Walmart

14

min read

Walmart Inc. reported $713.2B in revenue and $29.8B in operating income for fiscal 2026 (year ended Jan 31, 2026). On its face: a 4.7% top-line and a 1.6% operating-income story — a tired big-box operator. Underneath: four "alternative profit" lines that did not exist as material revenue six years ago, growing 20–50% per year, and reshaping the income statement.

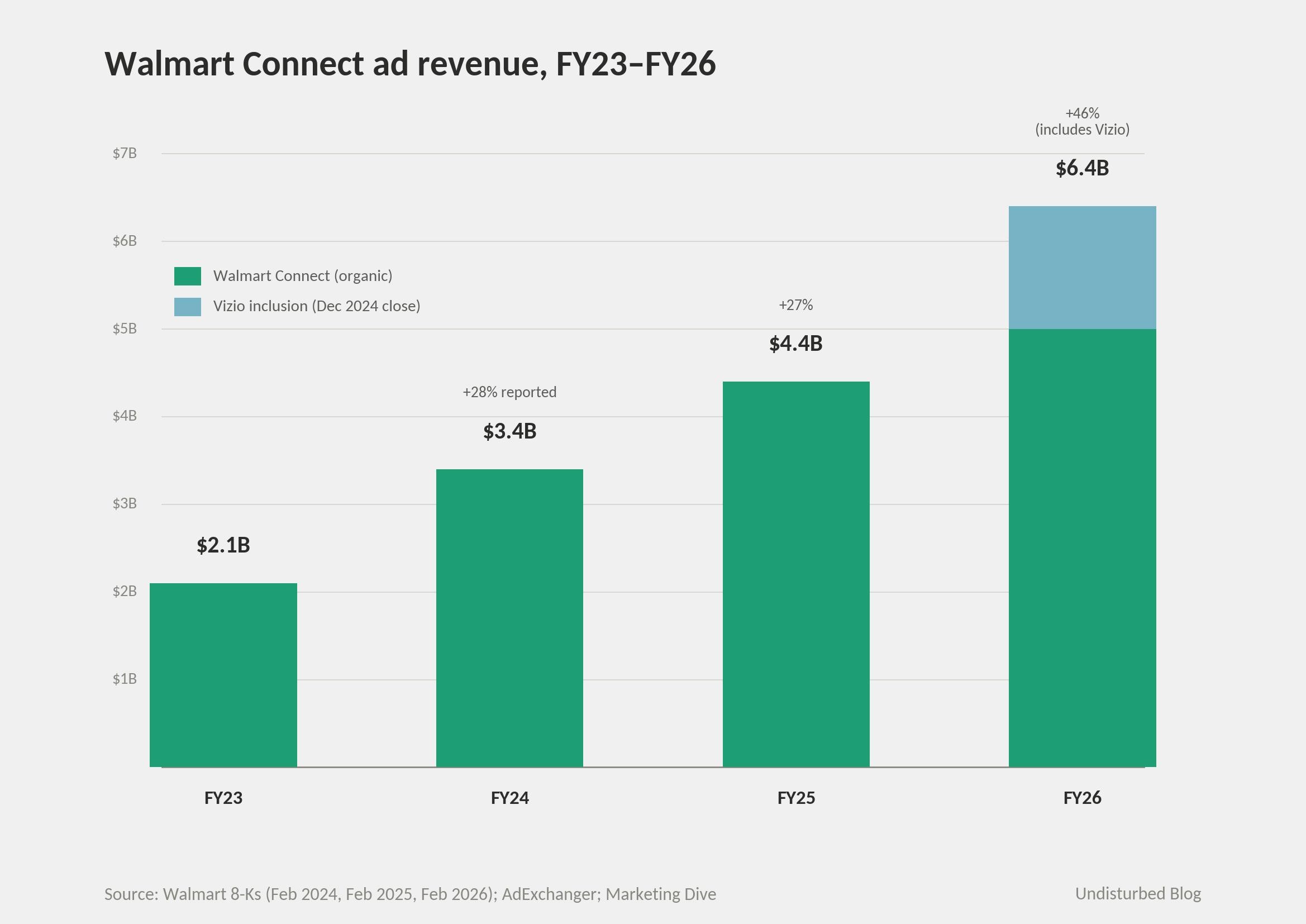

CFO John David Rainey told investors in February 2025 and again in February 2026 that advertising and membership combined "accounted for nearly one-third" of Q4 operating income. Global advertising revenue went from ~$2.1B (FY23) → $3.4B (FY24) → $4.4B (FY25) → ~$6.4B (FY26). The FY26 jump was inflated by Vizio's mid-year inclusion; the like-for-like Walmart Connect U.S. business still grew 41% in Q4 FY26 alone.

