Delta Air Lines

12

min read

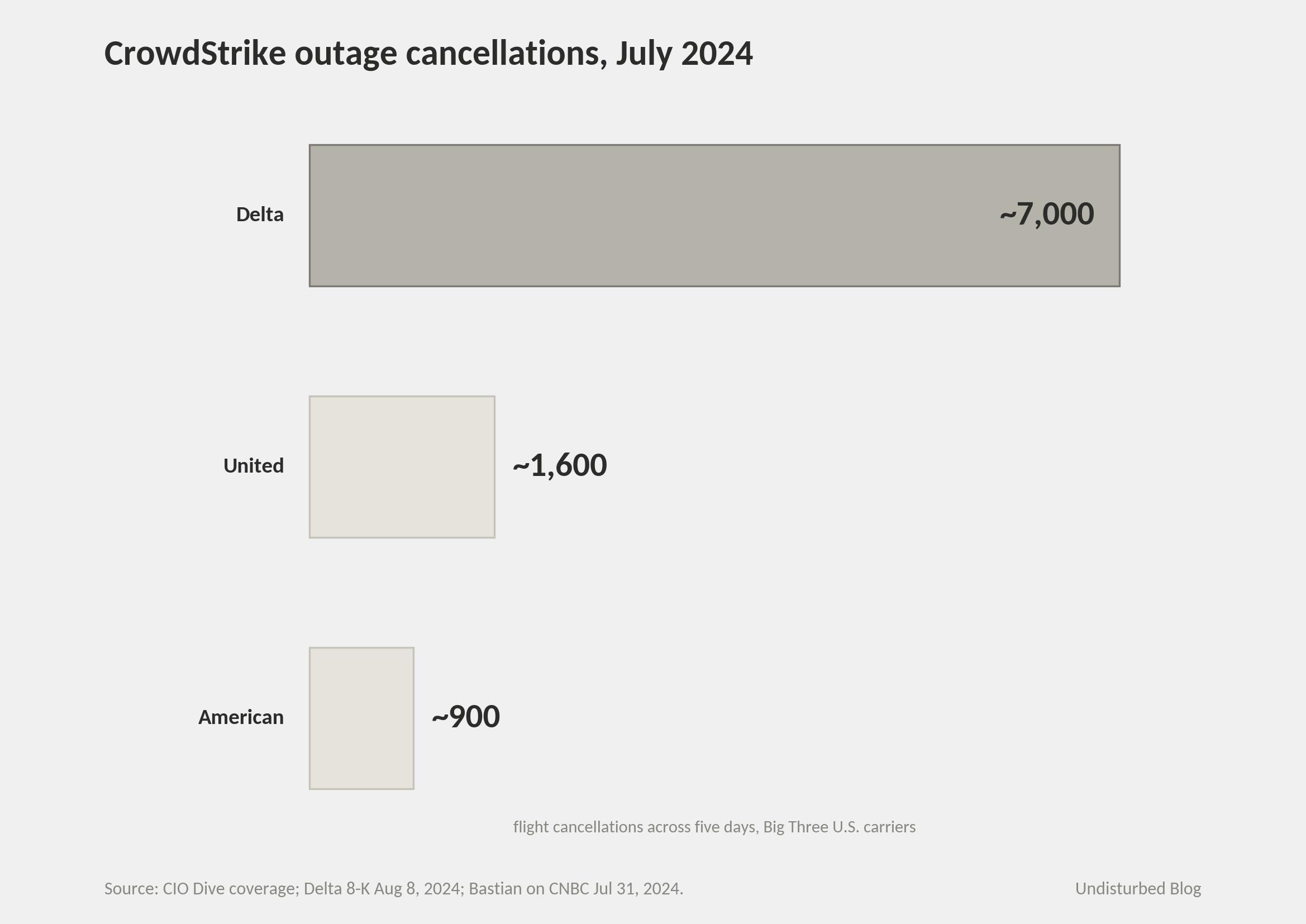

Delta's centennial year and three live AI surfaces arrived in the same calendar window. Fetcherr-powered dynamic pricing scaled from 1% of domestic fares in late 2024 toward a 20% target set for end-2025; APEX and Skywise predictive maintenance ran across roughly 990 aircraft; Delta Concierge, a generative-AI assistant, opened in beta to SkyMiles members on October 29, 2025. The same window contained the CrowdStrike outage of July 19, 2024 — a bad kernel update on Microsoft Windows that took down a reported 60% of Delta's mission-critical apps, forced 40,000 servers to be rebooted by hand, drove roughly 7,000 cancellations across five days, and cost a half billion dollars by Ed Bastian's own count on CNBC. Inside Delta the contrast wasn't framed as a contradiction. It was framed as a clarification.

