Allianz

15

min read

Allianz operates roughly 70 separately regulated insurance entities across some 70 countries, serving 128 million customers with 156,000 employees. The 2025 financial year closed with operating profit at €17.4 billion, a new record, and core return on equity at 18.1%. By early 2025, more than 60,000 of those employees were already using AllianzGPT — the internal LLM platform launched in September 2023, less than a year after ChatGPT's public release — and the company has committed to rolling AllianzGPT 2.0 to all 156,000 employees in 2026.

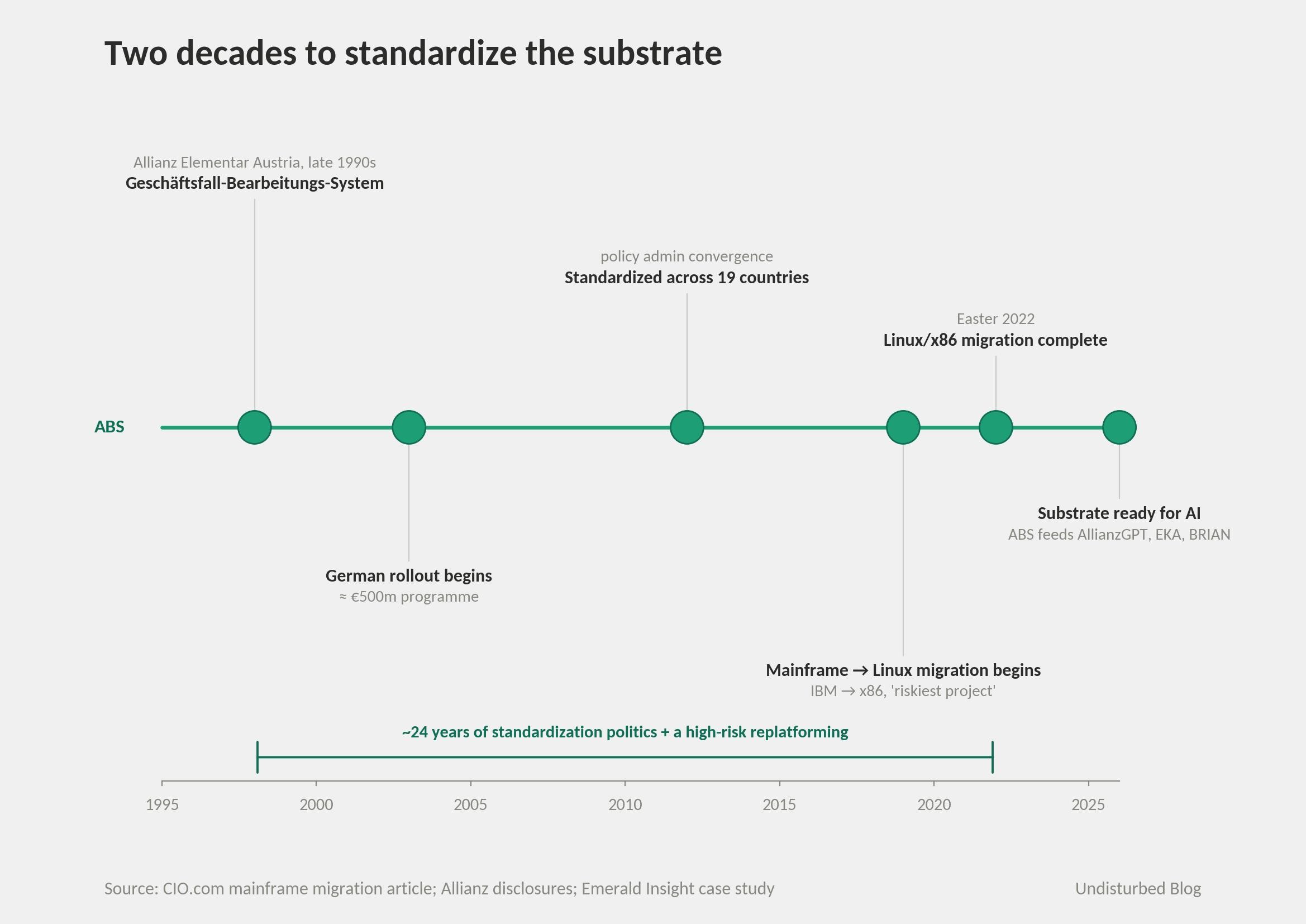

Underneath the visible AI activity sits a substrate that took two decades to build: the Allianz Business System, now handling roughly 60 million policies across 19 countries and migrated off the IBM mainframe to Linux/x86 by Easter 2022; and the Allianz Data Platform, which feeds more than 900 registered AI use cases. The model layer above it changes vendors fluidly — OpenAI in 2023, DeepSeek added in two weeks in early 2025, Anthropic's Claude promoted to a "core component" of the internal platform in January 2026. When a multinational federation of regulated entities decides to take AI seriously, the strategic move is to fuse the substrate and rent the intelligence. The slow layer is defined by jurisdiction. The fast layer is defined by whoever shipped the best model this quarter.