This is the structural shift. Walmart is not pivoting away from retail. It is monetizing the substrate retail produces — store traffic, payment data, supplier relationships, fulfillment infrastructure, and now connected-TV inventory — as a parallel high-margin layer. Amazon proved the same pattern in cloud (AWS, 2002–2006: an internal infrastructure layer turned outward). Walmart is the first retail-native re-instantiation. The frame Walmart itself uses is "Adaptive Retail" / "people-led, tech-powered." The financial behavior fits the AWS analogue almost exactly.

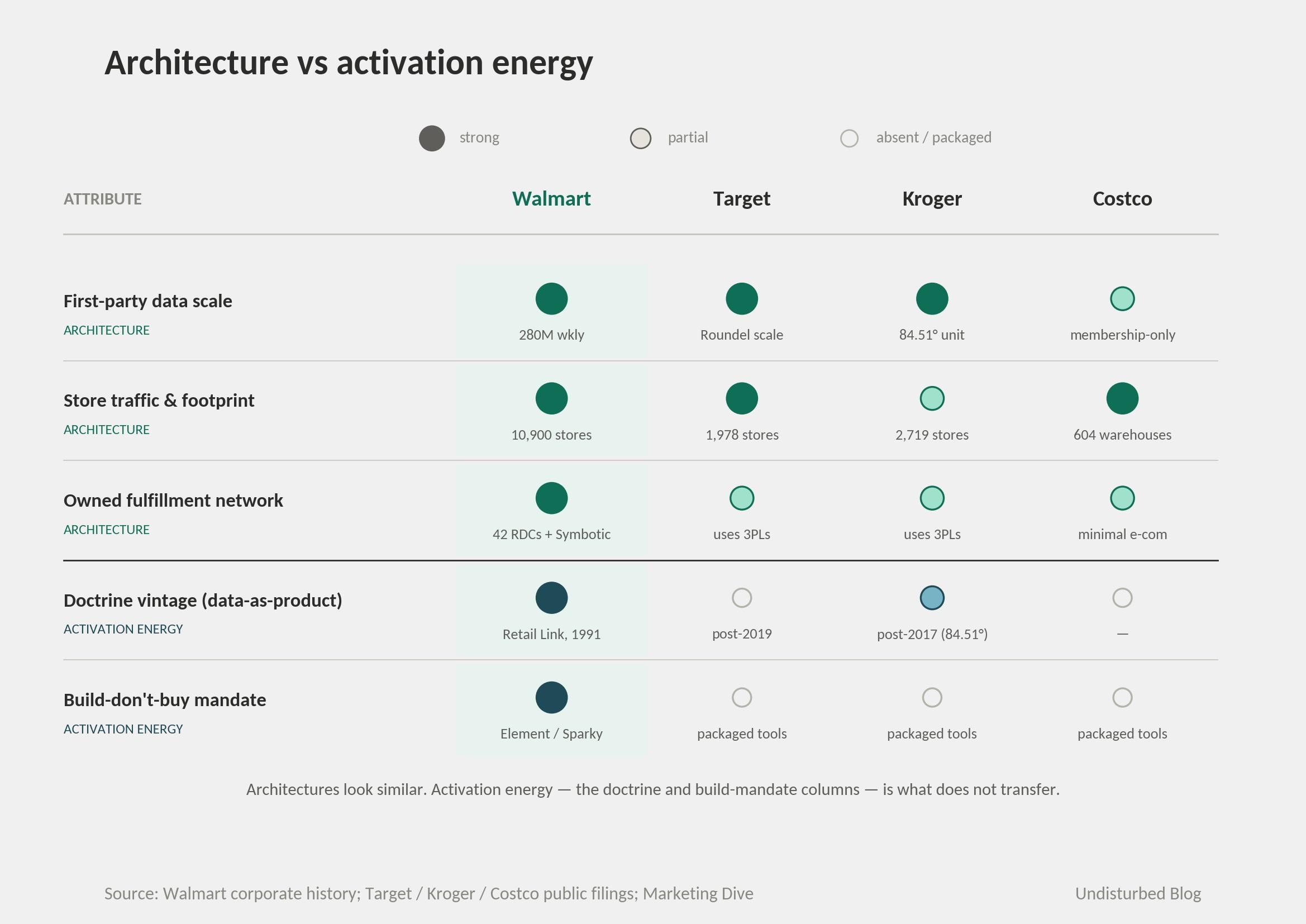

Most large retailers have customer data, store traffic and supplier relationships. Almost none have turned them into a meaningfully external revenue line. The reason is not capability — it is doctrine. Walmart is comfortable letting outside parties touch what most operators consider proprietary because it has been doing it since 1991, when Retail Link gave 20,000 suppliers extranet access to Walmart's own POS data. The doctrine pre-dated the platform. Without that history, the productized layer always loses to the "but this dilutes our edge" argument in the first cost-cutting cycle.