When physical assets and operational reliability define the product, AI lands as a separate fast-clock layer on top of a slow-clock substrate. The substrate doesn't speed up — and the speed of the AI line is set by the integrity of the substrate, not the cleverness of the model. Delta's centennial isn't background context for the AI strategy. It is the AI strategy.

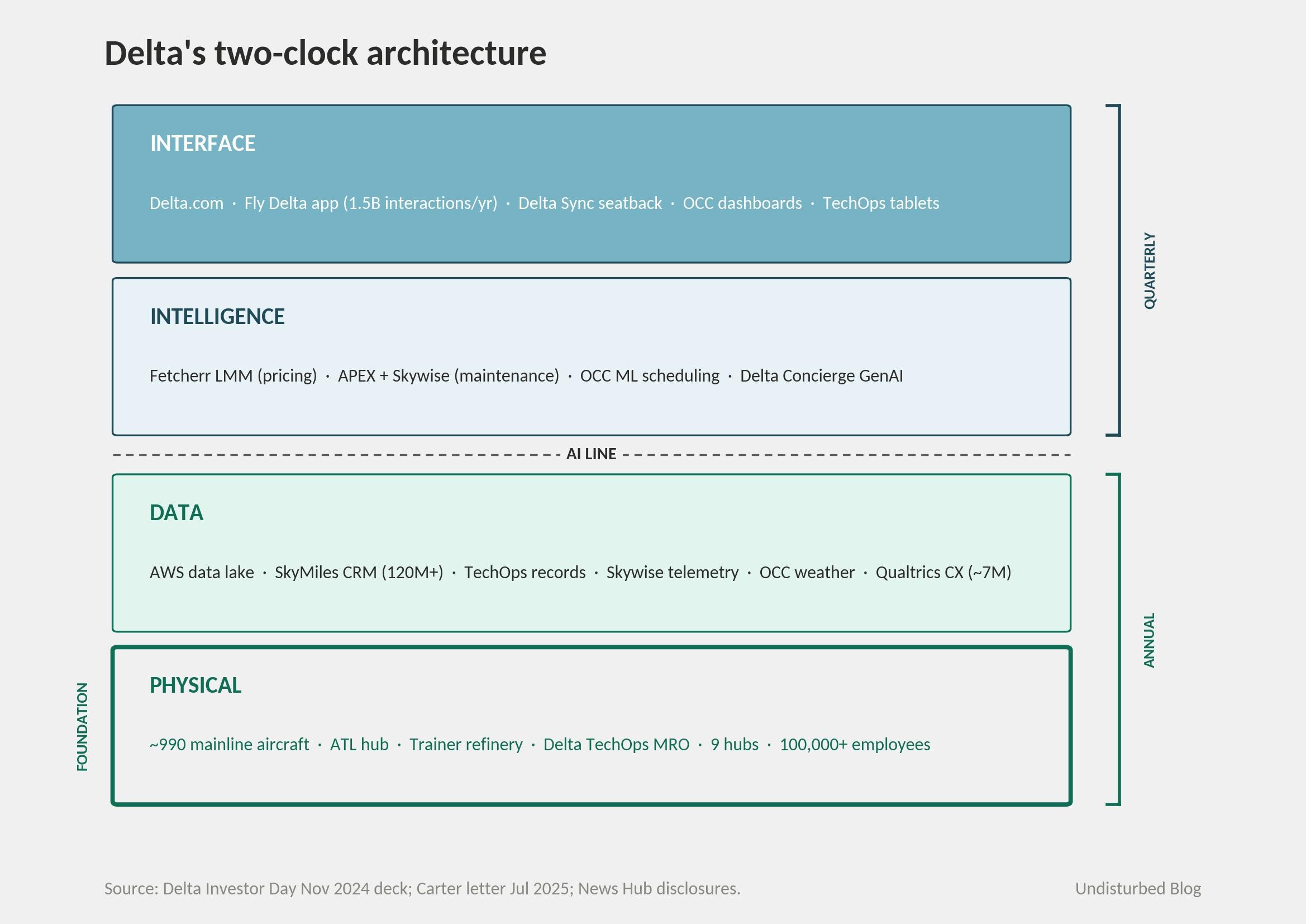

The Strategy in One Picture

Delta itself doesn't draw its strategy as four layers. But once you read the November 2024 Investor Day deck and the July 2025 letter Peter Carter sent to three U.S. senators, the four layers fall out cleanly.

