UnionPay

14

min read

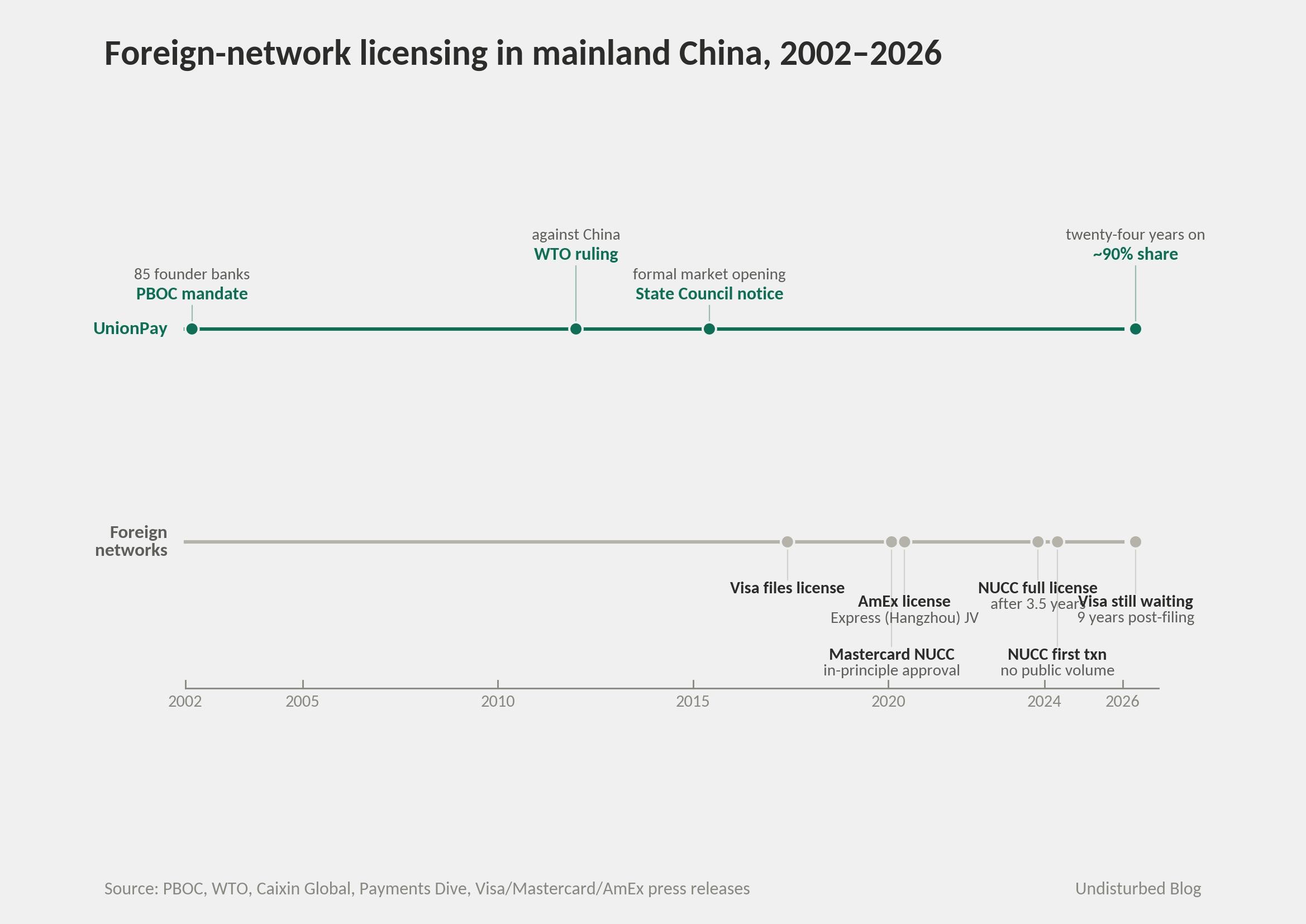

UnionPay holds an estimated 90% of mainland China's yuan card clearing market in 2026, after twenty-four years of nominal opening. American Express through a joint venture got the first foreign clearing license in 2020. Mastercard through its NetsUnion JV processed its first domestic transaction in May 2024. Visa filed in 2017 and is still waiting. The substrate is guaranteed by statute, not won by competition. UnionPay's 2023 revenue was RMB 47.24 billion at roughly 30% net margin — the only public financial cut, surfaced inadvertently through a 0.021% equity-share auction by China Telecom. There is no investor day, no published services-revenue line, no Chief Services Officer. Its 2025–2026 AI moves — the APOP agentic-payment framework launched April 3, 2026; the Nihao China inbound-tourism super-app launched December 19, 2025; AI-generated fraud rules disclosed at "85% accuracy" by Chairman Dong Junfeng at Davos — are real but framed as national-infrastructure stewardship and Belt-and-Road interoperability, not as a productized services franchise.