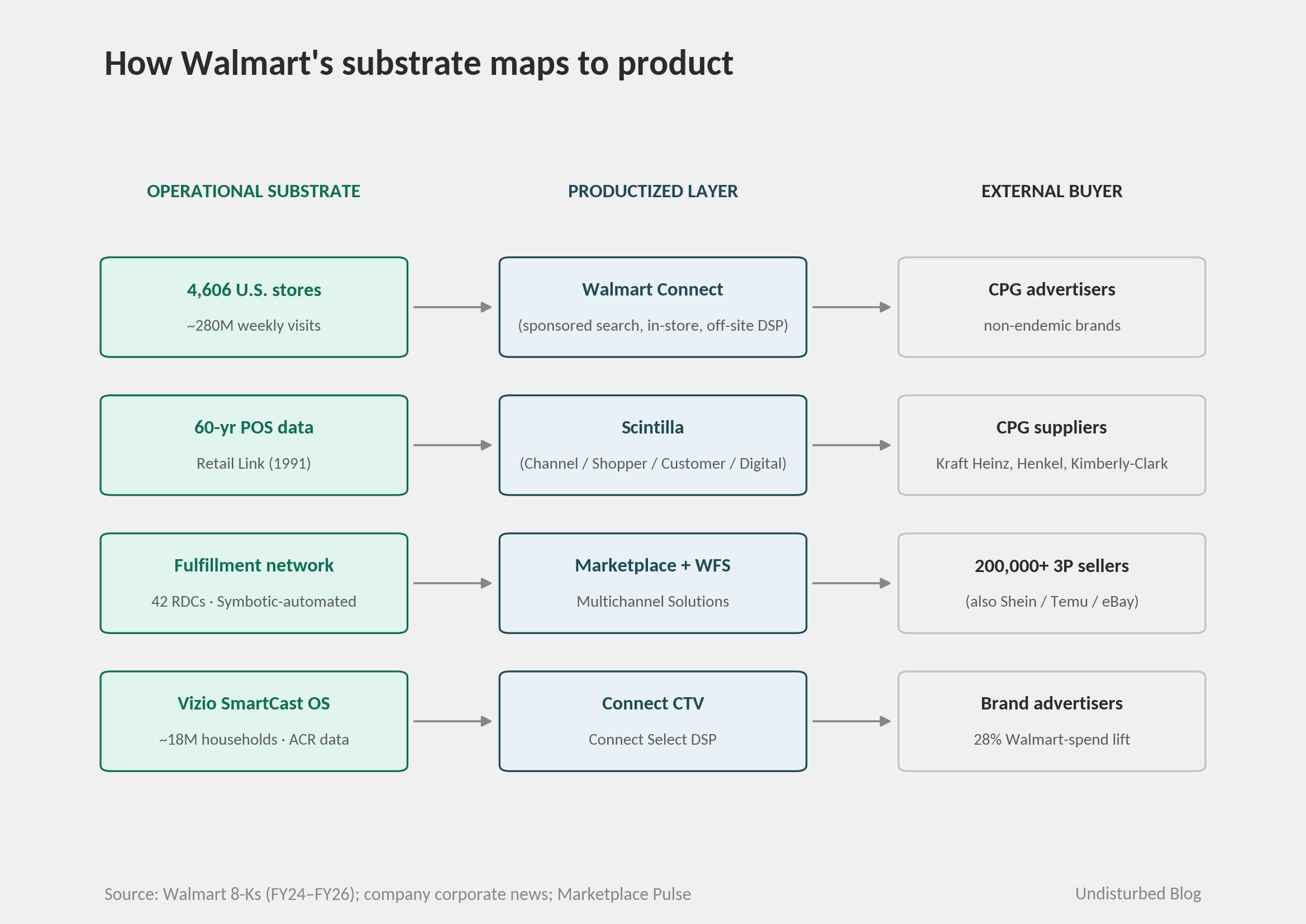

How the substrate maps to product

Two reads matter. First, every productized line rides on substrate the core retail business is already paying to operate. The marginal cost of an ad-impression on walmart.com or a WFS pick is near-zero relative to the revenue it generates. Second, the layers stack: a third-party seller on Marketplace becomes a buyer of WFS, then a buyer of Walmart Connect ads. One operational substrate. Three points of monetization. The revenue compounds before any new fixed cost is added.

How it actually works — three closed loops

Loop 1: Walmart Connect → closed-loop attribution → higher CPMs → more ad spend.

Walmart Connect was renamed from Walmart Media Group on January 28, 2021 with the explicit ambition of becoming a "top-10 U.S. ad business" within five years. The closed loop is the reason CPGs pay Walmart above standard CPC: a P&G shopper-marketing dollar spent on Sponsored Search is reconciled against actual Walmart card and store transactions, not panel data. That measurement loop is what advertisers are buying — proof of incremental sales lift, attached to the same SKU they advertised against. Vizio extends the loop to the living room: SmartCast viewing data ties to Walmart account purchases, and at IAB NewFronts in March 2026 the unified login showed a 28% lift in Walmart spend among CTV-exposed households. The loop closes; the spend rises; the next quarter's CPMs follow.

Loop 2: Marketplace seller → WFS → Walmart Connect → commission compounding.

