UPS

14

min read

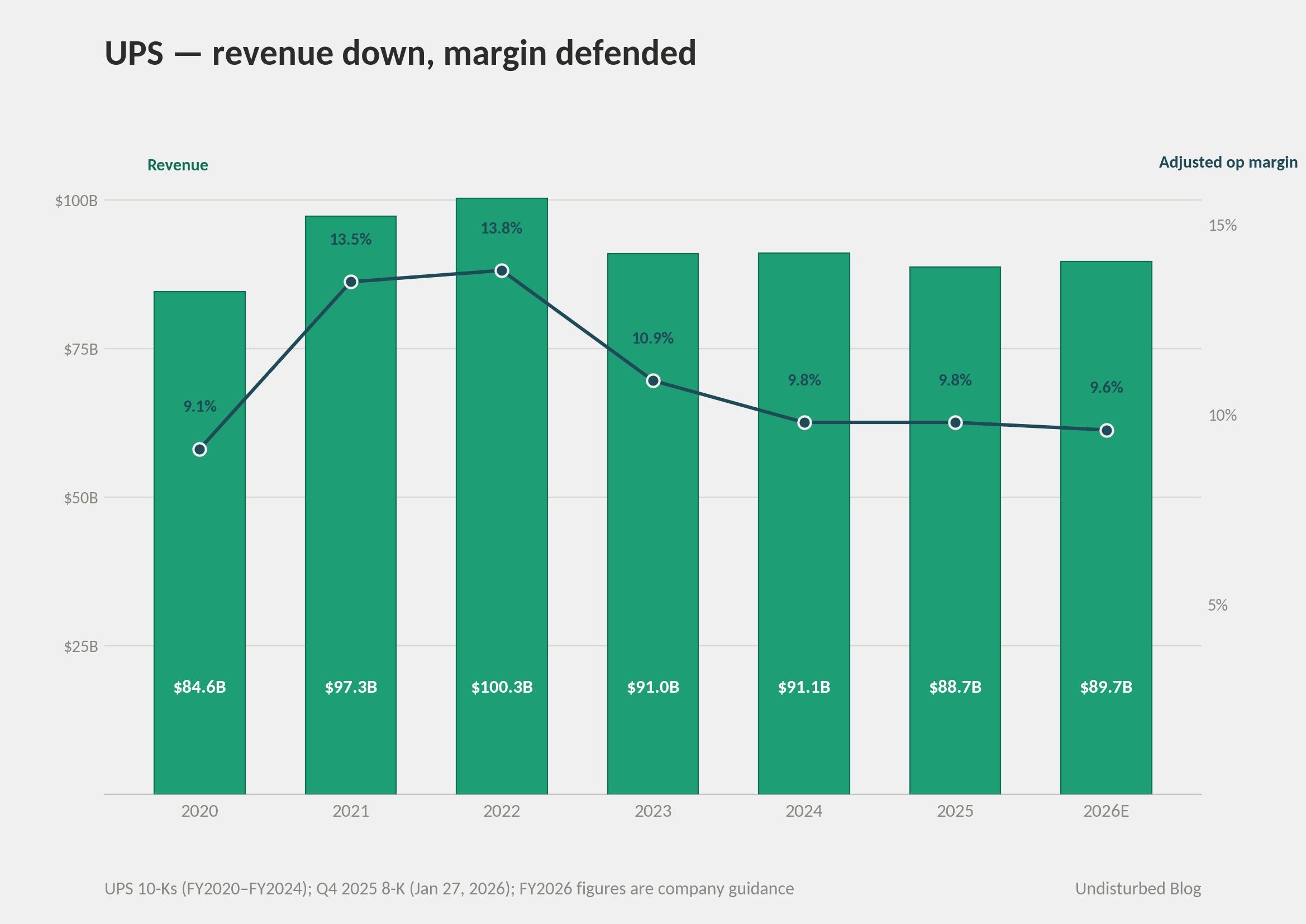

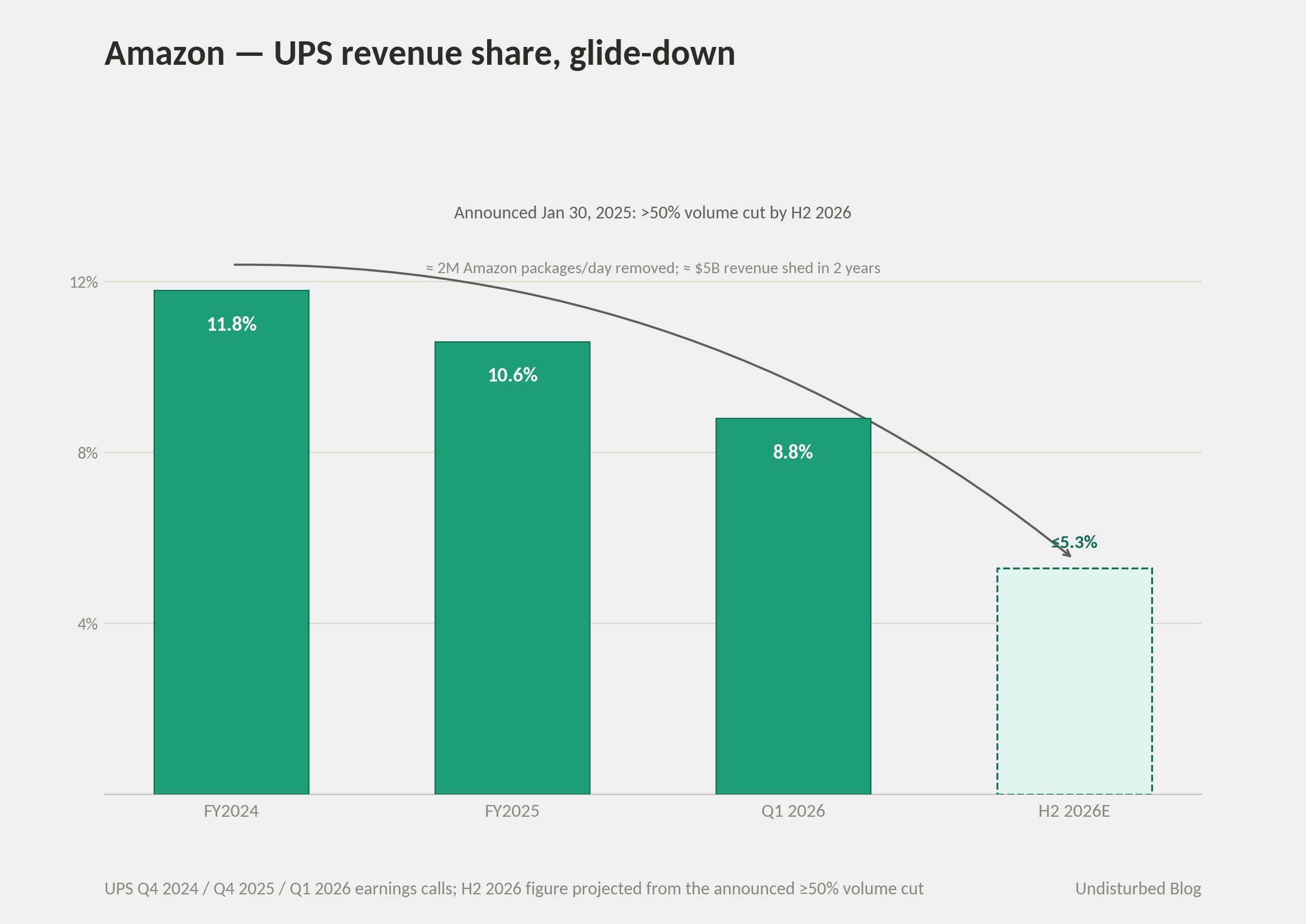

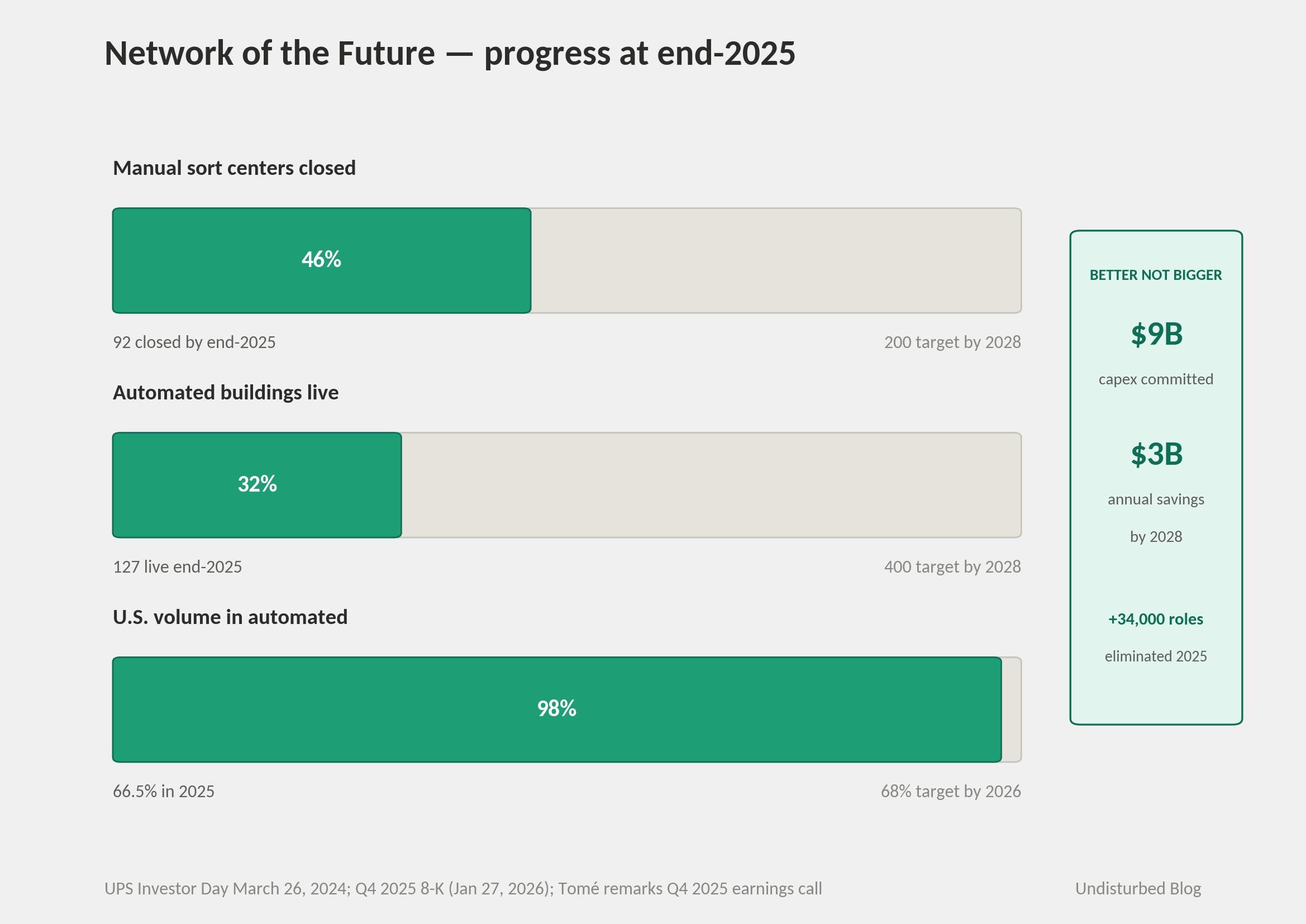

When Carol Tomé became UPS's first external CEO on June 1, 2020, she inherited a 22-year algorithmic stack and a strategic question that had been deferred for at least a decade: how does a logistics network bigger than any competitor's stop competing on volume and start competing on what the volume produces? The answer that has emerged over six years is unusually concrete. Volume is being compressed. Margin is being expanded. Amazon — 11.8% of UPS revenue in 2024 — is being cut by more than half by the second half of 2026, trading roughly $5B in revenue for U.S. revenue per piece up 6.6%. About 200 manual sort centers will close by 2028; 400 automated buildings will replace them under a $9B Network of the Future program targeting $3B in annual savings. ORION, the routing engine that has dispatched 55,000 U.S. drivers since 2016, now runs on top of a Network Planning Tools (NPT) digital twin and a Smart Package Smart Facility (SPSF) RFID layer that, by April 2026, reaches every U.S. delivery vehicle and facility. FY2025 closed at $88.7B in revenue and a 9.8% adjusted operating margin; FY2026 guidance is roughly $89.7B at 9.6%.

The strategic posture is what UPS calls "Better not Bigger," and it is what the operating numbers describe. The harder thing to describe is what makes it work. Companies that build durable AI advantage in mature industries don't compete on the algorithm and don't compete on the data. They compete on the closed loop between the two — algorithm built in-house, trained on operational exhaust no one else can produce, feeding back into the same network it optimizes. Algorithm as thought, data as cage.