That last absence is the thesis. When substrate is mandated rather than competed for, the productization pattern that defines Visa and Mastercard becomes optional. UnionPay neither fuses to its rail (the Visa case, where deep services integration is the natural moat) nor federates around it (the Mastercard case, where adjacent buyer-set expansion is the only way to grow services faster than the substrate). It runs the rails, builds the international flag, and invests in just enough AI infrastructure to stay technically credible. Read against the two competitive networks, UnionPay is the negative test that confirms the positive cases: federation and fusion are responses to competitive pressure on the substrate. Strip out the competition — by statute, by charter, by institutional structure — and the doctrine collapses to something simpler. Operate the network. Expand the channel. Leave services monetization to whoever has to fight for revenue.

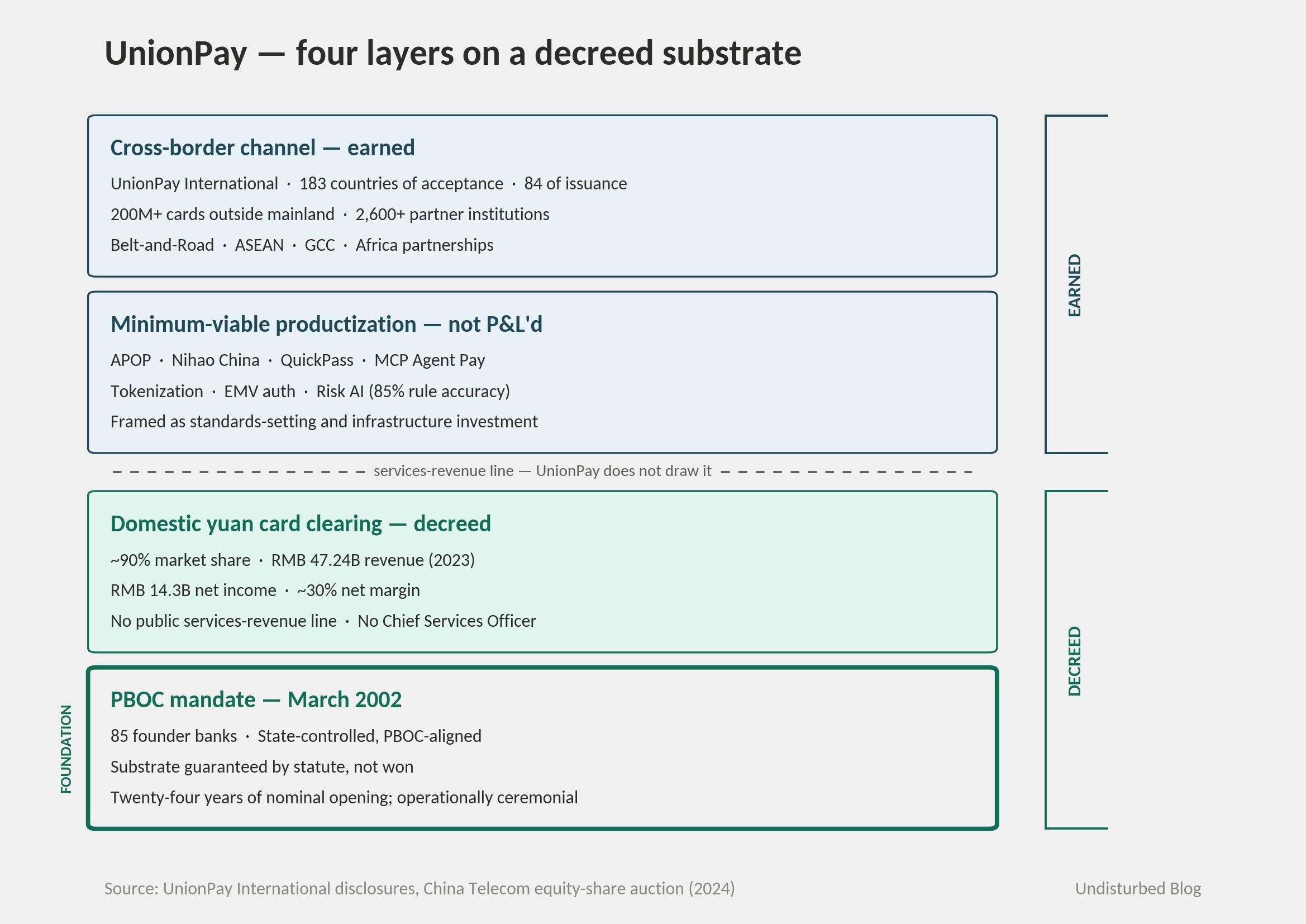

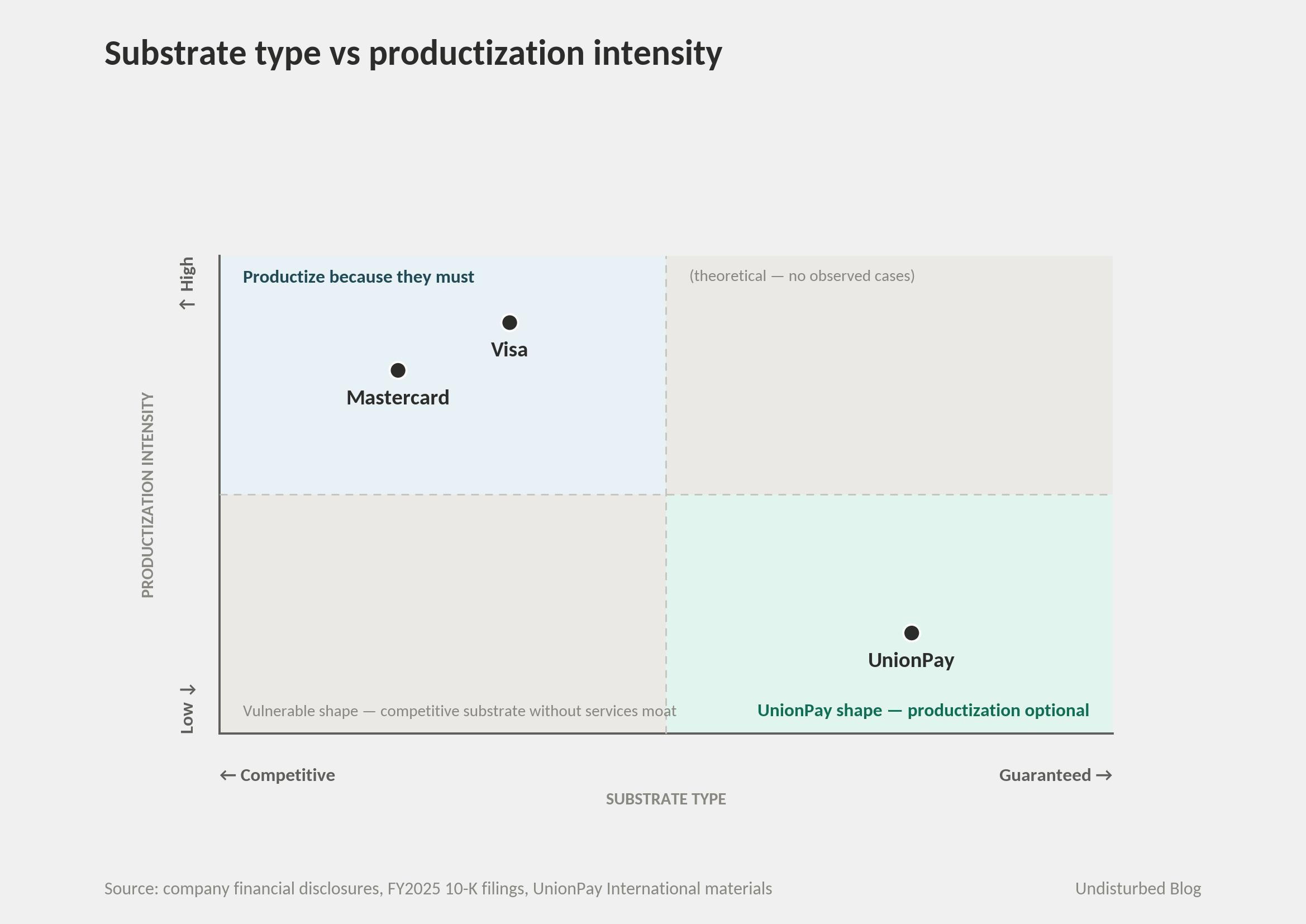

The strategy in one picture

The architecture has four layers stacked on a single regulatory foundation. PBOC's March 2002 mandate established UnionPay as the sole yuan card switch, with eighty-five founder banks. On top of that mandate sits domestic clearing — ~90% market share, the RMB 47.24B revenue line, the ~30% net margin. Above that is a minimum-viable productization layer (APOP, Nihao China, QuickPass, MCP Agent Pay, tokenization, risk AI) that is real but never P&L'd as a services franchise. And at the top is the cross-border channel — UnionPay International's 183-country acceptance, 200M+ cards outside mainland, 2,600+ partner institutions, anchored to Belt-and-Road, ASEAN, and GCC corridors.