The diagram does two jobs at once. It shows that Delta runs on two clocks — a slow one for fleet renewal, refinery operations, hub real estate, MRO infrastructure, and the data exhaust they produce; and a fast one for the AI models and the digital surfaces they feed. And it shows where the AI line actually sits: between the model and the data, not between the model and the customer.

That second point matters more than it sounds. United, American, and Delta all have AI projects. What separates Delta is that the AI line is drawn just above a substrate Delta has spent a century building.

The AI line, in a company like Delta, is whatever line — when crossed in either direction — slows the other side down. Above it: intelligence and interface, iterating quarterly. Below it: data and physical, iterating annually or slower. Compressing the slow layer with AI is a familiar trap; aircraft refits and hub real estate don't speed up because a model says they should. Slowing the fast layer to match cedes the customer surface. Delta's choice is to keep the layers on different clocks and police the seam between them. The line is a discipline, not a diagram.

How It Actually Works — Three Closed Loops

Three AI surfaces went live on the same substrate. Each closes a loop back into the data layer; none runs as a one-way pipe.

The pricing loop.

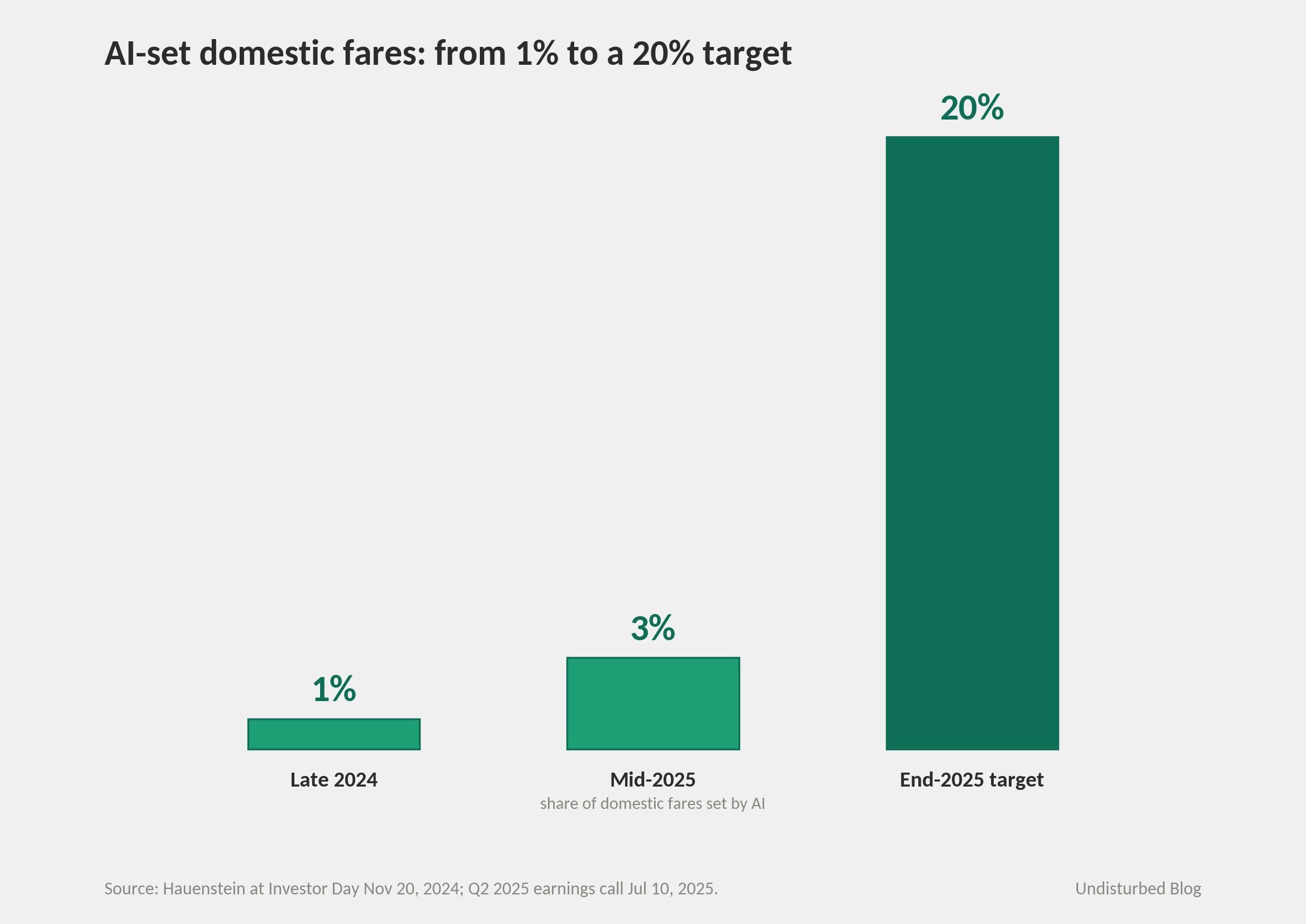

Glen Hauenstein, Delta's president, owns the Fetcherr program. Fetcherr is a Tel Aviv startup founded in 2019; its Generative Pricing Engine runs on what it calls a Large Market Model — a transformer trained on demand and inventory signals rather than language. SkyMiles purchase events and route demand flow into Delta's AWS lake, are stripped of personal identifiers, and feed the model. The model returns a fare; the fare appears on Delta.com or in the Fly Delta app; the booking — or the abandonment — flows back. At the November 2024 Investor Day, Hauenstein characterized AI as a super analyst working around the clock; by the July 2025 earnings call, the share of domestic fares set by AI had moved from roughly 1% to roughly 3%, with a year-end target of 20%. The loop is tight precisely because Delta keeps Fetcherr on aggregated inputs only — a doctrinal choice that became more important when Senators Ruben Gallego, Mark Warner, and Richard Blumenthal sent their July 2025 letter demanding answers about individualized pricing.