The Federation Layer Changes the Pattern

The architecture of a regulated multinational running AI on shared infrastructure is not a new shape. Earlier pieces in this series have walked through it inside FedEx, where physical assets and the data they generate move on annual cadence, locked to capex cycles, while intelligence and interface layers swap models and surfaces quarterly. The same four-layer geometry holds inside JPMorgan, with a balance sheet swapped for trucks. Allianz fits the same geometry, but with one feature neither earlier case carries.

FedEx is a single operating company. JPMorgan is a single regulated bank holding. Allianz is a federation: about 70 separately regulated insurance operating entities, each with its own balance sheet, its own Solvency II capital requirement, its own local regulator, its own Chief Data Officer. The pace layering happens inside that federation rather than inside a single legal entity.

That single difference changes how the substrate has to be designed, how AI ownership is structured, and how the strategy survives executive succession. A simple test makes it concrete. In a single-entity case, when the CEO replaces the head of one division, AI strategy survives because the substrate is shared inside one company. In Allianz's case, the substrate has to survive a regulator in any of roughly 70 jurisdictions deciding it doesn't like something. The Singapore government blocked Allianz's S$2.2 billion Income Insurance acquisition in October 2024, and Allianz withdrew within two months. That isn't a setback. It's the operating condition of the federation pattern.

The federation also rules out two adjacent answers that have been documented elsewhere. The one-substrate-fits-all model that DHL built around a unified data layer is not on the table here — Allianz built two substrates and runs them at deliberately different speeds, with the Allianz Business System and the Allianz Data Platform on annual cadence and AllianzGPT swapping foundation models in weeks. The substrate-as-product model — building internal infrastructure and turning it into a sovereign offering, as Schwarz Gruppe has done with STACKIT — has also been declined. Allianz consumes Azure, AWS, and Anthropic; it does not sell its substrate to anyone. The 2019 Syncier attempt to commercialize "ABS Enterprise Edition on Azure" has gone quiet. The dog didn't bark.

Most pattern analyses treat regulated industries as one bucket. They aren't. A single-jurisdiction bank can ship a chatbot to 100% of its customers on the same day. An insurer with operating entities in Germany, India, Australia, Singapore, the US, and Brazil cannot. Every model deployed touches six insurance regulators, six privacy regimes, six labor councils, and six product approval cycles, running on six different clocks. The pace layering isn't a design choice in that environment; it's the regulatory geography forcing itself into the architecture. The strategic move is to treat that constraint as the moat, not as the cost.