Three things are worth reading off the picture. The bottom layer is regulatorily guaranteed, not commercially won. The middle layer is what would be the productization layer in Visa or Mastercard — small, real, and not P&L'd as a services franchise. The top layer is geopolitical channel-building positioned as state-aligned infrastructure work, not commercial moat-building. Visa fuses to its rail. Mastercard federates around its rail. UnionPay does neither — because it doesn't have to.

How it actually works — three closed loops

Visa's loops culminate in services revenue feeding back into network economics. Mastercard's culminate in token-as-a-service for AI agents and recurring SaaS uncorrelated with card volume. UnionPay's culminate in volume protection, channel expansion, and infrastructure adequacy — and stop there.

Loop 1 — Mandate → Volume → Margin

The 2002 PBOC mandate gave UnionPay a monopoly on yuan card clearing. The 2012 WTO ruling against China and the 2015 State Council notice formally opened the market; the operational reality has been ceremonial. AmEx's Express (Hangzhou) JV got the first foreign clearing license in June 2020 and launched co-branded RMB cards in 2021 with no disclosed material volume. Mastercard's NetsUnion JV received in-principle approval in February 2020, full license in November 2023, and processed its first domestic transaction in May 2024 — three years of ambition to reach "millions of locations" with no public volume disclosure that would suggest above-1% share. Visa filed for a license in 2017 and is still waiting.