The Strategy in One Picture

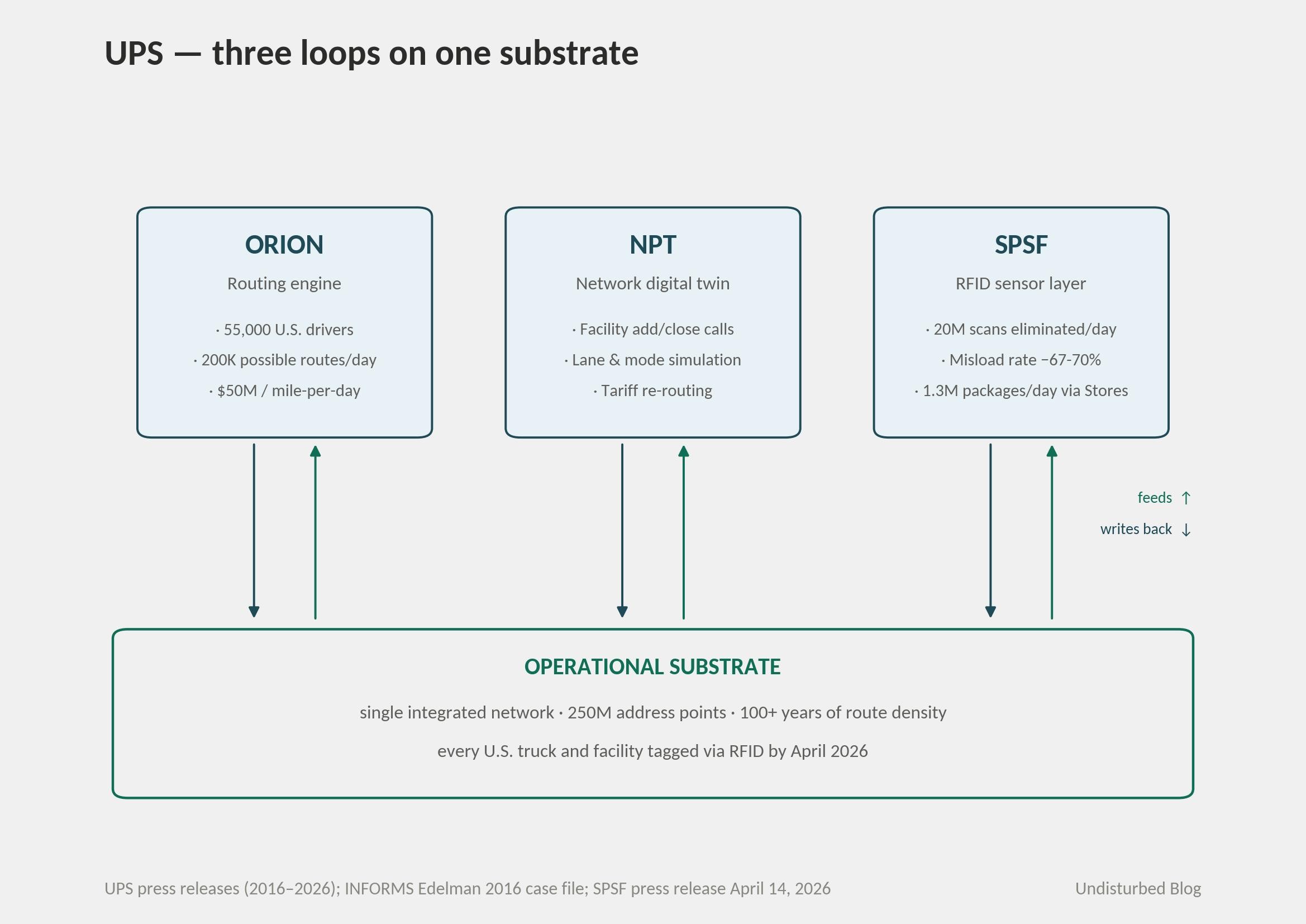

UPS itself doesn't call its strategy "algorithm as thought, data as cage." The official framing is "Customer First, People Led, Innovation Driven," with "Better not Bigger" as the strategic posture and "Network of the Future" as the build-out program. But three systems sitting on top of one operational substrate is the more interesting way to read it.