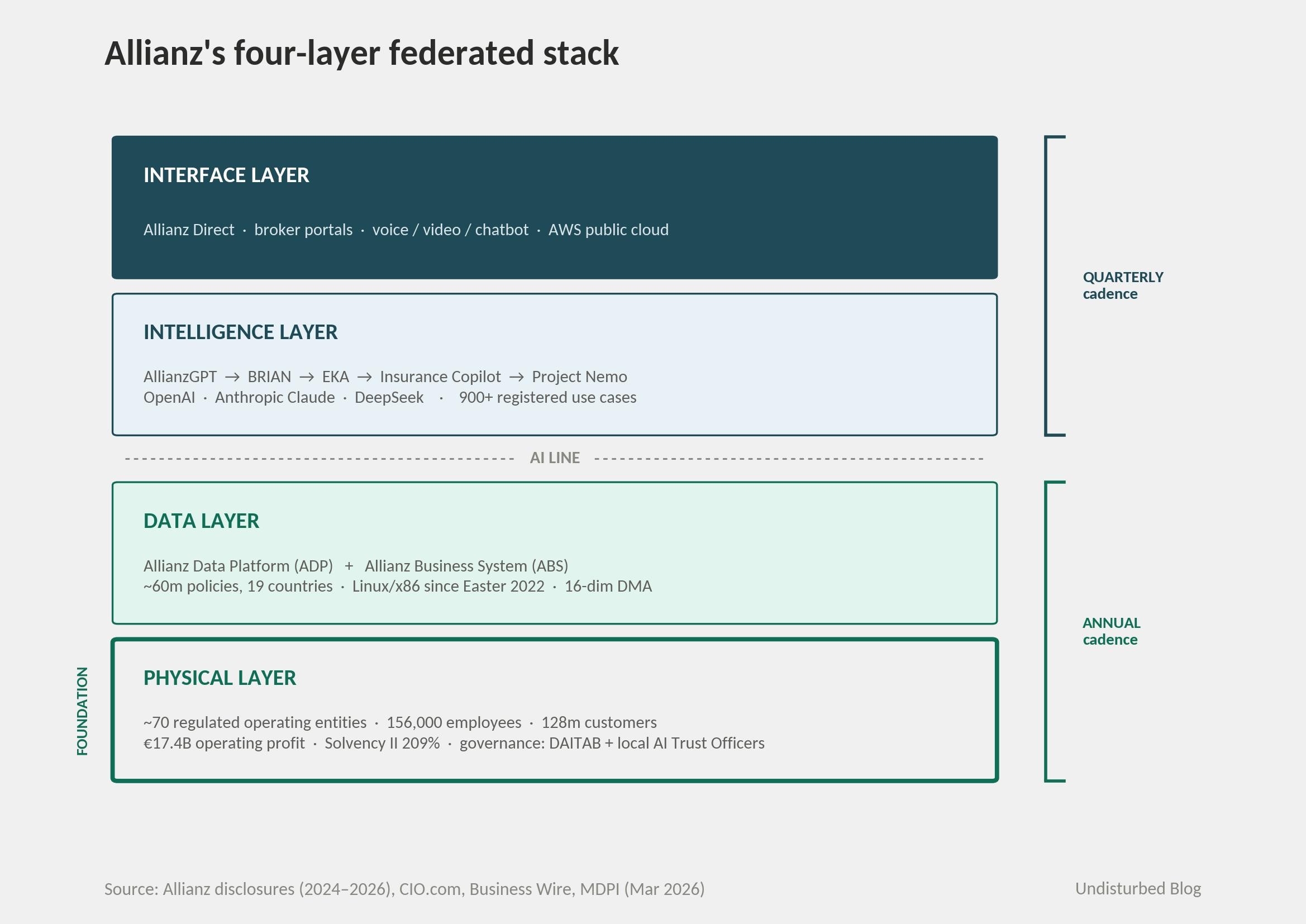

The Strategy in One Picture

Two things are different from the FedEx and JPMorgan diagrams.

The first is at the bottom. In the single-entity case, the physical layer is "trucks" or "branches" — one asset class, one accounting treatment. Here it is a federation of regulated entities, each with its own balance sheet and its own regulator. The decades-cadence layer isn't one slow thing. It's seventy slow things, held together by shared governance.

The second is at the top of the data layer. The Allianz Business System is a policy administration platform that took roughly twenty years to standardize across nineteen countries — and Allianz's CTO has said publicly that the 2019–2022 mainframe-to-Linux migration was "one of the riskiest and most difficult projects of my career." That isn't an AI project. It's the precondition for AI to be possible at all.

Allianz itself does not draw the diagram this way. The strategy decks present three pillars — smart growth, productivity, resilience — and put AI under productivity. The four-layer view is an analytical frame imposed from outside. But the slot-by-slot evidence supports it: the Business System moves on a decade clock, AllianzGPT swaps models on a weeks clock, and the COO who owns both is one person.

