Schwarz Gruppe

15

min read

Schwarz Gruppe — the privately held parent of Lidl and Kaufland, Europe's largest retailer at €175.4 billion in FY2024 revenue — has spent more than two decades building IT infrastructure for its own scale. Over the last three years, that infrastructure has been spun into Schwarz Digits and reframed as an external offering: STACKIT for sovereign cloud, XM Cyber for cybersecurity, and a $600 million anchor commitment to Cohere's Series E, conditional on the Aleph Alpha merger closing, for sovereign AI. The €11 billion Lübbenau data center, broken ground in November 2025, is the largest single investment in the company's history — nearly six times Schwarz Digits' current annual revenue.

The bet underneath all of this is that EU sovereignty regulation has turned operational IT capability itself into a sellable layer, and that a retailer with a €175 billion balance sheet can outlast pure-play cloud startups in a market US hyperscalers cannot structurally serve. When regulation makes jurisdiction a non-negotiable input, the IT substrate built for internal use becomes a product — and balance-sheet depth, more than cloud-native pedigree, decides who serves the new demand.

The substrate, not the data

The shape of this move is unusual for a retailer. The more familiar pattern is the one Walmart, Tesco, and dunnhumby have run for years: productize the outputs of operations. Loyalty data, sales data, shopper behavior, all repackaged and resold to suppliers and brands. The retail substrate generates data; the data is the external product.

Schwarz does not do this. Lidl Plus, with more than 100 million users globally, was connected to Meta and Google in March 2025 — not as a data product sold to other advertisers, but to improve Lidl's own ad targeting. There is no "Lidl Connect" advertising platform sitting on top of the loyalty footprint. There is no dunnhumby of discount. The customer data stays internal.

What Schwarz productizes is not the data but the substrate underneath it. The roughly 23,000 servers, 30 petabytes of storage, 1.4 million network ports, and 4,000 IT staff originally built to keep 14,200 stores running. The same compute, network, and storage capacity that powers Lidl's checkout systems and Kaufland's logistics is now sold — under the brand STACKIT — to the European Commission, the Dutch central bank, FC Bayern Munich, SAP RISE customers, and ARD's public broadcasters.

The distinction matters because the buyers and the moats are different. The retail-data-as-product play sells reach into a loyalty footprint to a CPG brand; the moat is the loyalty base. The substrate-as-product play sells jurisdictional control to a central bank or a ministry; the moat is regulation plus capex. Few companies can credibly do either — Schwarz happens to be one of perhaps three retailers globally whose internal IT operates at hyperscaler-adjacent scale.

And before the obvious comparison forms — didn't Amazon do this with AWS, start as a retailer and sell its own IT externally? — the shape rhymes but the moat does not. AWS is a scale moat, built into what was effectively a green field in 2006. STACKIT is a jurisdictional moat, built into a sub-market that regulation has carved out from a market scale alone cannot serve. Amazon's bet was that cloud would commoditize. Schwarz's is that jurisdiction will not. Different bets, different moats, different markets.