Industry estimates put UnionPay's mainland yuan card clearing share at ~90% in 2026. The only public financial calibration is the 2023 revenue of RMB 47.24 billion at RMB 14.3 billion net income surfaced through China Telecom's auction of a 0.021% equity stake — a ~30% net margin consistent with a regulated near-monopoly clearing utility, not a services-led franchise. The loop is closed by structure: substrate is decreed, volume follows, margin is high, capital is reinvested into more substrate.

Loop 2 — Belt and Road → International acceptance → Geopolitical channel

The only "earned" volume UnionPay has is cross-border. UnionPay International's 2025–2026 deal cadence reads exactly like a state-aligned infrastructure operator's ledger: China-Vietnam QR interoperability with NAPAS in April 2025; UAE Jaywan co-badged cards in February 2025; Malaysia CIMB MoU in May 2025; Indonesia ASPI/QRIS partnership; Korea GLN; Spain/Portugal Getnet through Santander in November 2025; Brazil Banco do Brasil; Uzbekistan Uzcard/HUMO; Kyrgyzstan IPC; Nepal FonePay; Austria Bluecode at the November 2025 Global Partners Conference with eleven cooperation documents and seventy-two institutions present.

Footprint: 183 countries of acceptance, 84 of issuance, 200M+ cards outside mainland, 2,600+ partner institutions, ~6.7M QR-accepting merchants in 45 countries. This is real reach. But the framing in Dong Junfeng's Davos remarks (January 2026) is "trusted ties, shared success" and "key livelihood link," not "fee monetization." The loop converts mandate-protected domestic margin into international channel work, which serves renminbi internationalization and Belt-and-Road policy goals more than it serves a P&L.

The most telling 2026 development is on the other side of this loop. On February 3, 2026, at Web Summit Qatar, Visa announced a Visa Direct integration with UnionPay International's MoneyExpress remittance platform — Visa now plugs into UnionPay's substrate for China-bound flows rather than competing with it. The terminal scene of three networks: when substrate is mandated, the right strategy for the competitive networks is to integrate, not displace.

Loop 3 — Infrastructure investment → Minimum-viable productization → Standards-setting

This is the loop most often misread as "UnionPay is doing what Mastercard is doing." It isn't.

UnionPay's 2025–2026 AI products are real. The APOP framework launched April 3, 2026, with a live Hong Kong taxi-booking transaction via the Evonet AI assistant on the Hoppa platform; the framework specifies four capability layers — agent identity lifecycle, intent management, single sign-on, payment authorization — and is positioned as an open standard. The MCP Agent Payment Service supports conversational request-to-payment. The Nihao China app, launched December 19, 2025 at the China International Travel Mart, ships AI-driven inbound-tourism functionality for foreign visitors with multilingual NLU, real-time route planning across 43 cities, 160-currency conversion, and 300+ online platform integrations including Meituan, Ele.me, Ctrip, and JD.com. The intelligent risk-control system Dong Junfeng cited at Davos generates expert risk rules at "85% accuracy."