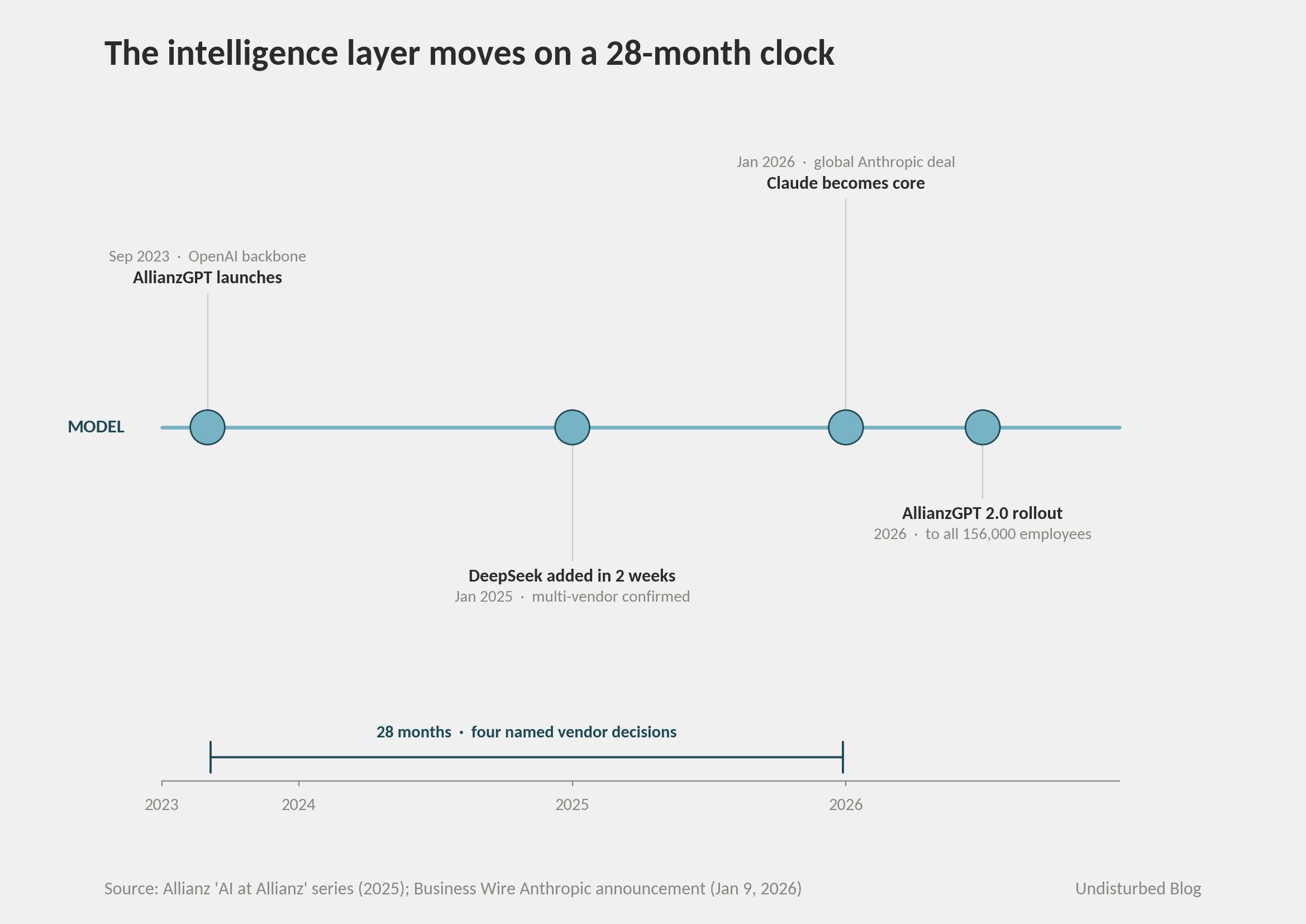

The vendor cadence makes the speed gap visible. The Business System took twenty years to stabilize. Above it, the intelligence layer cycled through four named decisions in the 28 months between AllianzGPT's launch and the Anthropic partnership — OpenAI as the initial backbone, DeepSeek slotted in within two weeks of its release, Claude promoted to "core component" status, and AllianzGPT 2.0 staged for the full 156,000-employee rollout in 2026. The slow layer is twenty years. The fast layer is twenty months. The architectural job is to make sure neither one is forced to move at the other's clock.

How It Actually Works — Three Closed Loops

Three loops show where AI actually runs at Allianz, and where the federation reshapes the standard four-layer mechanics.

Loop one: BRIAN and the underwriting question stream.