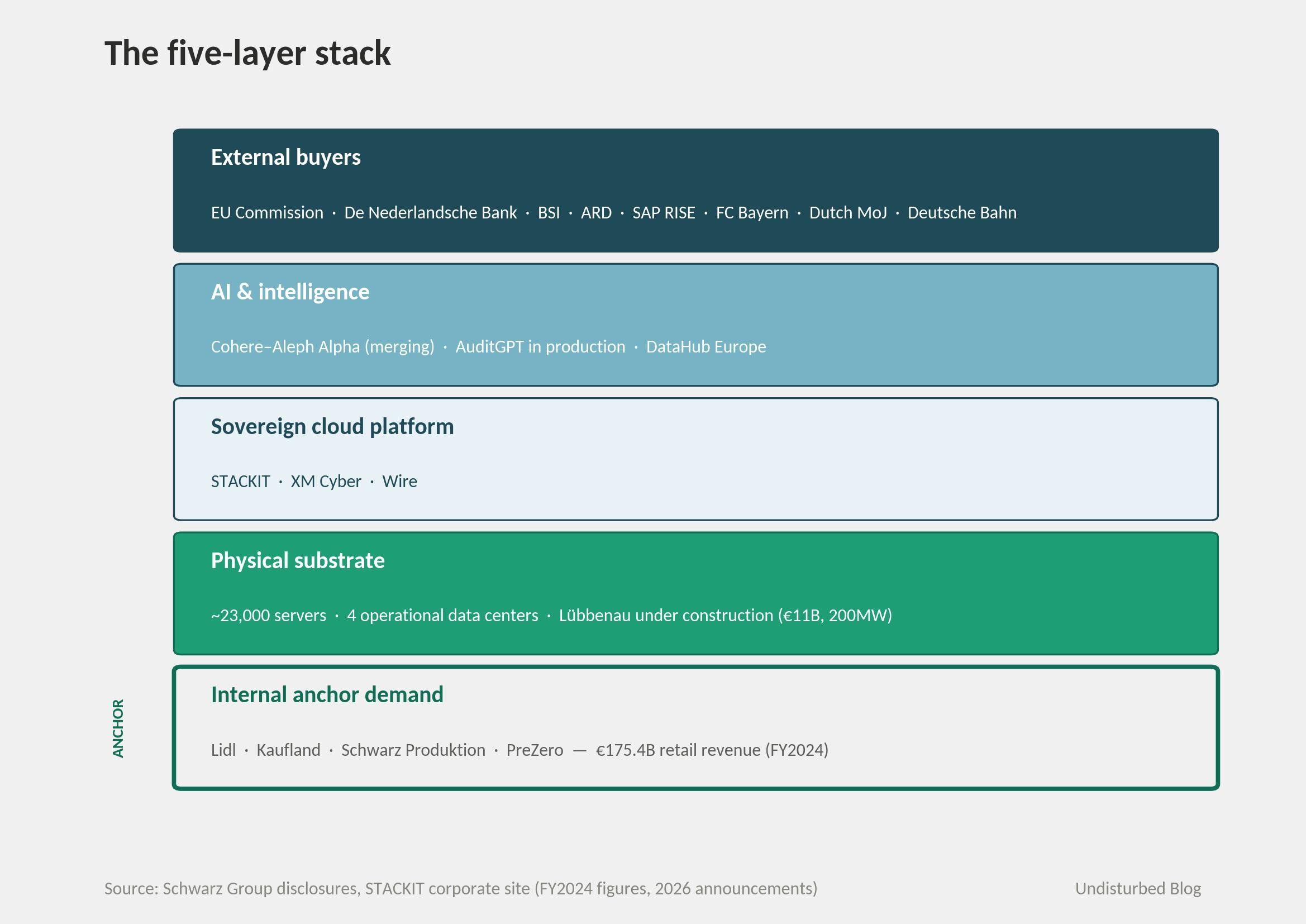

The strategy in one picture

The architecture stacks five layers. At the base sits the internal anchor demand — Lidl, Kaufland, Schwarz Produktion, PreZero, all funded by the €175 billion retail business. On top of that, the physical substrate: roughly 23,000 servers, four operational data centers, and the €11 billion Lübbenau campus under construction. Above the substrate, the sovereign cloud platform — STACKIT, XM Cyber, Wire. Above that, the AI and intelligence layer — the merging Cohere–Aleph Alpha entity, AuditGPT in production. At the top, the external buyers: the European Commission, De Nederlandsche Bank, BSI, ARD, SAP RISE customers, FC Bayern Munich, Deutsche Bahn, the Dutch Ministry of Justice.

The picture inverts the normal direction of two arrows. Most retailers buy IT from someone else; Schwarz built it. Most cloud providers built infrastructure for external customers first; Schwarz had a captive internal demand of 595,000 users — and the cash flows of Lidl and Kaufland behind them — before any external customer existed. Both inversions matter for what comes next.

Three closed loops

Loop 1 — The substrate loop.

Schwarz's internal IT operations needed scale that few European companies have. Four thousand IT staff operating roughly 23,000 servers across data centers in Germany and Austria gave the company an operating capability that nobody bought from STACKIT in 2018, when STACKIT was first stood up internally. By 2024, that same capability — extended, hardened, certified — was being sold to FC Bayern Munich and SAP. Each external customer raises utilization on infrastructure already built for internal use; each new customer also funds the next data center. The €11 billion Lübbenau campus does not have to be paid for by external revenue; it is paid for by the retail business. External revenue, as it grows, just makes the asset return better. The loop closes in the sense that internal scale created the substrate, the substrate became sellable, and external sales fund more substrate.

Loop 2 — The sovereignty loop.