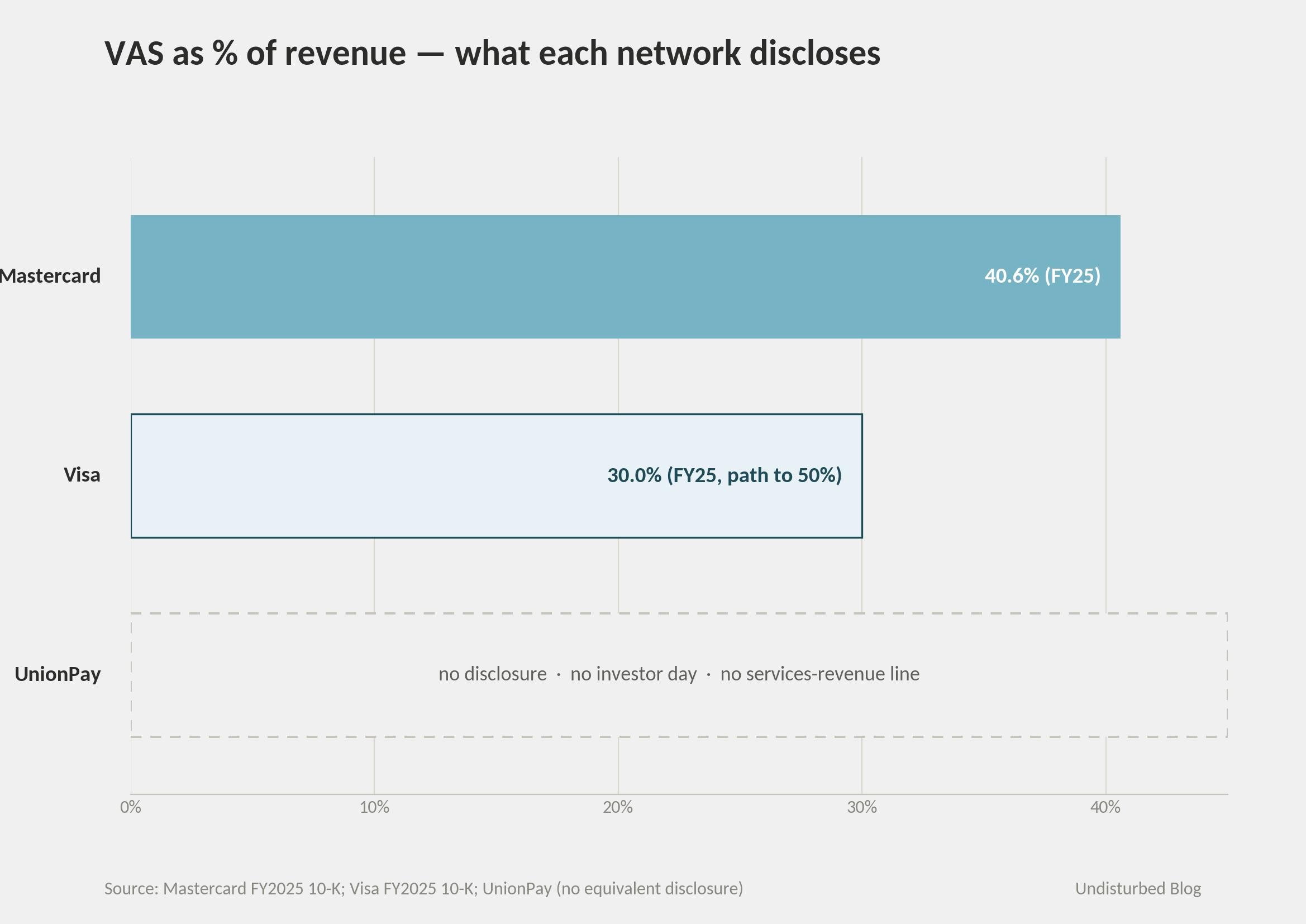

But these are not federated brands sold as a services franchise. APOP is positioned as standards-setting and Belt-and-Road interoperability, the way ITU specifications get positioned. Nihao China is positioned as "actively responding to the national call to improve convenience of inbound tourism" — policy alignment, not product-market fit. Risk AI is described as ecosystem capability, not a Decision Intelligence Pro analog sold to issuers globally. Mastercard's disclosure that 60% of its value-added services revenue is "network-linked" has no UnionPay equivalent because there is no UnionPay services revenue line to be linked or unlinked. The loop closes on infrastructure adequacy, not external monetization.

The three loops together do something specific. Loop 1 protects volume. Loop 2 expands channel. Loop 3 maintains technical credibility. Nowhere is there a "data → product → external services revenue" arc — which is precisely what defines the productization pattern in Visa and Mastercard.

The numbers

The data section in a UnionPay piece looks different from the Visa or Mastercard piece, and the difference is itself the diagnostic. Where Mastercard discloses VAS revenue at 40.6% of FY2025, currency-neutral organic growth of 18%, named program owners by function, and quarterly investor calls that calibrate services intensity to the third decimal, UnionPay discloses none of these. The closest thing to a financial disclosure is the 2023 cut from China Telecom's equity-share auction — RMB 47.24B revenue, RMB 14.3B net income, RMB 333.7B total assets, ~30% net margin. Beyond that, third-party aggregators (Nilson, RBR, Statista, CoinLaw) supply most of the visible numbers.