Read it left to right and the strategy reads itself. The substrate is the moat. The three systems are not three products — they're three windows into one decision engine running on one corpus. ORION decides the micro flow (which stop sequence per driver). NPT decides the macro flow (which hub, which lane, which mode). SPSF feeds both with high-resolution package events. Each system writes back into the same substrate the others read from.

The pattern only works if the algorithm is built in-house and the data can't be replicated elsewhere. Buy the algorithm and the loop opens. Outsource the data and the cage dissolves.

The moat sits on the data side, not the algorithm side. ORION's mathematical core — vehicle routing on a giant graph with time windows — is taught in any operations research program. UPS could publish the code tomorrow and the moat wouldn't move. What can't be published is 22 years of address-level package telemetry from a single integrated network that no other company has ever operated. The lesson for AI strategy in mature industries isn't "build the smartest model." It is to identify the operational data the company produces that no competitor can produce, and then build the algorithm that learns from it. The algorithm is the thought; the data is the cage that makes the thought defensible.

How It Actually Works — Three Closed Loops

Loop 1: ORION and Dynamic ORION

Research started in 2003 inside UPS's internal Operations Research group, building on Package Flow Technologies (PFT, deployed 2003, 85 million miles a year saved on its own). ORION's first field test was Gettysburg, Pennsylvania, in 2008. Eight pilot sites in 2010-2011, six beta sites in 2012, official launch in 2013, full deployment to 55,000 U.S. drivers by the end of 2016. About 1,000 pages of code, 250 million address data points, an average of about 200,000 possible routes per driver per day, server bank in Mahwah, New Jersey. INFORMS gave it the 2016 Edelman Award — the Super Bowl of operations research practice. Build cost: $250M. Engineering hours, per Jack Levis (the program lead, retired): roughly 17 million.

The closed loop in operation is daily. Package Flow Technologies predicts volume and pre-loads the package car. ORION ingests the stops plus DIAD telemetry plus customer service commitments plus traffic plus map corrections drivers entered the day before. It outputs a sequenced manifest. UPSNav, deployed December 2018, gives the driver turn-by-turn directions down to loading-dock-level entry points. The driver executes; GPS, scan, and time-stamp telemetry pour back into the substrate overnight. Maps and route heuristics improve. Across 55,000 drivers, the loop closes every day.

Dynamic ORION, announced in January 2020 and deployed across 2020-2021, replaced static day-start manifests with real-time re-optimization. Per UPS, Dynamic ORION saves an additional 2-4 miles per driver per day on top of the original ORION's 6-8. The canonical Levis number — and one of the more widely cited ROI claims in 21st-century operations research — is that each mile per driver per day removed is worth roughly $50M annually to UPS. The 2016 figures: 100 million miles a year removed, 10 million gallons of fuel, 100,000 metric tons of CO₂, $300-400M in operating cost. By Levis' own post-retirement estimate, the ongoing benefit is closer to $500-600M a year.

Loop 2: Smart Package Smart Facility

Concept work in 2019, first ~100 facilities in 2022, full U.S. distribution-site rollout by mid-2023. The architecture has four waves. Smart Facility puts RFID readers at sortation and loading points, eliminating manual barcode scans during the load-into-truck step. Smart Package Car puts RFID readers in delivery vehicles — 60,000 by end of 2024, the rest in 2025, every U.S. package vehicle by April 2026. Smart Driver shows the driver exactly where any tagged package is on the truck. Smart Customer pushes RFID labels back to the point of origin: every UPS Store location prints them by end of 2025, processing 1.3 million RFID-labeled packages a day through that channel alone.

The numbers are blunt. Twenty million manual scans eliminated per day. Misload rate down 67-70%. Cost-per-piece in automated facilities is 28% lower than in conventional ones. Investment to date: more than $100M.

The reason this matters for the cage isn't the throughput improvement — it's that every package, every truck, every facility, every retail counter is now a sensor writing back into the same substrate ORION and NPT consume. UPS is the first major logistics operator to do this across an integrated network at this scale. FedEx's RFID is scoped mostly to high-value and healthcare shipments; the substrate isn't comparable.