The EU's Cloud Sovereignty Framework, finalized in October 2025, scores cloud providers across eight dimensions — strategic, legal, operational, environmental, supply-chain, technology, security, EU law compliance. US hyperscalers struggle with this framework structurally; AWS, Microsoft, and Google are subject to the US CLOUD Act through their parent companies. STACKIT, owned by a foundation registered in Heilbronn, is not. In April 2026 the European Commission awarded its €180 million sovereign cloud framework — the first significant public-sector procurement under the new rules — to four providers. STACKIT was one of two that won independently, without forming a consortium. The Dutch government followed with its own framework agreement weeks later. De Nederlandsche Bank — the Dutch central bank — signed in early November 2025. The German federal cybersecurity authority, BSI, signed a sovereign-cloud cooperation in March 2025. ARD's public broadcasters signed in August 2025. Each contract is small on its own; each contract becomes a reference for the next. Sovereignty validated becomes sovereignty reusable.

Loop 3 — The stack loop.

STACKIT alone is an infrastructure product, with the same kind of margin pressure as any IaaS provider. The third loop is what closes the value chain. In November 2023, Schwarz co-led Aleph Alpha's $500 million Series B alongside Bosch Ventures, SAP, and Hewlett Packard Enterprise — the bet at that point was that Aleph Alpha would become a European-grounded frontier-model competitor, the German answer to OpenAI. By mid-2024 that bet had quietly broken: Aleph Alpha conceded it could not match the training budgets of OpenAI, Anthropic, or Google, and pivoted away from frontier-model competition toward enterprise tooling. In April 2026, Cohere announced it would absorb Aleph Alpha at a combined $20 billion valuation — the 90/10 ownership split, with Cohere shareholders taking 90% and Aleph Alpha shareholders 10%, made the structure plain — and Schwarz committed $600 million to Cohere's Series E with deployment locked in on STACKIT. This is Plan B. Plan A was a German frontier model on European cloud; Plan B is a Canadian-anchored model on European cloud, same sovereign-deployment promise, different operator at the wheel. The combined entity will run on Schwarz infrastructure; Schwarz's customers get a sovereign AI option that an independent cloud provider cannot offer. AI workloads are GPU-hungry, which is why Lübbenau is being built for up to 100,000 GPUs — by comparison, the Deutsche Telekom–Nvidia data center under construction in Munich is targeting 10,000.

Each loop is closed in the sense that the next iteration improves on the prior one. There is no obvious step where a human has to make a buy-versus-build decision; the answer has already been built.

The numbers

The numbers tell a story with one obvious tension.