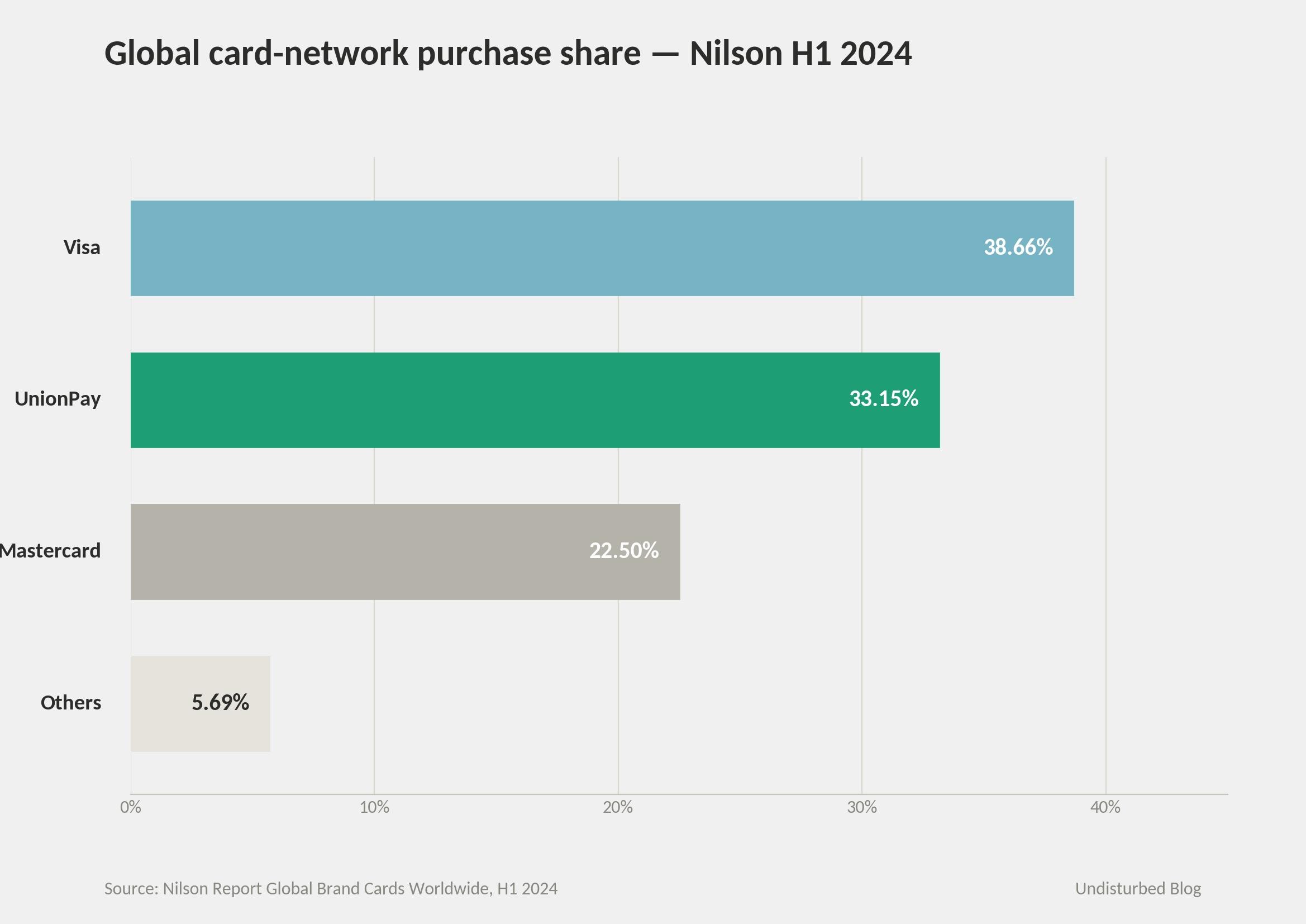

The market-share numbers, where they exist, are stark. Mainland yuan card clearing: ~90% UnionPay share post-2015 deregulation. Mobile payments: Alipay ~54% / WeChat Pay ~42% / UnionPay QuickPass distant third with ~50M MAU on a ~240M registered base, against Alipay's ~1.4B global MAU and WeChat Pay's ~935M China users. Globally on cards: Nilson H1 2024 puts UnionPay at 33.15% of global purchase transactions versus Visa's 38.66% and Mastercard's ~21–24%; the 2022 Nilson disclosure was that UnionPay overtook Visa as the world's largest debit-card brand at ~40% global debit share. Card transaction value (the most-cited 2017 disclosure) was RMB 93.9T / US$14.95T; CoinLaw's 2025 estimate of US$23.4T is directionally plausible but unaudited. International acceptance: 183 countries / 84 countries of issuance / 200M+ cards outside mainland / 2,600+ partners.

The e-CNY numbers, where UnionPay sits as commercial-bank switching infrastructure: 3.48B cumulative transactions and RMB 16.7T (~US$2.37T) by end-November 2025, with the January 1, 2026 framework reclassifying wallet balances as deposit money paying interest. mBridge cumulative cross-border volume reached US$55.5B by late 2025, with e-CNY representing ~95% of settlement volume.

The named individuals are a confirmed roster after the January 2025 leadership transition disclosed by Caixin and corroborated through subsequent UnionPay materials. Dong Junfeng (董俊峰) is Chairman and Party Secretary of China UnionPay, having moved over from chairing NetsUnion Clearing Corp; he is the public face at Davos, the Boao Forum, and the ASEAN-GCC-China Forum. Guo Dayong (郭大勇) is Vice Chairman, President, and Deputy Party Secretary, a former central-bank official. Larry Wang is CEO of UnionPay International. Shao Fujun transitioned from Chairman to Director. Hao Zhe, Hu Haozhong, and Tu Xiaojun are Executive Vice Presidents. The roster is intelligible to anyone reading Chinese SOE press; what is structurally missing is a Chief Services Officer or equivalent. There is no UnionPay analog to Mastercard's Craig Vosburg.

The cleanest empirical evidence for the no-productization thesis is the disclosure asymmetry itself. A network that needs to monetize services discloses them; a network that runs services as infrastructure investment does not. Mastercard tells investors that VAS is 40.6% of revenue, ~18% organic, ~60% network-linked. Visa tells investors VAS is ~30% with a stated path to 50%. UnionPay tells investors nothing — because it has no investors, no public earnings call, no ARR-style services framing. The contrast is not that UnionPay is hiding numbers. It is that the numbers do not exist as a managed disclosure category, because the strategy does not require them to. The absence is the punchline.

