Singapore Airlines

15

min read

Singapore Airlines runs 205 aircraft — including the world's largest A350 fleet — out of a single hub at Changi, with a separately listed maintenance subsidiary, SIA Engineering Company (SIAEC), that holds approvals from 28 national regulators and operates the largest Trent engine MRO joint venture in the world. These are assets that take a decade to change. On top of this slow substrate, SIA has layered AI tools that change every quarter: SITA OptiClimb for climb-phase fuel optimization on the A350, the KLM-BCG Pathfinder suite for tail and disruption optimization at Operations Control, Rolls-Royce Engine Health Monitoring for the Trent fleet, and the A*STAR-built SAAVIS robotic visual-inspection system for hangar work. CEO Goh Choon Phong reported in March 2025 that SIA had developed more than 250 generative AI use cases in the previous 18 months and implemented around 50 across end-to-end operations. FY2024/25 revenue reached a record S$19.5 billion; net profit a record S$2.78 billion.

The pattern underneath is what makes SIA worth studying. In asset-heavy industries, the intelligence layer is something to rent, not build. The defensible edge is not the algorithm — it is the operating speed at the seam where rented intelligence meets owned execution, and the R&D substrate that lets a company move from buyer to co-developer when the algorithm finally matters.

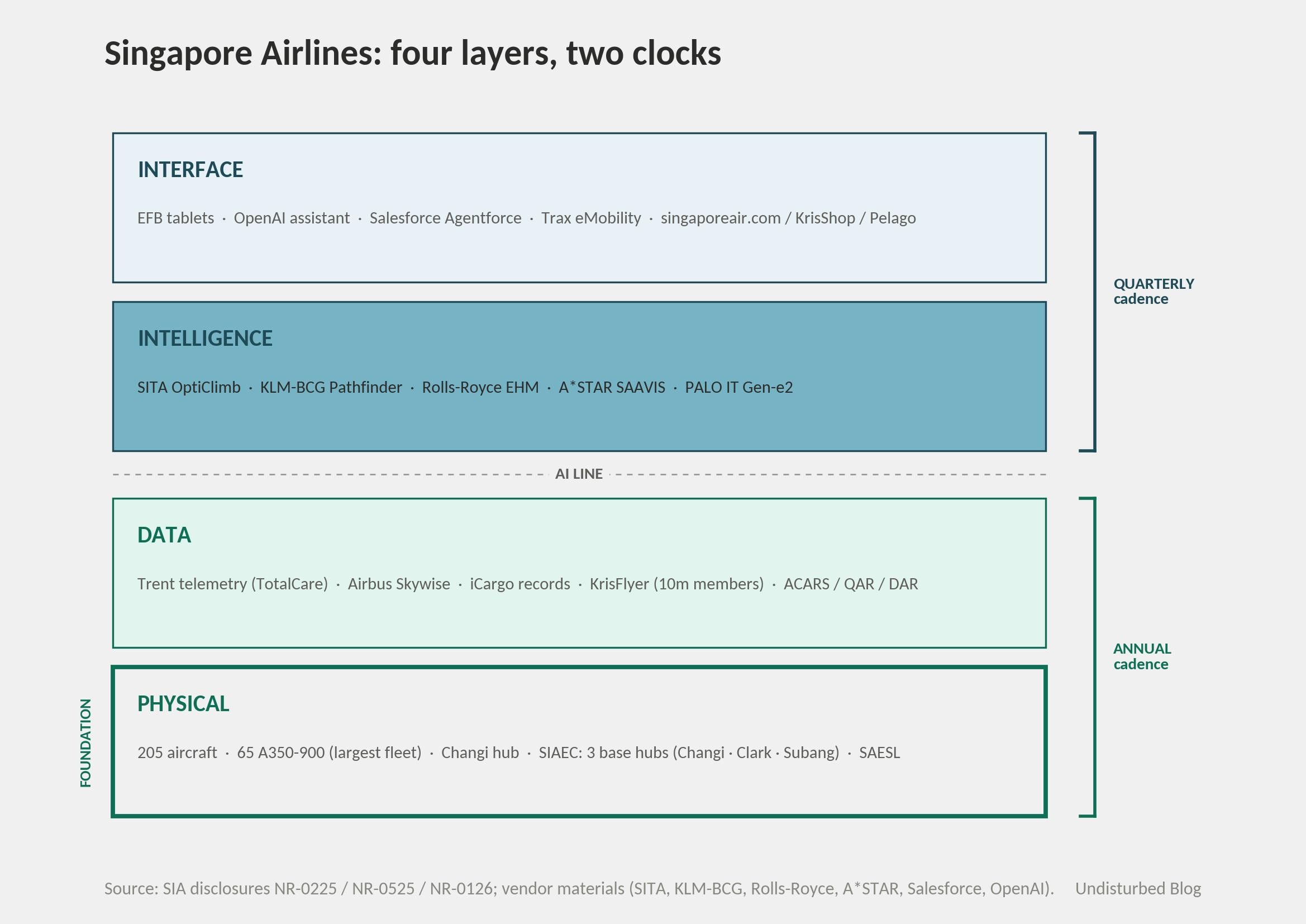

The Strategy in One Picture

SIA itself does not draw its strategy this way. But once the four layers are laid out, the company's pattern is unusually clean.