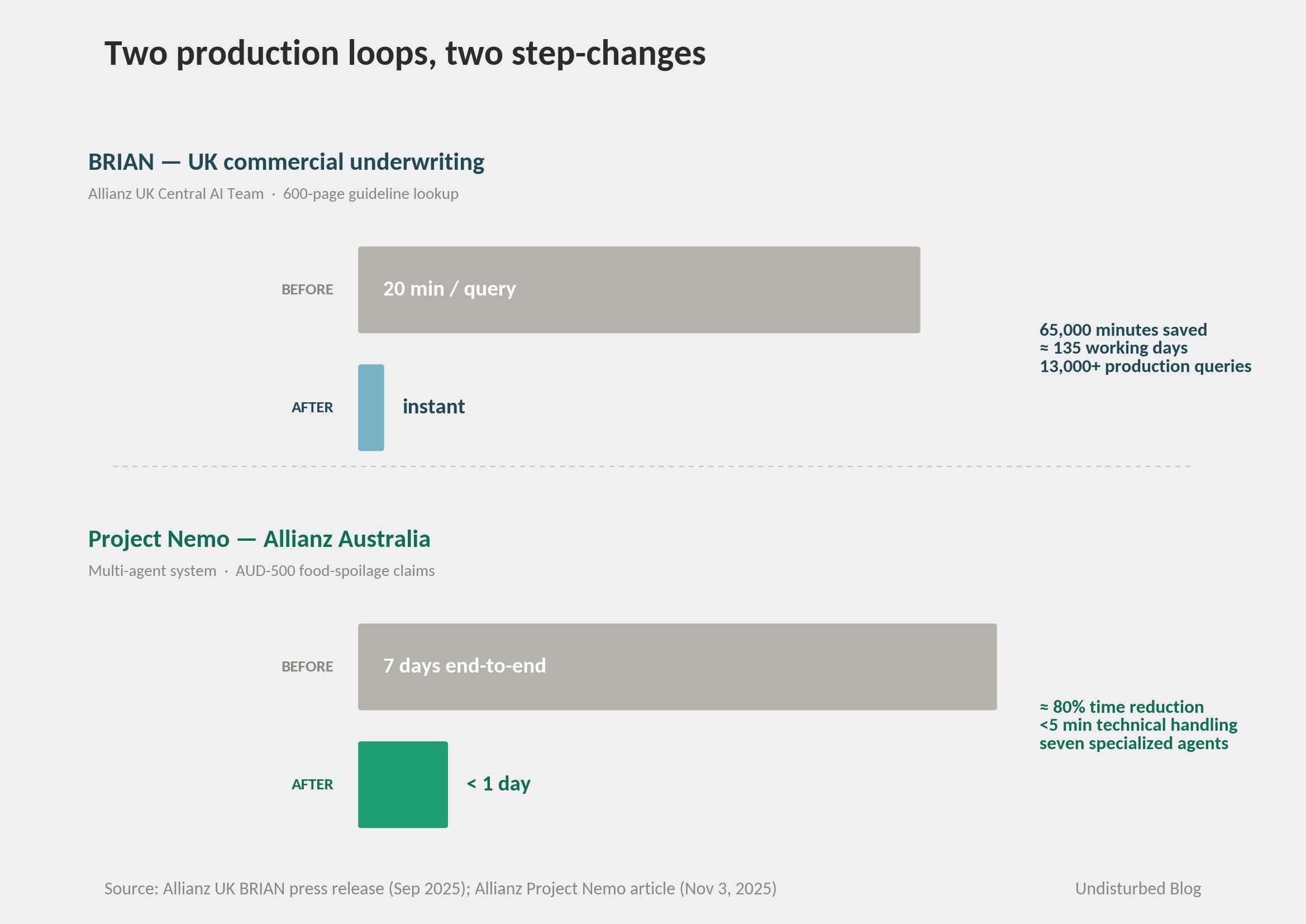

Allianz UK's commercial underwriting team had a 600-page guideline document. Reading it to answer one question took twenty minutes. The Central AI Team built BRIAN — an internal generative-AI assistant indexed against that document. In the pilot, 190 underwriters asked 3,000 questions. The system went into production in January 2025 across 260 users, scaling to all 600-plus UK commercial underwriters. By September 2025, BRIAN had handled more than 13,000 queries and saved roughly 65,000 minutes — about 135 working days. The closed loop isn't the obvious one (questions in, answers out). It's that every query, citation, and edge case where BRIAN gets it wrong becomes training material for the next version of the underwriting guideline itself. The intelligence layer is writing back to the data layer.

Loop two: Project Nemo and a multi-agent system per claim.

In July 2025, Allianz Australia put a multi-agent system into production for food-spoilage claims under AUD 500. Seven specialized AI agents — covering planning, fraud detection, coverage assessment, payout, audit, and adjacent tasks — handle each claim end-to-end. A human claims professional retains final authorization, and payouts are never fully automated. Processing time dropped from about seven days to under one day. The technical handling alone runs in under five minutes. The closed loop here is at the interface level: every claim the system processes generates a decision log that retrains the agents on the next batch. This is the first production agentic system Allianz has disclosed, and the design choice worth noting is that the orchestration sits at the operating-entity level, not the Group level. Australia ships first. Other entities graft onto the pattern when their regulators and labor councils sign off.

Loop three: Claude inside the substrate.

The January 2026 Anthropic partnership is the cleanest statement Allianz has made about the architecture. Three workstreams: workforce empowerment (Claude in AllianzGPT for all employees), agentic AI for motor and health claims (Project Nemo at scale), and compliance logging. The detail that matters: Claude Code is going to thousands of Allianz developers — the engineers who build and maintain the Business System and the Data Platform themselves. The intelligence layer is starting to write the data layer it sits on. If that recursion holds, the cadence of the slow layer could itself accelerate, because the people building it would be using the fast layer to do it. It is too early to claim that has happened. As of mid-2026, the partnership is five months old.

Across all three loops, the federation shows up in the same way: the loop is designed once at Group level — the platform, the governance, the model selection — then grafted onto each operating entity on a timeline its regulator allows. Australia first for Nemo. UK first for BRIAN. Germany and India first for EKA. The grafting is the operating model.

The Numbers

Numbers establish that this isn't a slogan.

Financial baseline. Total business volume of €179.8 billion in 2024 and €186.9 billion in 2025 (+8.1%). Operating profit of €16.0 billion in 2024 — the record at the time — followed by €17.4 billion in 2025 (+8.4%, new record). Core EPS of €25 in 2024 rising to €28.61 in 2025. Core return on equity of 16.5% and 18.1%. P/C combined ratio of 93.4% at YE 2024 and a Solvency II ratio of 209% at the same date. Capital Markets Day 2024 targets, running to 2027: EPS CAGR 7–9%, return on equity ≥17%, P/C combined ratio 92–93%, and more than €27 billion in cumulative net cash remittance 2025–27. Berenberg analysts estimate that AI and digital have already trimmed roughly 60 basis points per year off the P/C expense ratio — which is the line where AI inside an insurer is supposed to show up if it is doing real work.