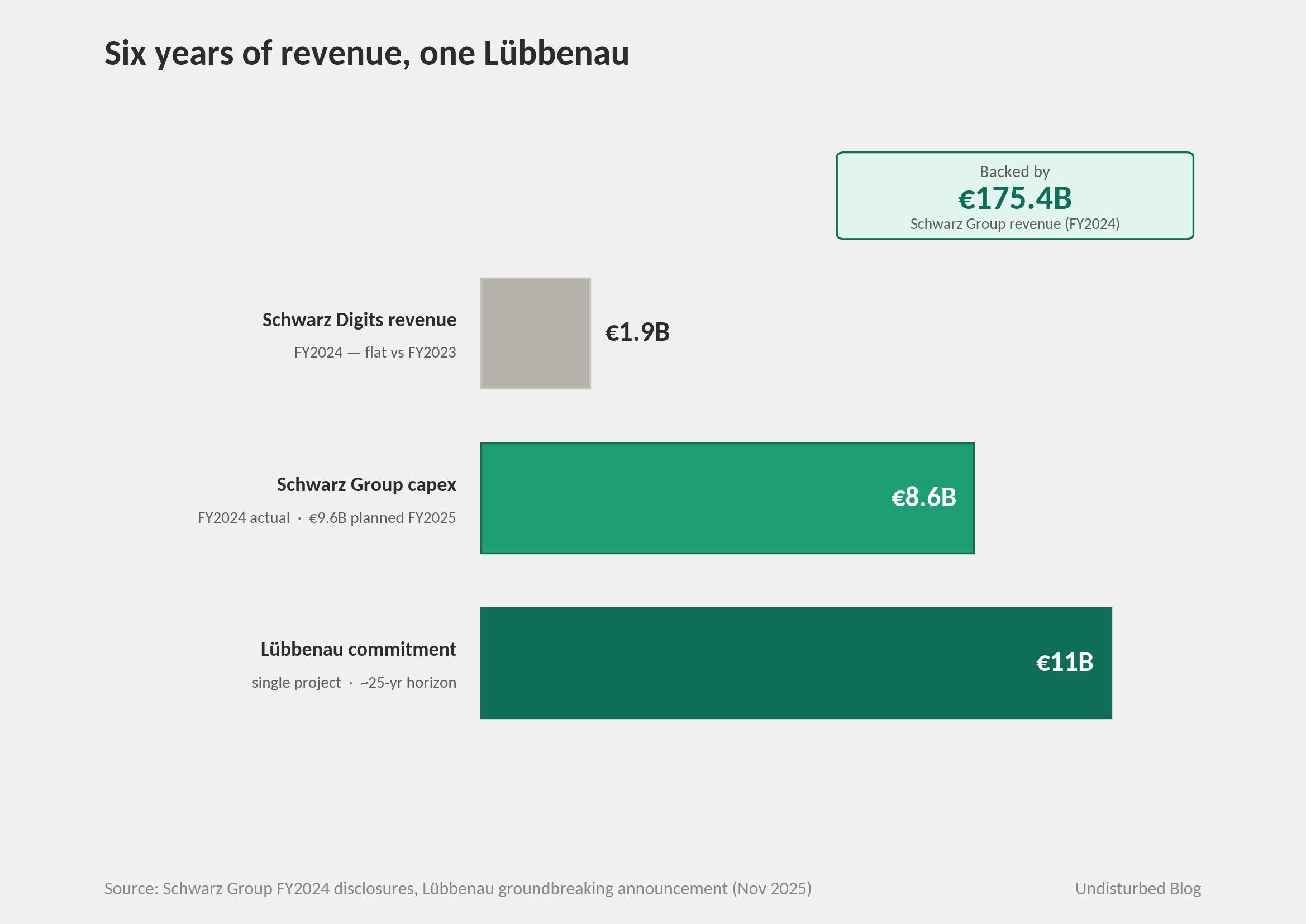

In FY2024, Schwarz Group revenue was €175.4 billion, up 4.9% — the slowest growth in over a decade. Lidl: €132.1 billion (5.3% growth). Kaufland: €35.2 billion (2.9% growth). Schwarz Produktion: €4.6 billion. PreZero: €3.9 billion. Schwarz Digits: €1.9 billion — flat versus FY2023.

The €1.9 billion is the headline number that sounds underwhelming. It is. It is also the wrong number to anchor on, because it includes both internal and external revenue, and because it is being grown asymmetrically: investment in the digital division has been moving aggressively while the revenue line stays flat. Group capex for FY2024 was €8.6 billion, planned €9.6 billion for FY2025 — a record. The single largest line item is the €11 billion Lübbenau data center, broken ground November 18, 2025; first phase completion targeted for end of 2027. The investment is, as the company itself notes, the largest single project in its history. Construction is €2.5 billion of that total; technology infrastructure inside the building is €8.5 billion. The site occupies 13 hectares of a former lignite power plant — chosen specifically because the existing 200MW grid capacity made it possible to skip years of transmission upgrades.

External validation has been moving faster than revenue, and it is stacked on a governance foundation laid in 1999:

April 2026 — STACKIT wins one of four EU Commission sovereign cloud contracts (€180 million ceiling, six years), one of only two independent winners alongside Scaleway

April 2026 — Cohere–Aleph Alpha merger announced at $20B combined valuation; $600M Schwarz Group commitment to Cohere Series E

November 2025 — Lübbenau groundbreaking, €11 billion data center

November 2025 — De Nederlandsche Bank signs framework

November 2025 — Dutch Ministry of Justice and Security framework (SLM Rijk)

August 2025 — Südwestrundfunk / ARD broadcasters cloud contract

March 2025 — BSI federal cybersecurity authority cooperation

November 2024 — Google Workspace migration for 575,000 Schwarz employees on STACKIT

October 2024 — SAP RISE deployment on STACKIT

September 2024 — STACKIT spun out as standalone GmbH & Co. KG

September 2023 — Schwarz Digits division formed, 7,500 employees at launch

November 2021 — XM Cyber acquisition for ~$700 million

2018 — STACKIT founded internally

1999 — Dieter Schwarz transfers 99.9% of group equity to the Dieter Schwarz Stiftung

Named program owners: Christian Müller and Rolf Schumann are co-CEOs of Schwarz Digits. Gerd Chrzanowski is General Partner of Schwarz Group, with operational accountability for the entire ecosystem. Dieter Schwarz himself, age 86, holds an honorary board seat with veto power but is not operational.