Loop 3: Network Planning Tools

NPT, with its sibling HEAT (Harmonized Enterprise Analytic Tool), is a real-time digital twin of UPS's global network — facilities, lanes, modes, packages, weather. The canonical use case is the February 2021 winter storm: NPT routed volume around impacted hubs and minimized service degradation. Then-CIO Juan Perez framed it on the way out the door: "It allows us to actually have visibility as to how packages and shipments move across the network across multiple modes." His successor as the public face of UPS technology, Satyan Parameswaran (President, IT), put it more sharply — once you have a digital twin, you depart from the world of static reporting.

What NPT decides: where to add a facility, where to close one, what to simulate before changing the physical network, how to re-route during a tariff regime change (used during 2025's trade-policy shifts). The 200 sort-center closures inside Network of the Future aren't intuitions from operations leadership. They're outputs of the digital twin reading the substrate ORION and SPSF feed.

ORION decides per driver. NPT decides per network. SPSF tells both what's actually happening. The algorithm runs the company.

The Numbers

Better not Bigger as a strategy is most legible in what UPS gave up. Revenue went from a $100.3B peak in 2022 to $88.7B in FY2025. Adjusted operating margin held at roughly 9.8%. Adjusted EPS came down from a peak — $9.73 in FY2024 — to $7.16 in FY2025, with FY2026 guidance roughly flat. Capex stepped down: $5.4B in 2020, $3.9B in 2024, ~$3.0B planned for 2026. Free cash flow (adjusted) has been $5.1-6.3B across the Tomé era.

The Amazon decision is the clearest single number. Announced January 30, 2025 on the Q4 2024 call: more than 50% volume reduction by H2 2026. Amazon was 11.8% of UPS revenue in 2024, 10.6% in 2025, 8.8% by end Q1 2026. By the end of June 2026, UPS will have removed roughly two million Amazon packages a day and shed about $5B in revenue inside two years. The trade is visible in unit economics: 2025 U.S. average daily volume down 7%, U.S. revenue per piece up 6.6%.

Network of the Future is the matched supply-side cut. $9B in capex, 63 sites with major automation projects, target 400 automated buildings, $3B in annual savings by end of 2028. As of Q4 2025: 127 automated buildings live, 24 more coming in 2026, 66.5% of U.S. volume already flowing through automated facilities, 68% target by end of 2026. About 200 manual sort centers will close by 2028 — 30 closed in 2023, 40 in 2024, 22 announced in early 2026, 24 more identified for the first half. In 2025 alone, 93 buildings ceased daily operations and 34,000 operational roles were eliminated, generating $3.5B in cost savings. Tomé's framing on the Q3 2025 call: "the most significant strategic change in direction in UPS's history."

Healthcare is the deliberate offset. Revenue grew from roughly $10B in 2023 to more than $11B in 2025, with $20B targeted for 2026. Q1 2026 was UPS's first $3B healthcare quarter. The supporting M&A stack — Marken (2016), Bomi (2022), MNX (2023), Frigo-Trans plus BPL (early 2025), Andlauer Healthcare Group ($1.6B, closed November 1, 2025) — moved UPS's healthcare-logistics presence into 14 new countries.

Each program has a named owner. ORION, originally Jack Levis. NPT and the broader digital stack, Bala Subramanian, EVP and Chief Digital and Technology Officer (a role created for him in June 2022, hired from AT&T). Network of the Future, Nando Cesarone, EVP and President U.S. — the operations leader executing the 200-facility consolidation. The CFO seat, Brian Dykes (Brian Newman was CFO during the 2020-2024 transition). The CEO, Carol Tomé.

The canonical ORION figures — $300-400M annually, 100 million miles, 10 million gallons of fuel — are from 2016. UPS hasn't refreshed the ORION-only number publicly since. The most recent specific figure ($500-600M/year) comes from Levis after he retired, not from the company. This is not an oversight; it is structural. ORION, Dynamic ORION, NPT, and SPSF have become so deeply intertwined that pulling out a clean ORION-only number isn't analytically possible anymore. When a successful AI program stops producing standalone ROI updates, the right question isn't whether it stopped working. It is whether it dissolved into the operating model. DRIVE at FedEx still has a clean line item. ORION at UPS has become the company.

Is AI a Norm Inside UPS?

ORION is not a pilot in one department. It is the way 55,000 U.S. drivers — and another 11,000 across North America and Europe — are dispatched. UPSNav is on the DIAD they hold, the sixth generation of an in-house handheld UPS has been iterating since 1991. NPT runs simulations before management makes facility-consolidation calls. SPSF data flows into customer service, into commercial conversations, into AI-assisted email response. The substrate writes to all of them.