Is AI a norm inside UnionPay?

The question for UnionPay is the same one used for Mastercard: structural accountability, substrate depth, and product breadth across buyer segments. Applied here, the answers are different in instructive ways.

Structural accountability is dispersed, not concentrated. APOP, Nihao China, MCP Agent Payment Service, and the intelligent risk-control system live across UnionPay International, the domestic clearing entity, and PBOC-aligned working groups. There is no single executive whose career maps to "owns the services franchise." Dong Junfeng's public framing positions him as steward of national payment infrastructure rather than as services champion. The org chart presupposes infrastructure stewardship, not productized services.

Substrate depth is real but narrower than Mastercard's. UnionPay runs tokenization, EMV-standard auth, biometric, and intelligent risk control across the mainland card-clearing rails. The "85% accuracy" of AI-generated risk rules disclosed at Davos is the closest thing to a Decision Intelligence Pro public datapoint. But the depth is in the rails, not in a federation of acquired brands. There is no UnionPay equivalent of Recorded Future, Brighterion, Finicity, or Ekata. Nothing has been acquired and rebranded into a productization layer.

Product breadth across buyer segments is also narrower. Mastercard ships eight productized AI lines into multiple segments — issuers, acquirers, governments, enterprises, SMBs, AI platforms, developers. UnionPay ships APOP and risk AI to FIs, MCP Agent Payment Service to AI platforms, Nihao China to consumers, QuickPass to consumers and merchants. The catalog exists. It is not on the trajectory of an investor-facing services franchise.

The honest conclusion is that AI is a norm inside UnionPay in the infrastructure sense — Dong Junfeng's claim at Davos to be a "leading application-driven AI practitioner in the financial sector" is defensible at the rails level. It is not a norm in the Mastercard sense of a productized, P&L'd services franchise with a single accountable executive. The doctrine doesn't require that. It requires that AI keeps the rails technically credible and gives the cross-border channel work modern tooling. Both are happening.

Inside the same country, the comparison that lands hardest is UnionPay versus Ant Group. Ant — running Alipay without a substrate guarantee, having to win consumers and merchants — produces the Bailing/Ling LLM family (open-source Ling-1T trillion-parameter in October 2025; Ling-2.5-1T and Ring-2.5-1T in February 2026), the Zhixiaobao consumer AI assistant, the Maxiaocai financial agent, Alipay Tap! NFC adoption hitting 100M users in eleven months, and the MultiSafePay acquisition in January 2025 for international expansion. UnionPay produces APOP and Nihao China. Same regulatory environment, same banking system, same labor pool — and a totally different productization trajectory because Ant had no substrate guarantee. The doctrine emerges where competitive pressure exists; it doesn't emerge where the pressure is absent.

Why this answer fits UnionPay

Three things had to be true at the same time for the no-productization doctrine to hold, and they are.

The first is DNA. UnionPay was operationalized out of the 1993 Golden Card Project under Jiang Zemin and stood up by PBOC governor Dai Xianglong in March 2002 as a consortium of eighty-five commercial banks. The founding logic was standardization — replacing fragmented bank-card incompatibility with a unified switch — not commercialization. Twenty-four years later, the founding logic is still recognizable in every annual UnionPay International press release that emphasizes "interoperability," "openness," and "global connectivity." The DNA is infrastructure stewardship, not platform productization.

The second is doctrine. Through three chairmen — Liu Tinghuan, Su Ning's transitional period, Shao Fujun, and now Dong Junfeng — the publicly stated priorities have been the same: domestic clearing reliability, cross-border channel expansion, support for renminbi internationalization, and now CBDC infrastructure. The doctrine has been remarkably consistent, partly because it is shaped by PBOC priorities rather than CEO discretion. The closest thing to "productization" UnionPay has expressed is technical-standards setting (APOP positioned as an open protocol; QR-code interoperability with ASEAN partner wallets; e-CNY POS acceptance integration). Even that is framed as standards work, not service monetization.

The third is institutional shape. UnionPay is not a listed public company. It has no quarterly earnings call. Its net margin (~30% in 2023) is high enough that there is no commercial pressure to find new revenue lines. Its customer base — the eighty-five founding banks plus the broader Chinese banking sector — are also its shareholders. PBOC's regulatory and ownership influence means UnionPay's job is national-infrastructure stability and renminbi internationalization, not shareholder return. There is no listed-equity multiple to defend with services-mix shift; there is no investor day to use as a productization-doctrine showcase.

Three networks, three doctrines, one industry. Visa fuses to its rail because that rail is the largest in the world and competition makes deep services integration the natural moat. Mastercard federates around its rail because the rail is sub-scale relative to Visa, and adjacent buyer-set expansion is the only way to grow services faster than the substrate. UnionPay does neither because the substrate is mandated, and the commercial pressure that produces the other two doctrines is absent. The interesting comparator is not substrate size — UnionPay's substrate is comparable in volume to Mastercard's — but substrate type. Mastercard's substrate is competitive; UnionPay's is guaranteed. That single difference flips the doctrine. The organizing principle that connects the three cases is that productization intensity scales inversely with substrate guarantee. Visa and Mastercard productize because they must; UnionPay does not because it doesn't.