The operations loop.

Roughly 990 mainline aircraft, plus regional partners, generate sensor and telemetry streams continuously. The Airbus Skywise platform handles the Airbus fleet; APEX, Delta TechOps' in-house engine forecasting program, handles the engine side. APEX moved Delta's predictive material demand accuracy from about 60% to over 90% and won the 2024 Aviation Week Network Grand Laureate Award. Predictions feed into mechanic interfaces — replace this component within X flight hours — and outcomes feed back into the model. Maintenance-related cancellations have fallen from roughly 5,600 in 2010 to about 55 in 2018, on Delta's own count. The Operations & Customer Center, anchored by the largest in-house meteorology team at any U.S. airline, ingests the same telemetry plus weather, crew, and dispatch feeds, and runs ML scheduling tools that Carter's July 2025 letter describes as anticipating where crew replacements will be needed.

The customer loop.

Ranjan Goswami, who became Delta's chief marketing and product officer in April 2026, owns the customer-facing AI surfaces. Delta Sync, launched in 2023, recognizes a SkyMiles member at the seatback by birthdate and tailors the experience — the smart-TV move done for an airline cabin. Delta Concierge, first introduced as a concept at CES 2020 and re-launched as a generative-AI assistant at CES 2025, went into beta to SkyMiles members on October 29, 2025. Fly Delta app interactions ran to about 1.3 billion in 2024 and over 1.5 billion in 2025. Each interaction is a row in the lake; each row sharpens the next recommendation. Delta works with Qualtrics on the customer-experience layer; Qualtrics analyzed roughly 7 million Delta customer records during 2024.

What's the same about all three loops? The intelligence layer reads from and writes back to the same substrate. The pricing model and the maintenance model are different; the data lake they share is not.