The diagnostic that matters most is what changed for the driver. Before ORION, success was measured against last year's average for the route. After ORION, it is measured against ORION conformance — the algorithm sets the baseline, the driver executes, and variance from ORION is what management reads. The KPI itself moved one layer up. That is the deepest signal that an AI program has crossed from initiative to norm: the metric itself moves. The algorithm is no longer competing for relevance with human judgment; it has become the baseline human judgment is graded against. Most "AI initiatives" fail at exactly this seam. After two years of deployment, if the sales team is still measured against last year's quota and the operations team against last year's throughput, the algorithm hasn't become the org chart yet. It is still optional. UPS made it mandatory.

Other AI surfaces are layered on top of the same substrate. DeliveryDefense scores roughly 2% of addresses that drive more than 30% of shipping losses; Subramanian's framing at the March 2024 Investor Day was explicit — "we will be using unique data that only UPS can aggregate for our customers to help unlock value," which restates the closed-loop logic in one sentence. Message Response Automation (MeRA), a generative-AI agent on UPS's roughly 52,000 customer emails a day, cut agent handle time by half in pilot. Asset Health does predictive maintenance on the vehicle and aircraft fleet. AI is now in the customs and tariff-routing decisions — used quietly during 2025's trade-policy turbulence.

The doctrine continuity is unusual. UPS's operations research group dates to the late 1990s digitization push under then-CEO Jim Kelly. PFT shipped in 2003. ORION 2008-2016. UPSNav 2018. NPT mid-2010s through today. SPSF 2019-2026. Dynamic ORION 2020. There is no gap in the cadence — and no pivot, either. The same group that built the routing engine built the digital twin built the RFID rollout.

Above all of it sits Jim Casey's 1947 "A Talk with Joe" speech, which UPS still teaches. The phrase is "constructive dissatisfaction." The institutional translation is: the network is never optimal, the algorithm is never finished, and the data is always the next bottleneck.

Why This Answer Fits UPS (and Won't Transplant Cleanly)

UPS was founded August 28, 1907 in Seattle by Jim Casey, age 19, and Claude Ryan, age 18, with $100 borrowed. By 1913, the company was running motorized delivery. By 1916, the brown — Pullman Brown, chosen to hide dirt — was the brand. By 1922, common-carrier authority. The key structural choice came early: a single integrated network where Express and Ground share trucks, sorts, drivers. That one decision compounds across decades.

The OR institutionalization came later but on the same substrate. The late-1990s digitization drive under Kelly — Levis quotes the framing as "this isn't good enough; take information out of people's heads, put it into databases, build a data model" — produced PFT (2003), then ORION (2008-2016), then NPT, then SPSF. The Make-or-Buy pattern reads cleanly: own the physical network, build the algorithm in-house, buy commodity layers (vehicles, retail real estate, healthcare cold-chain) and let the algorithm cage them with proprietary data. UPS has acquired aggressively — 26 transactions per Tracxn, mostly healthcare and last-mile gig — and has never outsourced its routing brain.

What makes 2020-2026 the inflection isn't any single pressure. It's that four pressures arrived together, the way they did at FedEx earlier in the decade but in a different configuration. New leadership: Tomé's June 2020 arrival as the first external, first-female CEO, with no ego invested in the prior strategy. Cost-structure pressure: the 2023 Teamsters contract — five years through July 2028, $30B in "new money," wages roughly twice peers per ShipMatrix's Satish Jindel. Customer-concentration risk that looked like a native-tech competitor: Amazon at 11.8% of revenue, building its own logistics network in parallel, eroding UPS margin from inside the customer base. Integration mandate, inverted: unlike FedEx, UPS didn't need to integrate Express and Ground — it had been one network for a century. The mandate was the opposite. Make it smaller. Network of the Future closes 200 buildings and pushes volume into 400 automated ones. The same program type, executed in reverse polarity.

The 100-year cage is what doesn't transfer. Address-level density data across 250 million points and 100+ years of single-network operation — FedEx had to merge Express and Ground in June 2024 just to start producing the comparable substrate. The DIAD ecosystem is six generations of in-house handhelds, not a vendor product. The OR depth is a multi-decade institutional capability, with INFORMS leadership, an Edelman win, and named program owners across decades. None of these are buyable.