The horizontal "AI line" is the structural insight. Above it, things move on a quarterly cadence: vendors push releases, models retrain, dashboards refresh. Below it, things move on a multi-year cadence: aircraft order books are set out to 2030, hangars are leased on 15-year terms, engine maintenance contracts run a decade. The two clocks are deliberately different. SIA is not trying to make the bottom faster; it is making the top usable.

What is unusual at SIA is that almost every entry in the intelligence layer is a vendor name. SITA. KLM-BCG. Rolls-Royce. IBS. RateGain. The exceptions are the SIA-NUS Digital Aviation Corporate Lab and the SAAVIS / "AI for Airline Operations" projects with A*STAR. The intelligence layer at SIA is mostly rented; the R&D substrate behind it is owned.

This makes SIA's profile distinct from a vertically integrated logistics operator like FedEx, which builds much of its intelligence layer in-house: routing engines, sort-center optimization, network simulation. SIA's intelligence layer is, with two exceptions, a portfolio of subscriptions sitting on top of OEM-owned data layers — Skywise belongs to Airbus, EHM to Rolls-Royce, OptiClimb to SITA. This is not a weakness. The architecture only requires that the layers move at different clocks. It does not require that the same company own all four. SIA's bet is that the intelligence layer is becoming a market, and that operators who rent fluently will out-execute operators who build slowly.