The Numbers

For FY2024, Delta reported revenue of $61.6 billion, pretax income of $5 billion, operating cash flow of $8 billion, and free cash flow of $3.4 billion. For FY2025, revenue reached $63.4 billion, with free cash flow guidance raised to $3.5–4 billion and year-to-date return on invested capital of 13%. The American Express co-brand remuneration — the financial expression of SkyMiles data — moved from $7.4 billion in 2024 to roughly $8 billion in 2025, with a publicly stated long-term target of $10 billion. Premium and loyalty together accounted for 57% of FY2024 revenue.

The AI-attributable numbers, where Delta has put them on record, are narrower but specific. APEX moved engine material demand accuracy from 60% to over 90% and saved an eight-digit dollar amount, per the Aviation Week Network's 2024 Grand Laureate citation. Skywise predictive maintenance runs at over 95% accuracy on flagged components. Fly Delta app interactions ran to 1.3 billion in 2024 and over 1.5 billion in 2025 — Bastian's CES 2025 figure and Eric Phillips' Q4 2025 disclosure, respectively. Maintenance-related cancellations fell from roughly 5,600 in 2010 to 55 in 2018. Hauenstein's pricing ramp — 1% to 3% to a 20% target across 2024 and 2025 — is the fastest-moving number in the stack.

Delta TechOps as a third-party MRO booked roughly $1 billion in revenue mid-2025, with full-year 2025 guidance of about $1.2 billion and a long-term aspiration of $5 billion. That's a separate third-party-services play; the relevant point here is what it implies about the substrate. A maintenance organization the rest of the industry pays Delta to use is exactly the sort of slow-clock asset that earns the right to put AI on top of it.

The pricing ramp deserves a second look. The 20% target for AI-priced fares is a deployment number, not a revenue-uplift number. Hauenstein hasn't disclosed a separate uplift for Fetcherr fares versus traditional fares; the closest public figure is Fetcherr's own marketing claim of 6–9% RASM uplift across its airline customers. The 20% is the share of fares the model is permitted to set without a human in the loop on every transaction. Reading it as a 20% pricing improvement is the wrong arithmetic. The right reading is that Delta's willingness to let the machine touch one fifth of domestic fares — before the next round of negotiation with regulators, with the public, with ALPA — reframes what controlled rollout actually means.

AI as Norm: The Succession Test

Three surfaces, three named owners, three loops back to the same lake — that's not three pilots. Hauenstein owns pricing; Don Mitacek and the OCC duty directors own operations; Goswami owns the customer side. Above them, Amala Duggirala arrived in January 2026 as Chief Digital & Technology Officer, taking over from Rahul Samant, who had run IT through the cloud migration and the CrowdStrike response. Duggirala's mandate combines IT and digital — the scaffolding for one substrate, many AI workloads, one accountable executive.

The harder test is succession. Bastian became CEO in May 2016. His CES keynote rhythm — 2020, 2023, 2025 — has paired with each major step in the digital agenda; the 2025 keynote at the Las Vegas Sphere was framed explicitly as a centennial reset. The November 2024 Investor Day deck identifies "Integrated Data & Analytics" as foundational, with modernized platforms below it and the connected digital experience and revenue-premium capabilities sitting on top. That's the four-layer stack in Delta's own slide template, before any analyst draws it. If the next CEO inherits that deck and the named owners that go with it, the norm survives the executive.

Norm at this depth travels through the org chart, not through the press release: a CDTO who answers to the CEO, named owners on each AI surface, doctrine codified in the response letters Delta files with regulators. By those criteria Delta is past the pilot phase. The harder version of the test will come when crew scheduling AI confronts ALPA in the December 2026 contract round. That's when norm stops being an organizational claim and starts being a labor-relations one.

What does Delta's normalization look like to the rest of the industry? The Big Three have publicly diverged on AI pricing. American Airlines CEO Robert Isom called AI-priced fares "bait and switch" in a July 2025 PBS NewsHour interview and pledged American would not deploy them. United Airlines, under Scott Kirby, markets aggressively on Starlink Wi-Fi and a tech-forward fleet plan but has been quieter on the pricing surface. Delta sits alone in publicly defending AI-set fares while explicitly walling off personal identifiers — a doctrinal stance that's now the single most visible disagreement in U.S. legacy aviation.