Consider the thought experiment. Suppose UPS handed FedEx the ORION codebase, the data schema, and the deployment guide tomorrow. FedEx couldn't run it. Not because of legal exposure — because ORION's heuristics presuppose a single integrated network where one truck does both Express and Ground, where left turns are systematically expensive, where address density follows a 100-year accretion curve. FedEx didn't merge Express and Ground until June 2024. Its address density is fragmented across two prior network footprints. ORION's left-turn aversion would mis-fire on a network that doesn't yet have ORION's assumed topology. Architecture is import-able. Doctrine is not. Most "just buy the AI tool" strategies fail at exactly this seam — the tool assumes a substrate the buyer doesn't have.

Activation energy is what makes the moment actionable; architecture is what makes the moment defensible. UPS has both right now in the same configuration. Most logistics companies have neither.

Where It Goes Next

Three trajectories worth watching. First, ORION's next layer — UPS has been signaling agentic AI as the natural extension, with Subramanian and others framing it as decision augmentation rather than agent replacement. The substrate is ready; what's unclear is the deployment cadence. Second, the build-out of Network of the Future toward the 2028 finish line: 400 automated buildings, $3B in annualized savings, 200 manual sort centers closed. The Pickle Robot deal — about 400 truck-unloading robots for roughly $120M, deployment late 2026 into 2027 — is an early signal. Third, the healthcare line: $11B in 2025, $20B targeted in 2026, with Andlauer ($1.6B, November 2025) the largest in-Tomé-era acquisition. Possibly more Asia or EU healthcare M&A.

The risks are visible. Q1 2026 results showed transitional cost drag — U.S. domestic adjusted op margin at 4.0% versus 7.0% a year earlier on $350M of one-time costs (MD-11 lease costs after the November 2025 Louisville crash and full fleet retirement, Ground Saver insourcing, weather, casualty). The November 4, 2025 crash that killed 15 people accelerated the retirement of all 26 MD-11s and forced an unplanned $137M after-tax write-off. The replacement aircraft — 18 Boeing 767s — won't all arrive until 2027. The margin recovery thesis is unproven through full peak 2026.

Two structural questions sit further out. Will agentic AI on top of ORION/NPT/SPSF reduce the human-in-the-loop count further than current Network of the Future plans assume? And does the FedEx-UPS comparison hold — does the single-network with deep algorithmic embedding doctrine continue to outperform the separated-layer fast-iteration doctrine across an industry cycle? Both companies will be readable on this question by 2028. UPS is betting yes.

FedEx, in the same decade and the same industry, has arrived at the opposite doctrine: separation, four layers running on different clocks so the fast layers don't disturb the slow ones. UPS's bet is the inverse — one substrate, deep algorithmic embedding, the algorithm running the company rather than running on top of it. The two largest U.S. parcel carriers have settled on opposite answers to the same problem. That contrast is the more interesting fact than either strategy taken alone.

When This Pattern Holds — Four Diagnostic Conditions

The case forces four diagnostic questions about when the pattern holds. They map to the four conditions that have to be present for this kind of closed loop to be real rather than aspirational.

The substrate test. Companies that hold a defensible AI position in mature industries produce operational data their competitors structurally cannot generate. UPS produces 250 million address points across a single integrated network, accreted across 100+ years. A data lake is not a cage; it is storage. The cage is data the algorithm needs and the rest of the industry cannot produce.

The algorithm test. The thinking layer is built in-house in every case where the closed loop holds. UPS uses Esri for some mapping but built its own ORION map of 250 million points. The vendor map is an input; the model is internal. Where the algorithm that runs the operation is licensed, the moat belongs to the vendor.

The doctrine test. The algorithm has become the metric, not an option alongside it. The cleanest test of organizational normalization is whether operators are graded against the algorithm's output rather than against last year's. UPS made the transition deliberately when ORION conformance replaced historical route-average benchmarking. Where management still grades against last-year baselines after two years of AI deployment, the doctrine hasn't shifted.

The timing test. Four pressures arrive together: new leadership without ego invested in the prior strategy; cost-structure pressure from labor or capital; customer or competitor erosion of margin from a quarter that is hard to ignore; and a clear mandate to reshape the network. UPS has had all four since 2020. Where three of four are absent, this pattern doesn't get past committee. Where all four are present and the company is not moving, the window is closing faster than the boardroom thinks.

References