A pure-play cloud provider with €1.9 billion in stagnant revenue would be a venture failure — Eulerpool's blunt May 2025 read, "cloud division disappoints," captures the simple version of the bear case. Schwarz Digits is not a pure-play. The unit's measure of success is not its own quarterly P&L — it is whether the substrate can be used to anchor sovereign AI demand at scale. The €11 billion Lübbenau bet is roughly six years of Schwarz Digits revenue; no startup could carry that capex without diluting its way to insignificance. A retailer with €175 billion in retail revenue can.

The €1.9 billion is best read as a lagging indicator on a substrate strategy whose leading indicator is who has signed up — the EU Commission, the Bundesbank, the German BSI, ARD, SAP, Cohere — over the last 18 months. The honest counter-read: if the lagging indicator does not start moving by FY2026, the leading indicators will start to feel rehearsed.

The norm beyond the cloud product

The hard test for any AI strategy is whether it survives the founder. Schwarz passes this test in two ways.

First, the founder is already gone operationally. Dieter Schwarz left management in 1999 and transferred 99.9% of Schwarz Group shares to the Dieter Schwarz Stiftung the same year. Voting rights sit in a separate operating company, Schwarz Gruppe Industrietreuhand KG, which decides how much profit returns to the foundation. The foundation is tax-exempt under German law as long as a stated charitable purpose is maintained. The structure was designed in 1996–1999 specifically to prevent breakup of the retail business and to ensure operational continuity through generational transition. Twenty-six years on, it has held.

Second, the AI norm is broader than the cloud product. Schwarz Group internal employees — about 575,000 at the time of the announcement, growing past 595,000 by year-end FY2024 — were migrated to Google Workspace hosted on STACKIT in 2024. AuditGPT, an AI agent automating financial audit workflows, is in production at Deutsche Bahn and within Schwarz itself. The DataHub Europe initiative with Deutsche Bahn aggregates industrial and media data for compliant model training. There is a written internal "AI Codex" describing how AI is to be developed and deployed inside the group, including the conditions under which the group will partner with external AI vendors. Schwarz Impulse, an annual decision-maker conference held in October 2025 for the fourth time, brings German and European politicians and partners into conversations about digital sovereignty.

The succession test isn't really about whether Dieter Schwarz approves of the €11 billion Lübbenau bet — he isn't operationally involved, and the structure was set up so he wouldn't have to be. The actual test is whether the foundation governance, the operating partnership, and the dual-CEO structure of Schwarz Digits can hold a five-year capex curve through political turbulence and revenue lag. Three years in, the evidence says yes.

The structure itself is worth pausing on. Most discussions of AI strategy succession assume corporate continuity through public-market governance — boards, proxy votes, quarterly cycles. Schwarz uses an older, slower mechanism: a charitable foundation as legal owner. The structure removes short-term return pressure entirely. €11 billion over six years is impossible to justify on a quarterly P&L; it is straightforward to justify on a 30-year mission. The pattern transfers poorly to public companies — but transfers very well to other family-owned European industrial groups. There is a class of EU sovereign-AI buyers and operators — Bosch, Bertelsmann, Carl Zeiss, foundation-owned and patient — that public-market analysts systematically underweight, and foundation governance is the structural reason.

Why this answer fits Schwarz

Schwarz has always been a vertical integrator. The doctrine is visible across the group: Schwarz Produktion supplies a meaningful share of what Lidl and Kaufland sell — €4.6 billion in 2024, up 9.5% year-over-year. PreZero handles the group's recycling. Schwarz Immobilien owns the property. Schwarz IT now operates the cloud. The default answer at Schwarz when something becomes critical is "build it ourselves and run it ourselves" — the same hard-discount logic Karl Albrecht used at Aldi, applied to every layer of the stack.

The doctrine is also expressed in the foundation structure itself. By placing 99.9% of equity in a tax-exempt foundation in 1999, Schwarz removed the option of being acquired or going public. Long-horizon capex — like a data center that pays back over 25 years — becomes structurally easier than for any publicly-listed retailer. Tesco does not have this option; Walmart does not have this option. Schwarz does.