Why This Answer Fits Delta

Delta has owned a refinery since April 30, 2012. Trainer, Pennsylvania, bought from Phillips 66 for about $150 million plus capex, run through Monroe Energy LLC; covers roughly 13% of East Coast refining capacity; gives Delta a 4–11¢ per gallon jet fuel cost advantage in the Northeast. No other airline owns one. Delta TechOps sells maintenance services to over 150 third-party customers. Atlanta — the world's busiest airport for 27 of the last 28 years — runs at 73% Delta share; ATL is closer to a Delta facility that other airlines also use than a neutral hub. None of this is AI strategy. All of it is the substrate the AI strategy sits on.

The pattern is consistent: Delta's instinct is to own the production layer. That's why the Fetcherr partnership stands out as the doctrinal exception. A Tel Aviv startup founded seven years ago, running pricing for Delta and a handful of carriers Delta has equity stakes in (Virgin Atlantic, WestJet) — that's a deeper external dependency than Delta typically tolerates. Delta's mitigation is the no-PII architecture, the decision-support framing, the controlled rollout. Carter's letter to the senators in July 2025, more than the CES keynote in January, is the strategy document — a public commitment to where the AI line sits.

The CrowdStrike outage of July 19, 2024, is the moment this all came into focus. A bad CrowdStrike kernel update on Microsoft Windows took down a reported 60% of Delta's mission-critical apps. Forty thousand servers were rebooted by hand. Delta's recovery — about 7,000 cancellations across five days, against roughly 1,600 at United and 900 at American — was the slowest of the Big Three. The point isn't who's at fault; the point is that a fast-clock IT failure proved the slow-clock substrate is binding. Faster AI on top of a fragile data layer is a worse airline, not a better one. The investments Delta has made since — completing the AWS migration, renewing the Kyndryl infrastructure deal, suing CrowdStrike — are all slow-clock investments in the substrate. They don't show up in the Fetcherr ramp. They make the Fetcherr ramp possible.

The architecture itself — four layers, AI line in between, three closed loops, named owners — is transferable. Other carriers can read the same Investor Day deck and copy the slide. What doesn't transfer is the activation energy: a refinery owned for fourteen years, a hundred-year MRO operation, a hub running at 73% share, an Amex partnership generating $8 billion a year in remuneration, a meteorology team forecasting weather for the OCC. Those took decades to build. The AI line works at Delta because what's underneath it has been compounding for a century.

Where It Goes Next

Three things are worth watching over the next year.

The first is the regulatory window on AI pricing. The July 2025 Senate letter, the Casar–Tlaib bill, and FTC interest in personalized pricing together define a policy environment that isn't yet rules. Delta's stated strategy was to ramp inside the window — reach 20% by end-2025 — while explicitly disclaiming PII use, on the theory that a fait accompli with no privacy violation is hard to undo. If the Senate letter becomes a hearing, the doctrine will be tested in public.

The second is the December 31, 2026 ALPA contract amendable date. AI-driven crew scheduling runs into seniority-based open-time rules and — at Delta specifically — an open dispute over the pilot scheduling software. Delta's mainline pilot group has flagged scheduling-software issues during recent IROPS events; ALPA Master Executive Council Chair Eric Criswell has been public about it. Whether the next contract gives Delta room to push AI into crew scheduling is the labor-relations test of normalization.

The third is the asset cycle. Eighty 717-200s are nearing the end of their service life; the A220 is replacing them. The A350-1000 arrives later in 2026 with cloud-based 4K seatback IFE, the Hughes dual-network connectivity, and 96 TB of onboard storage from Thales. None of this is AI. All of it is the slow-clock substrate refresh that lets the fast-clock surfaces stay fresh. The pattern only works if the layer underneath also moves — just slower.

The architecture travels; the conditions don't always travel with it. Four conditions surface across the case. The data has one address: Fetcherr, APEX, and Concierge close their loops against the same AWS lake, not three different systems of record. The AI numbers are read for what they are — the 20% pricing target is a deployment metric, not a revenue uplift, and Delta hasn't blurred the two. Normalization shows up on the org chart: named owners on each surface, a CDTO reporting to the CEO, doctrine codified in regulator-facing letters. And the substrate beneath the AI line is a compounding asset — refinery since 2012, MRO going back to the airline's earliest decades, ATL share since the post-merger consolidation — not a recently assembled tech stack. Where any one of those four is missing, the line doesn't hold.

References