The lesson for non-mandate companies — which is most companies — is that the productization pattern is contingent on competitive substrate. If a regulator, a charter, or an institutional structure protects volume, federation and fusion become optional. If that protection ever weakens, the doctrine has to be built fast — and it cannot be retrofitted in eighteen months.

Where it goes next

Three trajectories will tell whether the substrate guarantee is actually softening over the next eighteen months.

The first is foreign-network domestic share. Mastercard NUCC has been processing for two years and has not disclosed material domestic share. Visa is still waiting on a license nine years after filing. The signal to watch is not licensing announcements (those are political) but disclosed volume share. If foreign networks reach even 5% of mainland yuan card clearing, the substrate guarantee starts to weaken and UnionPay would face genuine commercial pressure for the first time. The expected trajectory in the absence of geopolitical realignment is that share moves slowly enough that the doctrine doesn't shift.

The second is the e-CNY trajectory after the January 1, 2026 deposit-money reframe. e-CNY's RMB 16.7T cumulative volume by November 2025 is significant; the January 2026 framework introduces interest payment on wallet balances and reclassifies them as commercial-bank deposit liabilities. If e-CNY adoption accelerates and substitutes for card clearing rather than for Alipay/WeChat, UnionPay's mandate substrate gets thinner. If it substitutes for Alipay/WeChat, UnionPay's role as commercial-bank switching for e-CNY actually strengthens. Q1–Q3 2026 data will show which path the trajectory follows.

The third is APOP's external adoption. If APOP is adopted only by Chinese FIs and Belt-and-Road partner schemes, it confirms the standards-setting framing — UnionPay extending state-aligned interoperability rather than monetizing a global agentic-payment service. If APOP gains material adoption from non-Chinese networks, AI labs, or U.S./European banks, the framing shifts and UnionPay starts to look more like Visa and Mastercard, with a productized services franchise emerging from a standards-setting beachhead. The most informative eighteen-month signal will be whether OpenAI, Google, or Anthropic add APOP to their agentic commerce stacks alongside Visa's Trusted Agent Protocol.

The risk on the other side is that the U.S. secondary-sanctions environment around Russia and adjacent jurisdictions tightens further, and UnionPay's international acceptance work has to pull back. UnionPay's behavior since 2022 — quietly throttling cooperation with Russian SDN-listed banks, openly limiting overseas use of Gazprombank UnionPay cards after November 2024 sanctions — suggests UPI is run with commercial caution about international acceptance integrity. If sanctions tighten further and the cross-border channel work has to retrench, the second loop in the doctrine narrows and UnionPay becomes more purely a domestic infrastructure operator. That would not change the no-productization conclusion; it would deepen it.

The diagnostic — when does the doctrine apply?

The analytical value of reading three networks together — Visa fusing, Mastercard federating, UnionPay doing neither — is that it generates a diagnostic for any company asking whether services productization is necessary or optional. Four conditions separate the companies that have to productize from the ones that don't.

The first is substrate type. Companies whose volume is competitively contested have to productize; companies whose volume is regulatorily, charter-, or institutionally guaranteed do not. Most companies fall on the competitive side and don't recognize it because they conflate "we have a strong moat" with "our substrate is guaranteed." Moats are built; guarantees are decreed. The test is whether removing the company's strongest competitor would meaningfully change customer behavior. If yes, substrate is competitive. If not — if customers transact with the company because their default routing forces them to — substrate is closer to guaranteed.

The second is the survival role of services revenue. UnionPay's ~30% net margin on mandate-protected clearing means a services line is unnecessary, because there is no public multiple to defend. Most public companies do have to defend a multiple, and services revenue is the easiest way to defend it. Removing the services line in those cases would force a strategic crisis. Companies that could lose their entire services revenue without strategic consequence may be operating closer to the UnionPay shape than their framing suggests — and probably shouldn't continue to invest in productization at the same intensity.

The third is customer optionality. UnionPay's customer banks are also its shareholders and clear yuan card transactions through it because they were configured to. That structural configuration is rare. Most customer relationships are reversible — customers prefer the company, but the preference can be defected from. Reversible preference is precisely the condition under which productization is necessary, because services-as-glue raises the cost of defection.

The fourth is doctrine portability under structural change. If a regulator, charter, or institutional structure changed tomorrow, would the services strategy survive freestanding, or would it collapse? UnionPay's services investments — APOP, Nihao China, risk AI — would survive a regulatory shift. They are infrastructure, not franchise. Mastercard's federation playbook would also survive — it is a real services franchise with real external revenue. The companies most exposed are the ones whose services revenue is downstream of structural protection without their leadership recognizing it. Those companies are vulnerable in ways the framing usually hides.

The four conditions together are a frame for distinguishing companies whose productization investment is load-bearing from companies whose productization investment is decorative. UnionPay shows what the latter looks like at scale: real, well-built, technically credible — and optional only as long as the substrate guarantee holds.

References