: a Tesco × Adobe Innovation Lab with engineers embedded in Tesco; Adobe Firefly Foundry for creative GenAI at scale; Adobe agentic AI for personalisation. The headline framing — every Clubcard customer's grocery online journey personalised one-to-one — is the activation thesis. Owner: Becky Brock.

The Sparky-shaped gap. On 9 April 2026, Tesco quietly opened a beta of an in-app AI shopping assistant to 280,000 staff, built with UK consultancy Tomoro AI. The assistant does meal planning and basket building; customer rollout is "later this year"; the assistant has no public name yet (staff will help name it). This is Tesco's first public-facing GenAI consumer agent, and it is roughly ten months behind Walmart. Walmart shipped Sparky to customers on 6 June 2025; Marty followed in July 2025; both run on Walmart's proprietary Element ML platform.

The lag is not a doctrine failure. It is a velocity choice. Tesco can run Mistral against thirty years of Clubcard doctrine tomorrow; it has chosen to validate the workflow with staff first. If agentic commerce becomes the dominant retail interface in the next twenty-four months, the substrate advantage compounds for whoever ships the agent first — and that's Walmart. If agentic commerce is a slow build over five-plus years, Tesco's deeper substrate gives it room to ship later and ship better. Murphy's published thesis is the slow read: AI nudging on health, waste, and price-timing rather than search-replacement. The doctrine doesn't need an LLM to be valuable. The substrate already runs.

Why the answer fits Tesco specifically

Three doctrinal bets compound here.

1994 — the founding bet. Sir Ian MacLaurin and Terry Leahy approved a £750,000 trial at three stores when Tesco's own technologists had quoted £40-50M for an in-house build. dunnhumby's six-month trial demonstrated 60p of every £10 in those stores being spent by trial Clubcard members. The board's commitment to a national rollout in February 1995 — 16 million pre-printed cards, every store closed for the weekend, national TV — is the operational expression of MacLaurin's October 1994 doctrine. Sales overtook Sainsbury's within a year.

2001 — the make/buy bet. Tesco bought 53% of dunnhumby for £30M; raised the stake to 84% in 2006 for an additional £15M; took full ownership in 2010 (undisclosed). The cumulative cost of internalising the productized layer was modest — under £100M, against a customer-data-science capability that today serves clients across 30+ countries. Compare Walmart's $2.3B Vizio acquisition: roughly twenty-three times more expensive, for a substrate (CTV viewing data) that Walmart doesn't yet license to other retailers and structurally can't.

2015 — the doctrine test. Dave Lewis, recently arrived from Unilever to run a Tesco recovering from the £263M accounting scandal, identified dunnhumby as a £2bn potential disposal. The bidders — TPG, Nielsen, WPP, Google, John Browett (ex-Tesco/Dixons), and the founders Dunn and Humby themselves — circled. The price collapsed from £2bn to roughly £700m; bidders pulled out after Tesco told them the buyer would have to renegotiate the dunnhumby-Tesco contract within five years. Lewis abandoned the sale. This is the doctrine test. Walmart has not had — and structurally may not have — an equivalent moment.

Why now (2024-2026). Three forces converge: post-cookie advertising makes first-party loyalty data disproportionately valuable; GenAI maturity makes a thirty-year doctrine interpretable in natural language for the first time (Mistral, Adobe, Tomoro); and the retail-media duopoly is forming globally. Amazon Ads (~$56B 2024) and Walmart Connect ($6.4B FY26) define the US ceiling; Tesco and Sainsbury's are forming the UK equivalent.

Architecture vs activation energy — inverted. Walmart's Connect needed Vizio (2024) to manufacture an architecture inflection mid-cycle; Walmart's Sparky and Marty (2025) are the activation expression. Tesco's architecture compounded since 1995 — it doesn't need a Vizio-equivalent. But the activation expression (consumer-facing agentic AI) is roughly twelve months behind Walmart. Walmart leads on agentic activation; Tesco leads on substrate doctrine. Both moats are real; neither alone determines who wins the next decade of retail. Walmart can't license its first-party data substrate to Aldi or Kroger; dunnhumby has been doing the equivalent for two decades. Tesco hasn't yet shipped a customer-facing agentic UX as of May 2026; Walmart shipped Sparky in June 2025 and is running ad units inside it. The pattern has two equilibria, and these two retailers are exemplars of each.