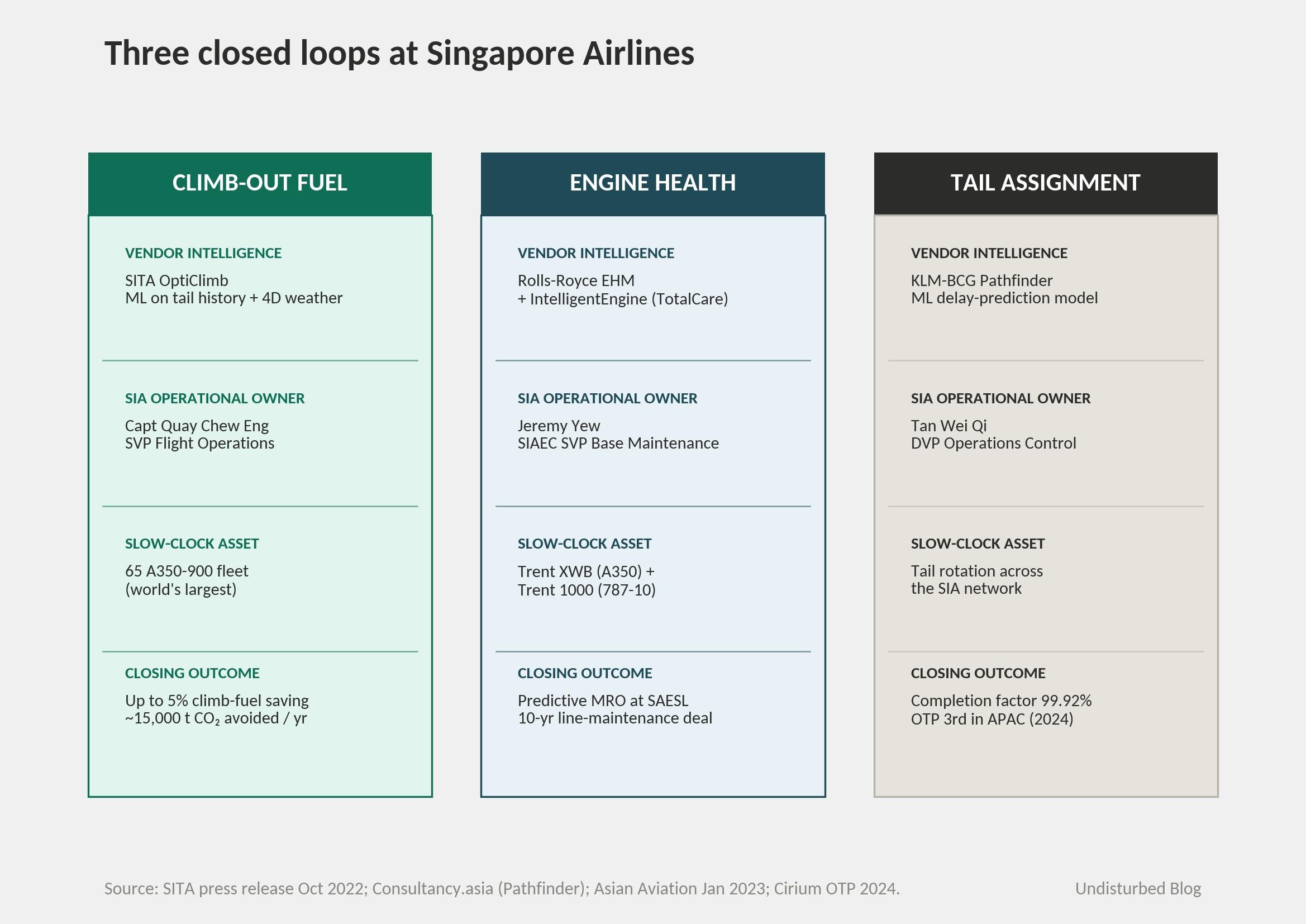

How It Actually Works — Three Closed Loops

Three operational loops show how rented intelligence translates into owned execution at SIA. In each, the algorithm runs on the fast clock, the asset on the slow clock, and a named person at SIA owns the seam between them.

Loop 1 — Climb-out fuel.

SITA OptiClimb has run on SIA's A350 fleet since August 2022. The system uses tail-specific machine learning trained on each aircraft's historical performance, combined with high-resolution 4D weather forecasts, to recommend three customized climb-speed setpoints that the pilot enters into the flight management system during cockpit prep. SITA's published claim is up to 5% fuel savings during climb-out per flight; for SIA's A350 fleet, around 15,000 tonnes of CO₂ avoided per year. Capt Quay Chew Eng, Senior Vice President Flight Operations, owns the deployment.

The loop closes inside SITA's data infrastructure, not inside SIA's: actual flight data from each climb feeds back into the tail-specific model, which improves over thousands of flights. SIA contributes the operational discipline — pilots actually entering the recommended setpoints — and the consequences of the savings flow to SIA's fuel line. The intelligence belongs to SITA. The decision and the outcome belong to SIA.

Loop 2 — Engine and airframe health.