AI program metrics. AllianzGPT launched in September 2023; by early 2025 it had more than 60,000 active users, a 95% weekly engagement rate among those users, 10 million-plus messages generated, and 60 domain-tuned instances in operation. AllianzGPT 2.0 is slated for 2026 rollout across all 156,000 employees. Owner: Manuela Diviach, Head of Group Operations, Organization, Data & AI. BRIAN passed 13,000 production queries by September 2025 and roughly 65,000 minutes (135 working days) saved against the legacy workflow, scaling to 600-plus underwriters; owner Benjamin Blackie, Allianz UK Central AI Team. EKA — the Enterprise Knowledge Assistant — runs above 90% accuracy, deployed across 10-plus operating entities (Italy, Mexico, Portugal, Benelux, UK, US Life, Germany, India), trained on corpora of more than 90,000 paragraphs and now running in production across more than 5,000 historical large claims documented in the MDPI paper (March 2026); technical owner Dong Chen, Head of Advanced Methods, Group Data & AI. Project Nemo: seven specialized agents, under 5 minutes technical processing, roughly 80% reduction in claim time (about 7 days to under 1 day) for AUD-500 food-spoilage claims; owner Maria Janssen, Chief Transformation Officer at Allianz Services, with Thomas Baach, MD Core Insurance Platforms, Allianz Technology.

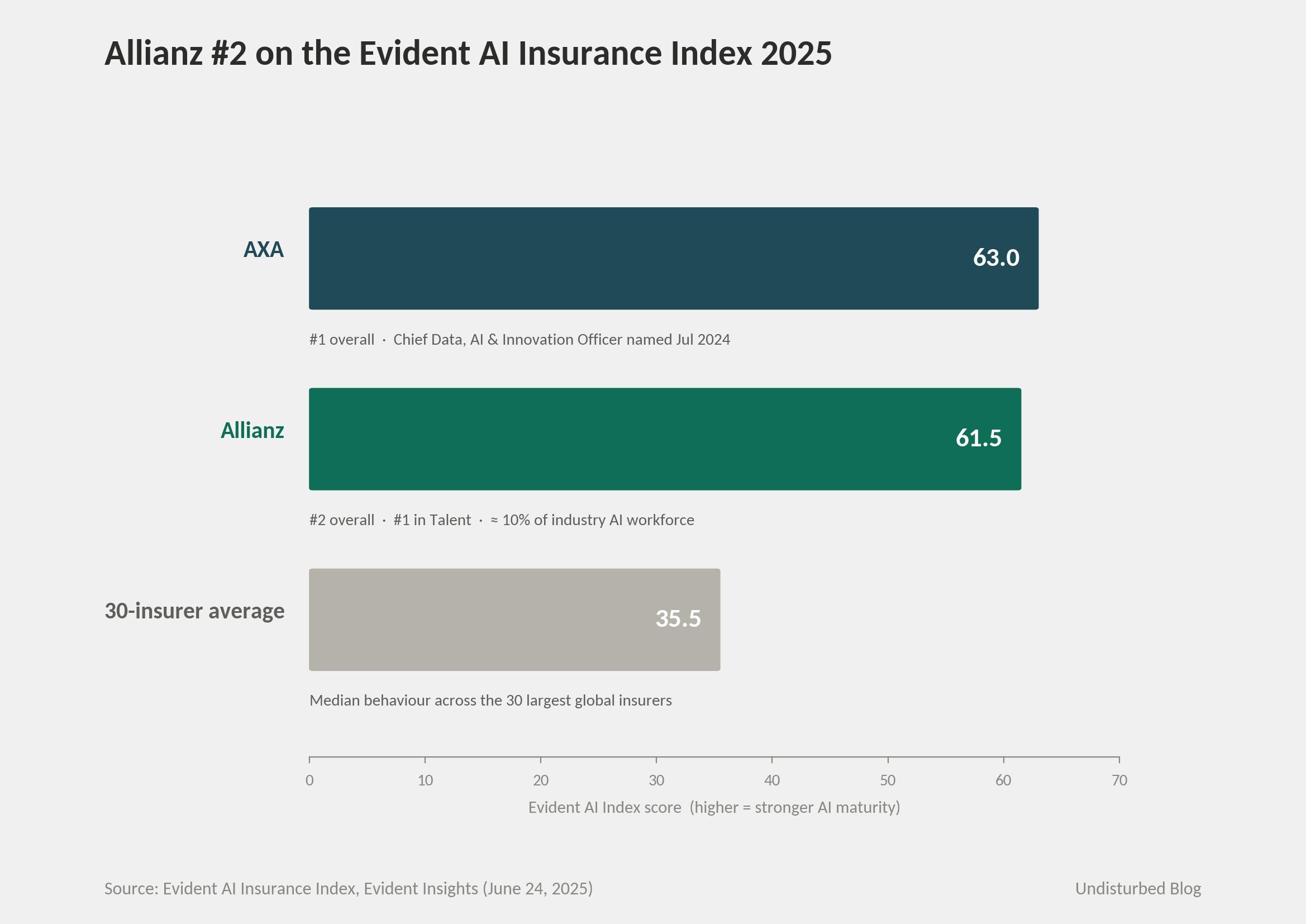

Industry context. The Evident AI Insurance Index, published June 2025, ranks Allianz #2 at 61.5 points behind AXA at 63, against a 30-insurer average of 35.5. Allianz holds the #1 position in the Talent pillar and employs roughly 10% of the AI workforce across the 30 largest insurers — about 2,300 of an industry total around 23,000.