Where it goes next

Agentic commerce inside Clubcard. The Adobe agentic AI capabilities + Mistral frontier models + Tomoro in-app assistant are the components for a Tesco Sparky-equivalent — but it will be Clubcard-native, not search-replacement. Murphy's published thesis: AI nudging on health, waste reduction, and price-timing recommendations. Expect a public name and customer launch in late 2026.

Booker integration. Booker, acquired in 2018 for £4B, supplies ~1.5M UK businesses; combining Booker's wholesale signals with Clubcard's retail-end signals into Sphere/TMI is the next data-asset frontier. Limited public progress to date. The frontier is real; the execution is unproven.

International AI strategy. Tesco is now structurally UK + ROI + Czechia / Slovakia / Hungary only. The international vehicle for the pattern is dunnhumby — selling Sphere to Loblaw, Raley's, John Lewis, Monoprix, Meijer. Tesco itself does not have a global retail footprint; dunnhumby has the equivalent of one.

Foundation-model ecosystem. Mistral (3-year deal, December 2025), Adobe (April 2026), Tomoro (April 2026) are public. No Anthropic, OpenAI or Google deals announced as of May 2026 — a notable gap given Walmart's deep OpenAI ecosystem and Sainsbury's Microsoft tie-up.

Possible M&A. A Vizio-equivalent for Tesco would be a CTV / connected-screen acquisition or a content-creator network. No public signals. The Booker template (B2B wholesale acquisition, 2018) suggests Tesco prefers operational acquisitions over media ones.

Risks to track. Clubcard Plus subscription quietly retired (the £7.99/month layered product had insufficient differentiation against Clubcard Prices). The CMA loyalty-pricing investigation, opened January 2024, found "little evidence" of widespread misleading promotions in November 2024 — but residual scrutiny on "was/now" promotions remains. Tesco Bank sold to Barclays for £600M in November 2024; Tesco Group no longer owns the financial-transaction stream, which materially shallows the data substrate. The 10-year strategic partnership preserves Clubcard Pay+ branding — but the data flows now route through Barclays. And data retention is GDPR-bounded: transaction-level Clubcard data is held for up to two years, not thirty. The doctrine is thirty years old; the raw data is bounded by law.

Conditions for the pattern

Four conditions distinguish a durable version of this pattern from a marketing claim.

Substrate. The operational substrate must be generative of behavioural data with continuous capture for at least five years per customer. Tesco satisfies this in doctrine if not in raw retention — thirty years of compounding strategy, two years of GDPR-bounded transaction data, much longer for aggregated patterns. A substrate younger than five years has not had time to compound.

Margin. Gross margins on the productized version must be materially higher than the core retail business. Tesco doesn't disclose, but the retail-media ROAS spread documented above implies materially better unit economics than the core 4% operating margin. Where the productized line cannibalises core economics rather than supplementing them, the math fails.

Doctrine. The productized capability must have been preserved through at least one CEO transition where it was tested. Tesco's 2015 Lewis sale-not-sold episode is that test. Without such a moment, doctrine claims remain unfalsifiable. The 2015 episode is what makes Tesco's claim credible rather than asserted.

Inflection. The AWS moment — when an internal team starts getting unsolicited inbound from external companies asking to buy what was built internally — must have actually arrived. Tesco's was 1995; Walmart's was 2024-2025. AWS moments are rare and recognisable in hindsight. dunnhumby was already a multi-client SaaS before Tesco bought it, which is why Tesco's inflection looks like a take-private rather than a build.

When three of four conditions are absent, the pattern is the wrong frame. When three are present and one is borderline, the borderline one is where the next twenty-four months of work belong.

References