The Trent XWB engines on SIA's A350 fleet, and the Trent 1000 engines on the 787-10s, stream telemetry continuously through Rolls-Royce's Engine Health Monitoring system, which feeds the TotalCare service contract. Rolls-Royce's IntelligentEngine program runs digital twins, novelty detection, and remaining-useful-life prediction over this stream. SIAEC sits on the operational side: in January 2023, SIAEC and Rolls-Royce signed a ten-year line-maintenance agreement covering the Trent 7000, 1000, 900, 800, 700, 500, and XWB. Borescope inspections, on-wing interventions, and shop visits at SAESL — the SIAEC/Rolls-Royce joint venture in Singapore that is the world's largest Trent MRO — are scheduled by what TotalCare's analytics suggest, not by fixed calendar.

In parallel, SAAVIS — the Smart Automated Aircraft Visual Inspection System, developed by ASTAR's I2R and IHPC institutes with SIAEC and ST Engineering — uses computer vision and AI to replace what was previously a roughly two-engineer, two-hour manual visual sweep. And a three-year joint project between SIA, SIAEC, and ASTAR is building predictive analytics for component failure paired with optimization of maintenance interval, workflow sequence, manpower, and resource allocation. Jeremy Yew, SIAEC Senior VP Base Maintenance, owns the new BMM hangar in Subang, Malaysia, where Trax eMRO and eMobility went live as a paperless operation from inception in 2025.

The honest read: the predictive intelligence on the engines belongs to Rolls-Royce. SIA owns the consequences — dispatch reliability, AOG cost, schedule integrity — and the operational discipline to act on what the OEM tells it.

Loop 3 — Tail assignment and disruption.

Pathfinder, the AI/ML and optimization tool built by KLM and BCG X, runs at SIA Operations Control. It uses an ML-based delay prediction model to recommend where to place schedule buffers and how to assign tails to flights in the days leading up to operations. Tan Wei Qi, Divisional VP Operations Control, owns the deployment. The official statement frames the value as "quicker data-driven decisions," "reduced fuel burn," and "reduced flight disruptions." Cathay Pacific runs the same KLM-BCG suite — the algorithm is not the moat. SIA's edge is the speed and discipline of the OCC where the algorithm's recommendations meet a real operations decision.

What makes these three loops genuinely closed is not the AI. It is that each loop has an operational owner inside SIA who converts vendor intelligence into a tail rolling onto a runway, an engine staying on wing, or a buffer absorbing a delay. Without that seam, an AI deployment is a demo. With it, it is a loop.

The Numbers

The financial baseline is unambiguous. FY2024/25 group revenue reached a record S$19.5 billion (up 2.8% year-on-year), and group net profit a record S$2.78 billion — though the headline net profit included roughly S$1.1 billion of non-cash gain from the Air India / Vistara merger. Group operating profit, the cleaner operational measure, was S$1.71 billion, down 37% as yields normalized post-pandemic. Through the first nine months of FY2025/26, the group recorded S$15.2 billion revenue and S$743 million net profit. Cash and bank balances stood at roughly S$8.3 billion at March 2025, providing the balance-sheet capacity for the S$1.1 billion A350 long-haul and Ultra-Long-Range cabin retrofit and an order book of 78 aircraft including 31 Boeing 777-9s.

On the AI and digital side, the most quoted single disclosure remains Goh Choon Phong's March 2025 statement that SIA Group had developed "over 250 use cases over the last 18 months and implementing around 50 initiatives across our end-to-end operations." This is the broadest organizational signal that AI is no longer an isolated workstream. Specific operational numbers are sparser:

SITA OptiClimb: up to 5% climb-out fuel savings per flight; roughly 15,000 tonnes CO₂ avoided per year on the A350 fleet (SITA disclosure, October 2022).

PALO IT Gen-e2 proof-of-concept: an 11-week development cycle compressed to 5 weeks, with 95% of code, documentation, architecture diagrams, and infrastructure-as-code AI-generated; the program is now scaling to roughly 700 SIA developers.