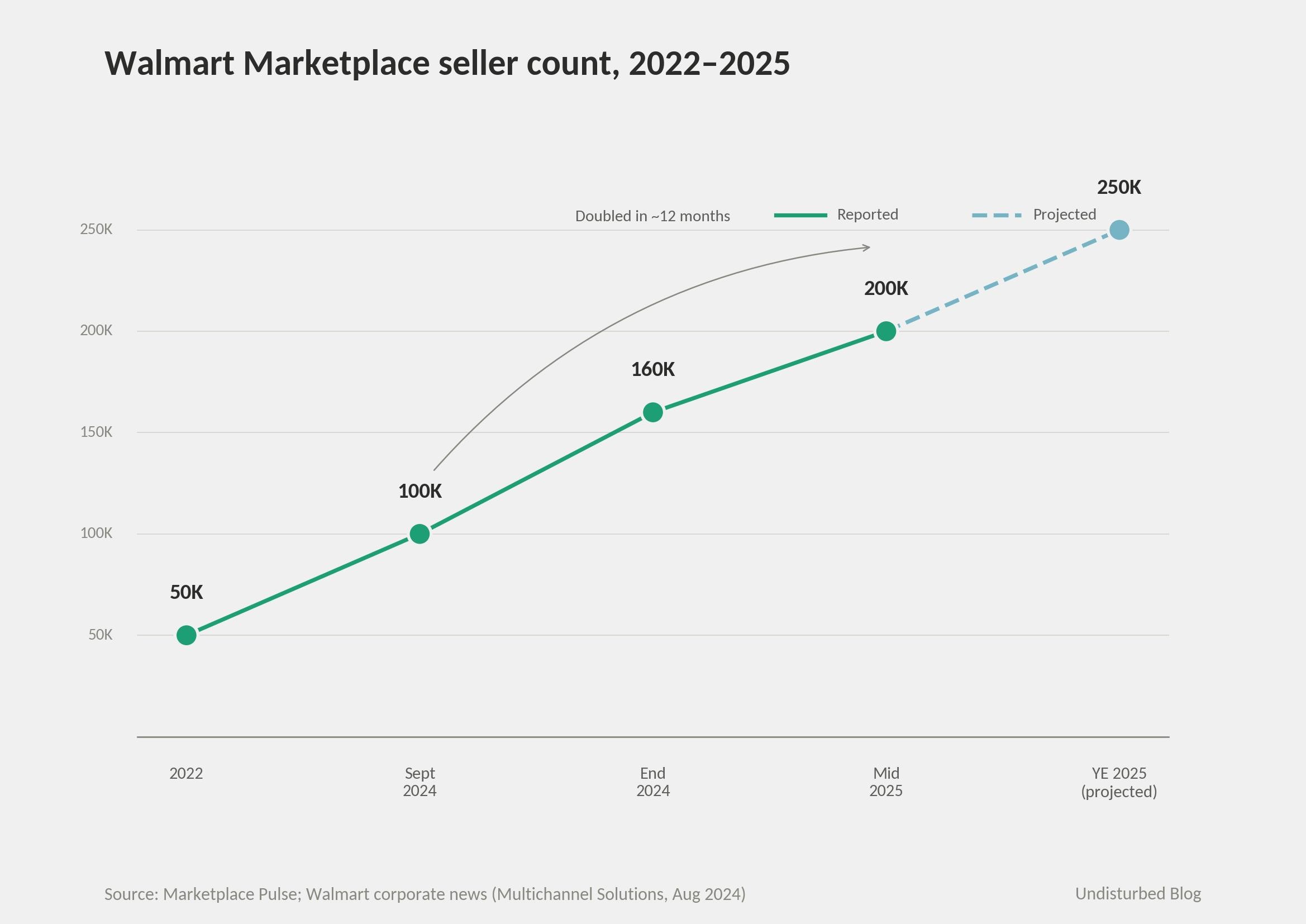

Marketplace launched in 2009 and accelerated under Marc Lore from 2016. WFS launched February 2020. Today: 200,000+ sellers (mid-2025, on pace for 250,000 by year-end), 420M+ SKUs, and 95% of items on walmart.com from marketplace sellers. The flywheel: a new 3P seller pays a commission on each sale → uses WFS to fulfill (52% WFS utilization in Q4 FY26, a record) → buys Walmart Connect ads to win search visibility → Walmart takes commission + WFS fees + ad fees on the same transaction. Multichannel Solutions (announced Aug 27, 2024) extended WFS to fulfill non-Walmart orders too — Shein, Temu, eBay, the seller's own site. The fulfillment network is no longer just Walmart's logistics cost. It is a product, sold by the pick.

Loop 3: Retail Link → Scintilla → Insights Activation → Walmart Connect.

Walmart Data Ventures was formed in 2021 under Mark Hardy (ex-CEO of InContext Solutions, P&G alum) "to unlock the full value of Walmart's first-party data." Walmart Luminate launched as paid SaaS in tiers, then was rebranded Scintilla at the Inspire 2024 conference (Oct 2, 2024) ahead of international expansion. Four modules: Channel Performance, Shopper Behavior, Customer Perception, Digital Landscapes. The insight is in the closing step — Insights Activation pipes the analytics directly into Walmart Connect campaigns as a one-click action. A CPG buys insight; the insight surfaces a campaign opportunity; the campaign runs on Walmart Connect; the campaign generates more first-party data; the data feeds the next insight. Reported 2024 metrics: client base +173% YoY, SMB representation +100%+, every renewal extended ≥3 years. Scintilla subscribers grew omni sales 15% YoY vs. peers (WDV, Oct 2025). Only Walmart and Kroger (84.51°) have a sales channel large enough to monetize this credibly — the loop requires both the data and the place to run the resulting campaign.

The pattern in all three loops is the same. Walmart paid to build infrastructure for itself. The infrastructure produces measurement. The measurement is what external buyers actually want. The product is the loop, not the capability.

The numbers

Walmart's fiscal year ends January 31. The transition from "retailer with an ad business" to "retail platform with a third of Q4 operating profit from services" happened in three reporting cycles.