A named program owner appears in every AI line above. That isn't decorative. It is the test of whether AI inside an insurer has actually escaped the R&D function or is still being narrated by one.

Vendor-led AI announcements lean hard on user counts: "60,000 employees using AllianzGPT." The number is real, but it isn't the proof. The proof is the 95% weekly engagement rate among that 60,000 — the share of users who came back without anyone asking them to. AI tools that don't get used twice are everywhere in insurance. The metric that tells you a tool has crossed from proof-of-concept to norm is repeat use, not registered users. Allianz publishes both, which is itself the signal.

Is AI a Norm Inside Allianz?

The question that separates an AI strategy from an AI program is whether AI use is a norm or an isolated experiment. Three pieces of evidence say it's a norm at Allianz, and one piece pushes against it.

First, ownership is structural. AI sits inside Operations, not inside a separate AI office. The accountable executive is Dr. Barbara Karuth-Zelle, COO and Member of the Board of Management, with a mandate extended through 2028. Below her, Manuela Diviach runs Group Operations, Organization, Data & AI; Dr. Philipp Raether is Group Chief Privacy & AI Trust Officer; Agostino Ferrara is CEO of Allianz Technology SE, with more than 11,000 employees in 20-plus countries. The absence of a "Chief AI Officer" title is itself the doctrine. AI is a process technology, not a product line. AXA created the explicit role (Andreas Schertzinger as Chief Data, AI & Innovation Officer in July 2024); Allianz did not. Both readings are defensible. Allianz's reading puts AI inside the function that already owns standardization across the federation.

Second, governance is Board-level. The Group Data and AI Trust Advisory Board — evolved from the 2021 Group Data Advisory Board — advises the SE Board. Eight Responsible AI principles, codified in the "Practical Guidance for AI," are checked at every lifecycle stage. Allianz signed the EU AI Pact in November 2024. Local AI Trust Officers operate in each operating entity. This is what shared doctrine looks like when it has been written down for years.

Third, the texture of use is daily. The 95% weekly engagement number among AllianzGPT users says the tool is now part of how work gets done, not an opt-in experiment. EKA is live across 10-plus operating entities. BRIAN is moving from pilot to default in UK underwriting. The Allianz Trade workforce has been running "Gen AI Ready" workshops to lift the entire credit-analyst function — about 550 analysts and 430 underwriters — into competence with generative tools.

The piece that pushes against the norm reading is that the disclosed deployments are still skewed to specific use cases at specific entities. Project Nemo is one product line in one country. BRIAN is one underwriting team. EKA is ten entities out of seventy. Allianz has shown it can graft AI loops onto entities, but the graft isn't finished. AllianzGPT 2.0 in 2026 is the next test of whether scale becomes uniform.

A strategy is a norm only if it survives the CEO who launched it. Oliver Bäte has been CEO since 2015 and runs the 2024–2027 "Lifting Ambitions" plan to the 2028 AGM. The interesting question isn't whether AI deepens during the remainder of his tenure — it will. The question is whether the federated stack survives the next CEO, who will face pressure to either re-centralize (and kill the operating-entity autonomy that makes the federation work) or re-decentralize (and let each entity pick its own AI platform). The architectural answer that protects the strategy is Karuth-Zelle's domain. Operations is where standardization decisions get made across a multinational. As long as AI sits there, the doctrine is structurally protected. The day it moves to its own office is the day the federation starts cracking.

Why This Answer Fits Allianz

The architecture of a federated regulated stack can be drawn on a single slide. The activation energy that puts a company in a position to draw it cannot be transferred the same way. This distinction matters because the natural reaction to a case study is "we should do this." The honest reading is "we can build the architecture, but the energy will take us a decade and several CEOs, and we may not have either." This is the gap between strategy and execution that most management frameworks understate. Three things had to happen for Allianz to be where it is now, and none of them can be compressed by reading about them.

First, the Business System itself. ABS started inside Allianz Elementar Austria as the Geschäftsfall-Bearbeitungs-System in the late 1990s. The German rollout alone cost roughly €500 million. The migration off the IBM mainframe to Linux/x86 ran from 2019 to Easter 2022, and the CTO described it as the riskiest project of his career. Roughly twenty years of standardization politics across seventy operating entities, plus a high-risk replatforming, before AI could land cleanly on top.

Second, the CDO federation. Most Allianz operating entities have their own Chief Data Officer reporting locally. The UK appointed Akhil Lalwani as CDO in June 2025. The structural pattern is one CDO per regulated entity. Building this network from zero — finding the people, granting them authority, negotiating their relationship with the entity CEO and with Group — takes years. Companies trying to retrofit it tend to end up with one Group CDO and a hollow operating-entity layer.