IBS iCargo at the first months post-go-live (August 2022 onward): around 1,500 users, 24,000 flights, 202,000 bookings, 192,000 air waybills, 8.5 million messages processed.

KrisFlyer membership crossed 10 million in March 2025, up from 8.8 million a year earlier.

SIA-NUS Digital Aviation Corporate Lab: S$45 million committed, five-year horizon, target of 70-plus researchers and PhDs trained.

On-time performance: SIA ranked third in Asia-Pacific in 2024 (Cirium), up from seventh in 2023; completion factor 99.92% in 2023.

Net fuel cost was roughly 29% of total expenditure in 1H FY2025/26 — material enough that climb-out optimization compounds, but not so dominant that AI on fuel alone reshapes the P&L.

The named program owner picture is intentionally distributed. Goh Choon Phong is the institutional sponsor — appointed CEO 1 January 2011, MIT-trained in computer science, and notably the former SVP Information Technology at SIA. Choo Mun Fai, VP Digital Innovation, owns the Generative AI Blueprint. Operational AI sits with line VPs: Quay on fuel, Tan Wei Qi at Operations Control, Yew at SIAEC base maintenance, Marvin Tan in Cargo. The structural choice is meaningful — SIA does not have a single Chief AI or Chief Digital Officer with end-to-end authority. Each loop is line-owned.

A 250-use-case disclosure is the kind of number that lands well in a keynote and travels poorly under analysis. It does prove that AI has crossed the threshold from special project to organizational habit at SIA — that quantity is not achievable through a single innovation team. What it does not prove is operational vs customer breakdown, dollars saved per use case, or how many of the 50 implementations actually closed a feedback loop versus running as one-shot tools. Stripped down: 250 use cases is evidence of an AI-literate organization. The evidence that AI is reshaping unit economics has to come from somewhere else — at SIA, the operational metrics, not the AI disclosures.

Is AI a Norm Inside Singapore Airlines?