FY | Total revenue | Operating income | Op. margin | eCommerce % of net sales |

|---|---|---|---|---|

FY24 (Jan 31 2024) | $648B | ~$27.0B | 4.2% | ~17% |

FY25 (Jan 31 2025) | $681.0B | $29.3B | 4.3% | ~18% |

FY26 (Jan 31 2026) | $713.2B | $29.8B | 4.2% | 23% (record) |

Walmart Connect / global advertising. FY24: $3.4B (+28%). FY25: $4.4B (+27%). FY26: ~$6.4B (+46%, includes Vizio). Q4 FY26 Walmart Connect U.S. alone +41% YoY, with Vizio contributing "triple-digit growth" off a small base. Walmart's ad-to-sales ratio sits at ~1% versus Amazon's ~8% — meaning the ad line could plausibly approach $20B without any retail-share gain. EMARKETER puts Walmart at 8.0% U.S. retail-media share for 2025 vs. Amazon Ads' 79.7%, with the duopoly capturing 89% of incremental 2026 retail-media spend.

That gap is more structural than the naïve read suggests. The naïve read is "Walmart has eight times the headroom." The structural read is harder: that gap measures the difference between a marketplace where 60% of GMV is third-party (Amazon) and one where third-party is still ramping (Walmart). Closing the gap depends on the marketplace seller count compounding — which is why the 100K → 200K seller curve over twelve months matters more than the ad number itself. The ad business is downstream of the seller flywheel. The forecast is an arithmetic identity, not a thesis.

Marketplace + WFS. 50,000 sellers (2022) → 100,000 (Sept 2024) → 160,000 (end 2024) → 200,000+ (mid-2025); 44,000 net adds in the first five months of 2025; ~60% of new sellers from China. WFS seller utilization reached a record 52% in Q4 FY26. Walmart U.S. Marketplace revenue +37% in FY25; +~20% in Q4 FY26.

Walmart+. Not officially disclosed. CIRP estimate: ~30M members in the Jan 2026 quarter, ~15% of Amazon Prime's ~201M U.S. base. Walmart+ members account for ~50% of U.S. .com/app spending and spend ~3× non-members. Total global membership income ~$4.3B FY26, growing double-digits each quarter.

Vizio. Announced Feb 20, 2024 at $11.50/share (~$2.3B equity value, all-cash). Closed Dec 3, 2024. ~18M SmartCast active accounts; >500 direct advertiser relationships at signing.

Capex. $13.1B (FY22) → $16.9B (FY23) → $20.6B (FY24) → $23.78B (FY25) → ~$25B (FY26, ~3.5% of net sales). 70%+ directed to technology and supply-chain automation.

The named program owners are what separates this from a slide deck. Mark Hardy runs Walmart Data Ventures. Seth Dallaire (EVP & CRO, Walmart U.S.) oversees Walmart Connect. Ryan Mayward (SVP retail media sales) handles ad sales. Sravana Karnati (EVP Global Technology Platforms) owns Element and Wibey. Suresh Kumar (EVP, Global CTO since July 2019, ex-Google/Microsoft/Amazon) owns the build doctrine across all of it. Daniel Danker — hired July 23, 2025 from Instacart as EVP, AI Acceleration, on a $44.1M FY26 comp package larger than McMillon's — closes the agentic-commerce gap. Each productized line has a single throat to choke.

The succession test

Does the strategy survive executive succession? Walmart will get an unusually clean answer in February 2026, when Doug McMillon retires and John Furner takes over.

The substrate test: Element, Walmart's proprietary multi-cloud ML platform (Kubernetes + MLOps, organized around what Walmart calls a "triplet model" of public + private + edge). It powers virtually every customer- and associate-facing AI tool in the company. Sravana Karnati announced Element's "agentic upgrade" plus the Wibey developer super-agent at Converge 2025 (August 2025). VentureBeat reports 1.5M associates use Element-built tools.

The product test: four "super agents" in production or rollout. Sparky (customer agent, GA June 6, 2025) — multi-modal, drove ~35% higher basket sizes per Jefferies analyst note (Apr 2026), with ad placements being tested inside it from late 2025. Marty (seller/advertiser agent, rolling out 2025–2026) — the Walmart Connect advertising assistant inside Marty handles 97% unique queries. My Assistant (corporate associate tool, expanded June 2025 to >900,000 weekly users and 3M queries/day, with real-time translation across 44 languages cutting shift planning from 90 to 30 minutes). Wibey (developer super-agent, August 2025).