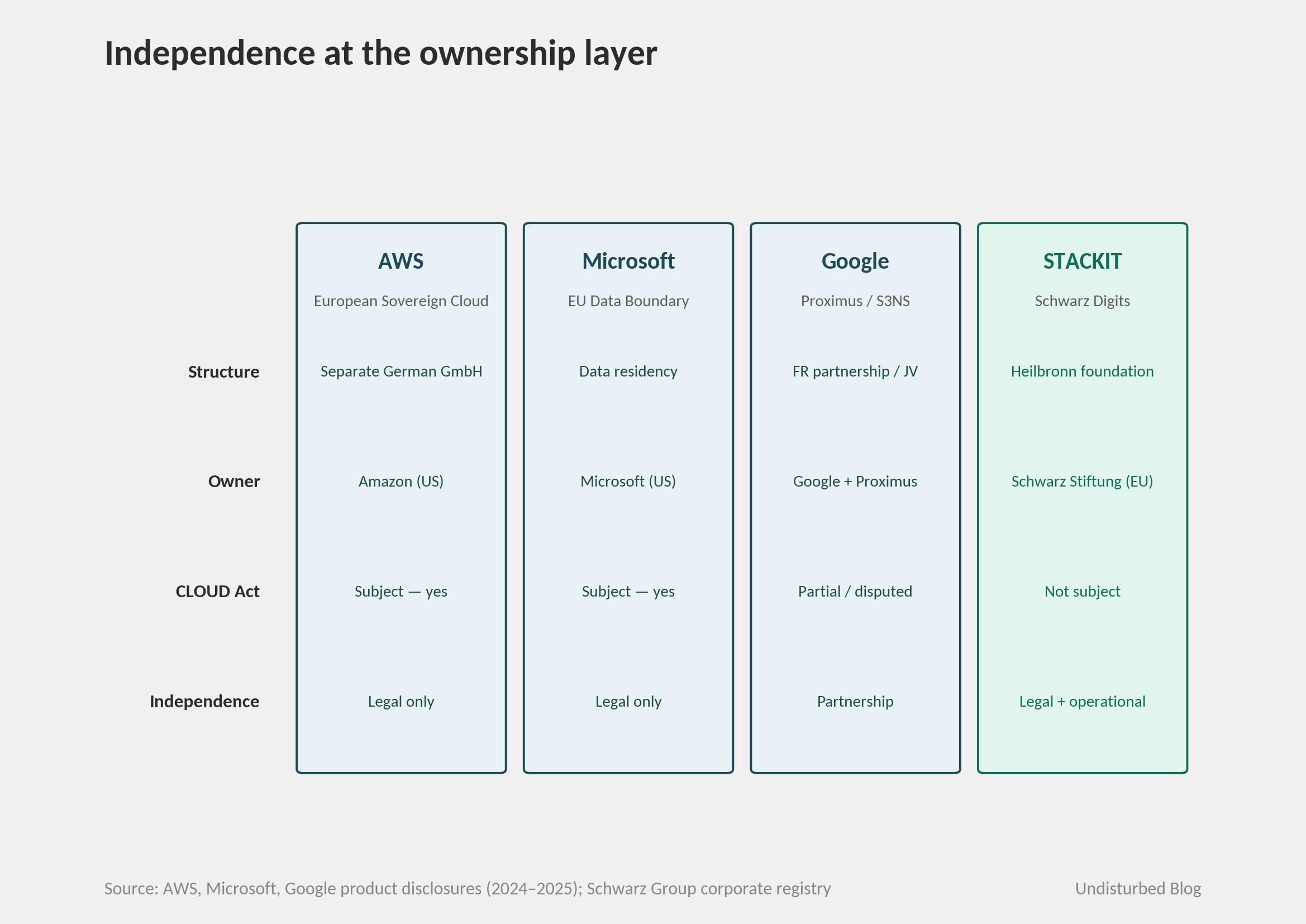

The inflection is regulatory. The EU Cloud Sovereignty Framework, finalized in October 2025 and used for the first time in the Commission's April 2026 award, is the first procurement instrument that explicitly excludes providers whose parent is subject to non-EU jurisdiction. AWS, Microsoft, and Google are not categorically excluded — they can partner with European operators, as Google did with the Proximus/S3NS consortium that won part of the same tender — but the framework rewards providers whose operations are independent at the legal layer. Schwarz, owned by a Heilbronn foundation, is structurally compliant in a way an American hyperscaler is not. The framework would not have made STACKIT relevant in 2018; it makes STACKIT structurally advantaged in 2026.

Other companies have the architecture. T-Systems has data centers. OVHcloud has scale. Scaleway has GPU infrastructure. None has Schwarz's activation energy. T-Systems is part of Deutsche Telekom, a publicly-listed telco where €11 billion of single-site capex against flat segment revenue would not survive a quarterly review. OVH is publicly traded; its market capitalization is roughly an order of magnitude smaller than the Lübbenau project's announced cost. Scaleway sits inside Iliad Group but operates at a fraction of Schwarz's substrate scale. Schwarz has both architecture (existing IT scale, brownfield site with inherited 200MW grid capacity) and activation energy (a foundation-owned €175 billion retail base that can absorb a flat-revenue digital division through six years of capex). The architecture transfers — somewhat. The activation energy mostly does not.