Third, brand-side restraint. Allianz has been the #1 insurance brand on the Interbrand ranking for seven consecutive years, with a brand value of $23.5 billion in 2024. That ranking lets Allianz use AI internally for productivity without needing to appear AI-first to defend its customer position. A challenger brand that hasn't earned that asset has to spend AI as marketing first and substrate second — which inverts the pattern and weakens it.

The Singapore Income Insurance episode is the cleanest illustration of how the doctrine has hardened. Allianz announced the S$2.2 billion acquisition in July 2024 and was blocked by the Singapore government three months later. Allianz withdrew the offer in December 2024. The earlier era of large inorganic bets — Dresdner Bank in 2001, €20 billion, sold for half that value seven years later — is over. The current era is "make and federate." Build the substrate. Run the intelligence layer on top of vendor models. Let each operating entity join when its regulator allows. The April 2026 Jio-Allianz India joint venture is the new template: a partnership, not a takeover, designed to be grafted onto the federation rather than absorbed.

Where It Goes Next

The next 18 months at Allianz are visible in the announced roadmap.

AllianzGPT 2.0 is the headline. The 2026 release is scoped to all 156,000 employees rather than the current 60,000-plus. If the 95% weekly engagement rate holds at full scale, AllianzGPT becomes the default work surface inside Allianz — the place where the median question gets asked and answered. That outcome would mean the intelligence layer has effectively absorbed the company's internal knowledge management, not as a project but as ambient infrastructure.

Claude inside motor and health claims is the second move. The Anthropic partnership names this directly. The pattern to watch is whether the Project Nemo design — multi-agent orchestration, human-in-the-loop authorization, entity-by-entity graft — replicates into higher-stakes claim categories. Motor claims are larger, more contested, and more regulated than AUD-500 food spoilage. The same architecture might or might not survive the higher stakes.

The third move is geographic. Jio-Allianz, the 50:50 India joint venture announced April 2026, is the freshest test of the "make and federate" doctrine. India is a different regulator, a different distribution model, and a different scale. If the joint venture uses ABS, the Data Platform, and AllianzGPT as the platform, the federated pattern is exporting itself into a fresh market. If it doesn't, the federation has a new exception to manage.

What is not visible in the roadmap is productization. Syncier's 2019 "ABS Enterprise Edition on Azure" has not produced disclosed external customer wins. There is no Allianz analog to Walmart Connect or STACKIT. The strategy is internal moat, not external platform. Unless that changes, the case stays a strategy piece rather than a product story.

The shape of the pattern becomes sharpest in contrast to Ping An. Ping An is trying to be the algorithm — proprietary models trained on a closed loop of customer data, with AI agents now fronting more than 500 services and roughly 60% of accident-and-health claims auto-settled, some in 51 seconds. The bet is that the algorithm itself is the moat. Allianz is trying to consume algorithms — OpenAI, Anthropic, DeepSeek interchangeable on a stable substrate, with the moat sitting in the Business System, the Data Platform, customer trust, and the federation's regulatory geography. Both readings can be right. They are different patterns, not different stages of the same one. The reason matters: a multinational federation cannot bet on a proprietary algorithm because no single algorithm is licensed to operate in seventy jurisdictions. The choice is structurally made by the operating model, not selected against alternatives.

When the Pattern Travels — Four Diagnostics

Four questions separate companies where this pattern can land from those where it cannot. They read as diagnostics, not prescriptions, and they apply to any multinational running AI on top of regulated infrastructure.

Substrate fragmentation. Companies whose front-line teams pull data from one substrate and those that pull from seven behave very differently when AI is layered on top. AI tools deployed on fragmented data return fragmented answers, and the expensive work — the part that takes a decade — is the substrate itself, not the model. Organizations that skip substrate consolidation because the AI demos look like the value tend to rebuild it later under harder conditions.

Measurable productivity. A useful test is whether AI productivity gain can be stated as a basis-point change in a unit-cost or expense ratio that the company already reports. Allianz's analysts put the figure at roughly 60 basis points per year off the P/C expense ratio. Companies whose AI programs cannot be expressed in a quarterly P&L metric are running research budgets, not productivity programs, and the distinction matters at the next planning cycle.

Board-level governance. Governance that lives inside legal, compliance, or risk as a check-the-box function tends to produce AI use that fragments by team. Governance that lives at the Board level — with an advisory body that meets, documents decisions, and has the authority to stop deployments, and with named officers in every operating unit — tends to produce AI use that scales across the federation. The structural location of governance is one of the cleaner predictors of whether AI becomes a norm or stays a series of pilots.

The inflection point. Companies that can name three concrete forces converging in a specific year tend to clear their next budget review. For Allianz, those forces are generative-AI maturity reaching production grade in 2023; combined-ratio pressure making productivity the only free lever inside Solvency II constraints; and Bäte's legacy plan running to 2027 with AI as the named productivity engine. Companies that cannot name three such forces are usually mistiming the strategy, and the strategy will not survive its first contact with finance.

References