The doctrine test: "Adaptive Retail" was coined by Suresh Kumar at CES 2024 (January 9, 2024). McMillon's "people-led, tech-powered" framing was repeated verbatim at every major investor event through FY26. Walmart partnered with OpenAI in October 2025 to certify 10M Americans by 2030, channeled through Walmart Academy. McMillon told the WSJ in September 2025 that headcount would remain roughly flat at ~2M for three years, and reiterated at HBR in November 2025: "every job we've got is going to change in some way." Total headcount is being held flat — not reduced — and productivity gain is the explicit thesis.

Two caveats matter. May 2025: 1,500 layoffs in U.S. retail and global tech teams "to remove layers and complexity." March 2026: Walmart effectively pulled the OpenAI Instant Checkout experiment after accuracy issues, pivoting to embed Sparky inside ChatGPT and Gemini rather than rent OpenAI's surface. The second of these is the more interesting tell. Walmart did not just abandon the partnership; it inverted it. It would rather control the agentic surface than pay for distribution. That is the same doctrine that runs Element instead of buying SageMaker, that bought Vizio instead of partnering with Roku.

The succession test is not whether AI continues — every retailer has that. It is whether the build-doctrine holds. McMillon's signature was not AI investment. His signature was the 2020–2021 unwinding of Marc Lore's $3.3B Jet.com era and the 2019 hire of Suresh Kumar to run "build, don't buy." Vizio is the calibrated exception that proves the rule — bought because 18M households of ACR data is the bottleneck the productized layer needs and cannot be built organically. Furner's first 18 months will reveal whether the doctrine is portable. If a major 2026 acquisition fits the Vizio template (substrate gap, controlled exception), the platform survives. If it looks like Lore-era growth-by-acquisition, the platform compresses.

Why this answer fits Walmart specifically

Sam Walton founded the company in 1962 in Rogers, Arkansas. He attended an IBM computer-training course in 1968 and adopted Walmart's first company-wide computer system in 1969 — earlier than nearly any U.S. retailer. The Retail Link system, conceived by Walton and David Glass beginning in 1985 and operational by 1991, cost ~$4B over time and gave 20,000+ suppliers direct extranet access to 100 weeks of POS data. Walmart's own buyers objected at the time, because they thought sharing data with suppliers would cost them negotiating leverage. Walton's response, per Frontline's Sam Hornblower: "suppliers and buyers were really all on the same side."

That is the primal doctrine. Operational data is more valuable shared/sold than hoarded. Scintilla in 2024 is the SaaS-era expression of the same thesis. Walmart Connect is the same thesis applied to advertising attribution. WFS is the same thesis applied to fulfillment capacity. The doctrine has been compounding for forty years before AI made the productization tractable.

Doctrinal continuity matters. McMillon (CEO since February 2014) inherited Lore's hybrid strategy of buying e-commerce capability — Jet.com $3.3B (2016), Bonobos, ModCloth, Jetblack. He unwound it in 2020–2021 (Jet.com shut May 2020; Lore retired Jan 31, 2021) and replaced it with build-don't-buy under Suresh Kumar (recruited from Google in July 2019 after stints at Microsoft Cloud and 15 years at Amazon). Vizio in 2024 is the controlled exception — bought specifically because Walmart could not build a TV-OS with 18M household reach organically.

The "why now" is five forces converging in 2024–2026: the post-cookie advertising world made first-party data disproportionately valuable; Amazon Prime Video's ad-default switch (January 2024) signaled CTV would become the next retail-media battleground; generative AI made internal tooling economically buildable for a non-tech company; Walmart U.S. e-commerce hit eight consecutive quarters >20% growth and reached 23% of net sales by Q4 FY26 (the first profitable digital quarters in U.S. and Mexico); and the substrate scale (10,900 stores, ~280M weekly visitors) finally made ad CPMs and seller commissions worth the build investment.

Architecture transfers. Activation energy does not. This is the distinction that separates what travels from what does not. The architecture — first-party data, store traffic, fulfillment network, supplier relationships — is reproducible at smaller scale. Target Roundel hit ~$1.76B in FY24, material but a fraction of Walmart Connect. Kroger has 84.51° and Kroger Precision Marketing. Costco has membership data. The architectures exist. What does not transfer is the activation energy — forty years of Retail Link doctrine, six years of Suresh Kumar's build-mandate, the willingness to spend $2.3B on a TV company most boards would have called a distraction, and the post-2019 internal capability to ship Element/Sparky/Marty/Wibey on a multi-cloud ML stack rather than buying packaged tools. Activation energy is not a slide; it accumulates in decades, not quarters. Other retailers can copy the architecture. They cannot catch up to forty years of compounded doctrine inside two budget cycles. A retailer announcing a "retail media network" in 2026 is not building Walmart Connect — it is building the announcement.