Where it goes next

Before the trajectories, the load-bearing counter-thesis. The strongest argument against everything above is that US hyperscalers are not standing still. AWS announced its European Sovereign Cloud in 2024, structured as a separate German legal entity (AWS European Sovereign Cloud GmbH) with European board members, European staff, and European data residency. Microsoft's EU Data Boundary went into general availability in 2025 — workloads, customer data, support tickets, and system-generated logs all kept inside the EU. Google has the Proximus/S3NS construction in France and parallel arrangements under discussion in Germany. The pressure Schwarz is responding to is the same pressure US hyperscalers are responding to, and they have ten times the capital to throw at the response.

What Schwarz still has, that the hyperscaler responses do not, is independence at the ownership layer. AWS European Sovereign Cloud GmbH is still wholly owned by Amazon; Microsoft EU Data Boundary still sits under a US parent subject to the CLOUD Act; the Proximus/S3NS structure is a partnership, not a divestiture. The EU's October 2025 framework rewards exactly this gap — providers whose operations are independent at both the legal and operational layer, not just one. If Brussels weakens the framework's operational-independence test, the moat narrows fast. If Brussels holds the line, Schwarz's structural advantage compounds. The next 24 months will tell which way the framework drifts in practice.

Three things to watch over that period.

First, Lübbenau Phase 1 completion in late 2027. The first three modules will provide the initial 200MW capacity and accommodate the first GPU clusters. If on schedule, this gives STACKIT compute capacity at a tier that puts it adjacent to — though still well below — AWS's European footprint. If late, it pushes the substrate thesis into 2028 and gives competitors a window. Watching construction milestones at Lübbenau is the single best leading indicator on whether the bet is on track.

Second, the Cohere–Aleph Alpha close, expected H2 2026, subject to regulatory approval in Canada, Germany, and the EU. The combined entity is targeting deployment on STACKIT as a flagship reference. If the integration delivers, Schwarz becomes one of perhaps three EU-grounded operators offering a full sovereign stack — substrate, platform, AI — to regulated buyers. If the merger stalls or the political coordination between Berlin and Ottawa frays, Schwarz still has a working cloud, but loses the AI-layer narrative that lets it compete on something other than IaaS pricing.

Third, the €1.9 billion digital division revenue line. Schwarz reports its FY2025 figures in May 2026. If Schwarz Digits revenue starts moving — even modestly — the substrate-as-product thesis is validating commercially, and the €11 billion bet earns a quarter more credibility. If the line stays flat through another fiscal year while capex accelerates, the foundation governance starts being tested in a different way: not on whether it can hold the bet, but on whether holding the bet remains the right call.

The pattern only works if the regulatory inflection lasts long enough for the substrate to mature. That is not under Schwarz's control, and it is the load-bearing assumption underneath everything else.