What to track next

The CTV ramp. Vizio + Onn TVs + a unified Walmart account login (announced March 23, 2026 at IAB NewFronts) targets ~25–30% U.S. household penetration. Connect Select (March 2026) gives mid-market advertisers programmatic CTV access alongside Paramount, Warner Bros. Discovery and the major SSPs. The marker to watch: whether Walmart Connect's ad-to-sales ratio drifts from ~1% toward Amazon's ~8%.

Scintilla's international expansion. Mexico and Canada launched in 2024–2025; the rebrand removed "Walmart" from the name precisely to enable Walmex/Asda-style banner extensions. The seller-side equivalent — Marketplace seller count on pace for 250,000+ by year-end 2025 — keeps compounding.

Sparky's monetization. Walmart began testing ads inside Sparky in fall 2025. If basket-lift consistency holds at 35% and sponsored prompts scale, Sparky becomes the next high-margin ad surface — and the first one Walmart owns at the agent layer rather than the search-results layer.

Element / WCNP as the next productized candidate. McMillon's HBR comment in November 2025 — that automation training "could one day grow into a profit center" — is the most pointed hint yet that Walmart's internal AI and automation tooling is being prepared for external offer. This would be the most direct AWS analogue Walmart has produced. It is the move worth tracking 2026–2028, because the AWS test is exactly this: an internal team starts getting unsolicited inbound from external companies asking to buy what was built internally.

Furner-era doctrine. The leadership shake-up announced January 16, 2026 — Guggina to Walmart U.S., McLay exiting International — signals tighter integration of e-commerce and retail. The OpenAI partnership reversal (March 2026) is a leading indicator: Walmart prefers to embed Sparky inside third-party agentic surfaces rather than license its checkout to them. The doctrine again. Keep the productized layer Walmart-owned.

The risk to track is concentration. EMARKETER projects Walmart and Amazon will capture 89% of incremental U.S. retail-media spend in 2026. That is a duopoly moat for now. If TikTok Shop, Instacart or DoorDash materially scales a closed-loop offering, Walmart's Connect pricing could compress before the ad-to-sales ratio gets close to Amazon's 8%. The platform's growth depends on retail-media spend continuing to consolidate, not fragment.

The diagnostic — four conditions for re-productization

Companies that turn operational substrate into external products tend to clear four conditions. Walmart clears all four. Most candidates clear at most two.

Substrate. The first condition is whether internal tools or datasets the company is already paying to build, run and refresh have, with modest packaging, an external buyer. Walmart's substrate map is explicit: Retail Link → Scintilla; ML platform → Element; fulfillment → WFS; store traffic → Walmart Connect. Companies whose candidate list comes up empty do not have a re-productization opportunity — they have an operating-leverage problem.

Margin. The second condition is whether gross margins on the productized version are materially higher than the core business. Walmart Connect take rates and Walmart+ membership margins sit dramatically above the 4.3% retail operating margin, which is why these lines now contribute a third of operating income on a small fraction of revenue. When the productized line cannibalizes core economics rather than supplementing them, the math fails.

Doctrine. The third condition is whether "data and operations as products to share or sell" is something the founders embedded — or a slogan a consultant wrote on the whiteboard. Walmart's Retail Link, 1985–1991, embedded the doctrine for forty-plus years before Scintilla packaged it as SaaS. Without doctrine, the productized line gets killed in the first downturn because someone reasonable will argue it dilutes focus.

Inflection. The fourth condition is whether the AWS moment is actually here. Walmart's was 2021–2024 — when first-party data became regulatorily scarce, when AI infra costs collapsed enough to build internal tools cheaply, and when the e-commerce flywheel finally hit positive operating leverage. AWS moments are rare and recognizable in hindsight. The leading indicator: an internal team starts getting unsolicited inbound from external companies asking to buy what was built internally.

When three of the four conditions fail, the frame is wrong for the company. When three hold and one is borderline, the borderline one is where the next two years of work belongs.

References