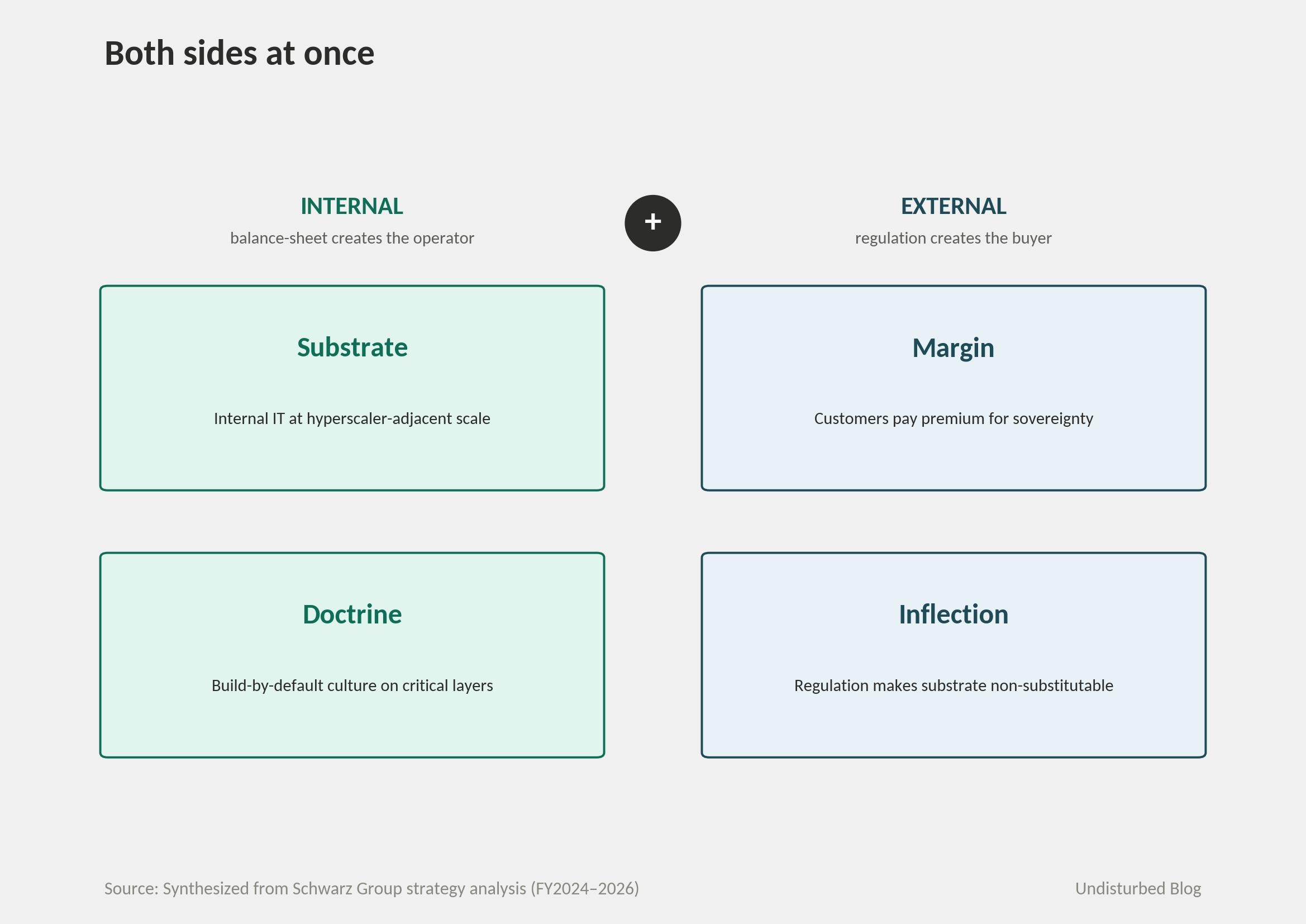

The four conditions for substrate-as-product

The pattern is rare for a reason. Four conditions have to align before substrate productization works as a strategy, and Schwarz happens to satisfy all four.

Substrate. The first condition is that internal IT operates at a scale where serving external customers is plausible without a years-long rebuild. Most companies fail this test in five seconds — their IT exists at the size needed to run their own business, no larger. Schwarz did not fail it. The 23,000 servers and 4,000 IT staff that exist to run Lidl and Kaufland sit at a tier that overlaps with the smaller end of hyperscaler operations.

Margin. The second condition is that customers in the same jurisdiction will pay a premium for what has already been built internally. STACKIT's premium over AWS is not technical — Schwarz has never argued its compute is faster or its tooling broader. The premium is jurisdictional. It exists because the EU's October 2025 sovereignty framework reshaped the demand curve for regulated buyers, not because the product got better.

Doctrine. The third condition is that the organization's instinct on critical capabilities is to build rather than to buy. The substrate-as-product move is unnatural for buy-by-default companies; it is natural for build-by-default ones. Schwarz's culture had been pointing in this direction for fifty years before STACKIT existed — Schwarz Produktion, PreZero, Schwarz Immobilien are all evidence of the same instinct applied to non-IT layers.

Inflection. The fourth condition is a regulatory shift that makes the substrate non-substitutable. Sovereignty in cloud, jurisdictional handling for data, supply-chain residency requirements — these are the obvious cases. Less obvious: medical device data, financial settlement, defense compute, energy grid telemetry. The principle is that regulation, not technology, sometimes reshapes which substrate is sellable.

Two of the four are external; two are internal. Regulation creates the buyer; balance-sheet creates the operator. Companies that have only the external pair build a stack and find no buyer for what they built. Companies that have only the internal pair build a stack and run out of patience before the buyer arrives. Schwarz sits on both sides at once, which is rare — and the foundation structure is what keeps the patience funded when the revenue lags.

References