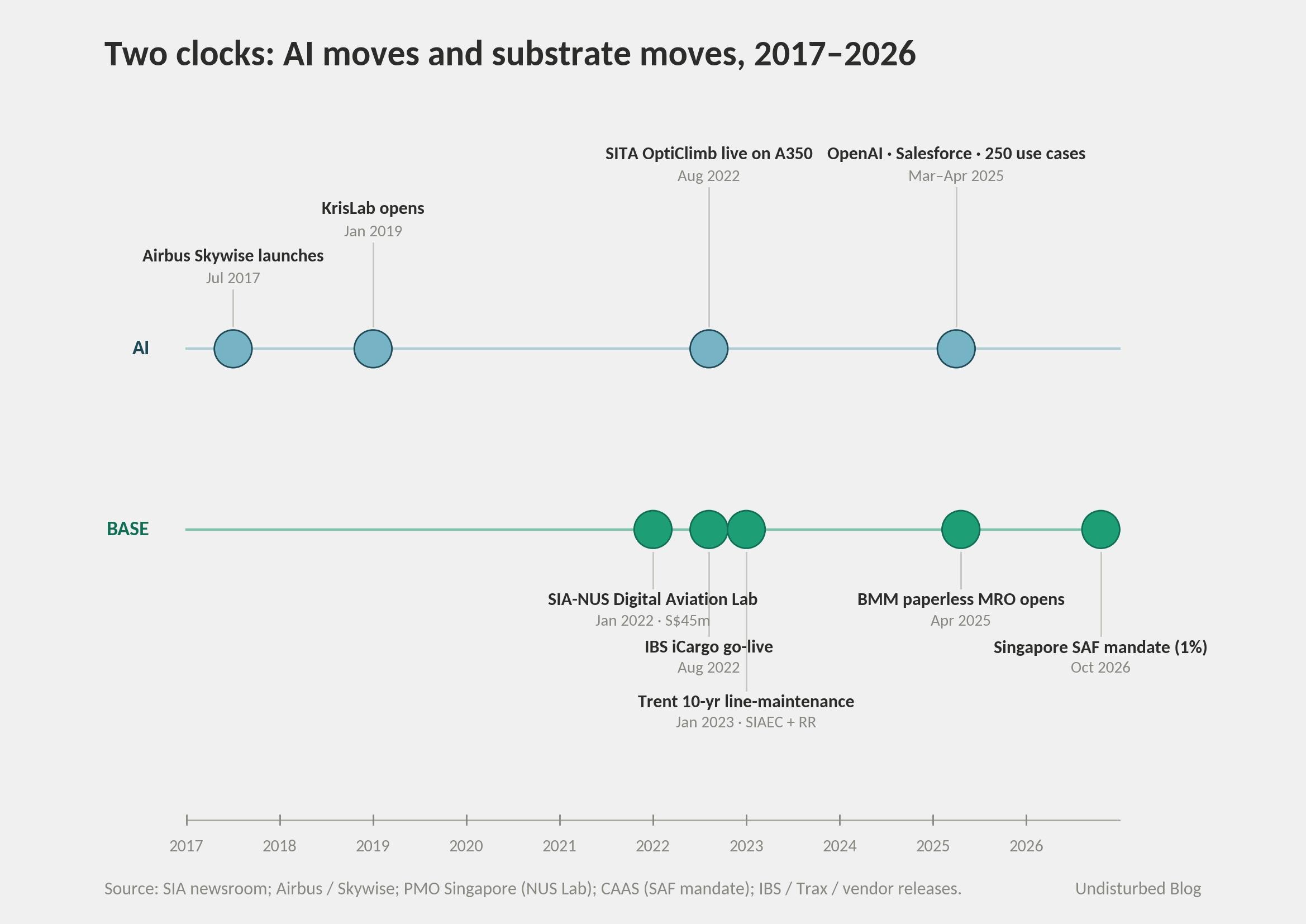

The strongest evidence that AI is institutionalized at SIA — rather than person-dependent — is structural rather than rhetorical. KrisLab, the Digital Innovation Lab inside SIA Group Sports Club, opened in January 2019 with explicit funding for employee-submitted prototypes. The Generative AI Blueprint, run by Choo Mun Fai, deliberately includes "managing associated risks with practical governance" — doctrine, not project list. The SIA-NUS Digital Aviation Corporate Lab funds 70-plus PhDs over five years, which means the company is committing to AI-literate engineers in 2030, not just in 2026.

Spread across functions confirms the same picture. AI shows up in flight operations (OptiClimb), operations control (Pathfinder), engineering and base maintenance (EHM, SAAVIS, the SIA-SIAEC-A*STAR project), MRO (Trax at BMM), cargo (iCargo, AirGain pricing), software development (Gen-e2 across roughly 700 developers), and customer-facing service (Salesforce Agentforce, OpenAI integration). The PALO IT account suggests procurement velocity has shifted: a discussion that would normally have taken four to five months collapsed into a fast yes when the AI angle was clear, which reads more like an organizational reflex than a one-off decision.

What is harder to confirm is the deeper test. The real test of whether AI is a norm at a company is not the number of use cases — it is whether the strategy survives the CEO who built it. SIA has not been tested on this. Goh Choon Phong has been in seat for fifteen years and is himself an MIT computer scientist who came up through SVP Information Technology — the digital agenda is not delegated to him, it is him. The institutional pieces (KrisLab, the NUS lab, the state-level partnerships with CAAS, A*STAR, NUS, EDB, the integration into Singapore's National AI Strategy 2.0) are designed to outlast any CEO. The velocity — how quickly a Gen-e2 PoC gets a yes — is the personal layer. When Goh retires, the architecture should hold. The pace is the variable to watch.

Why This Answer Fits Singapore Airlines

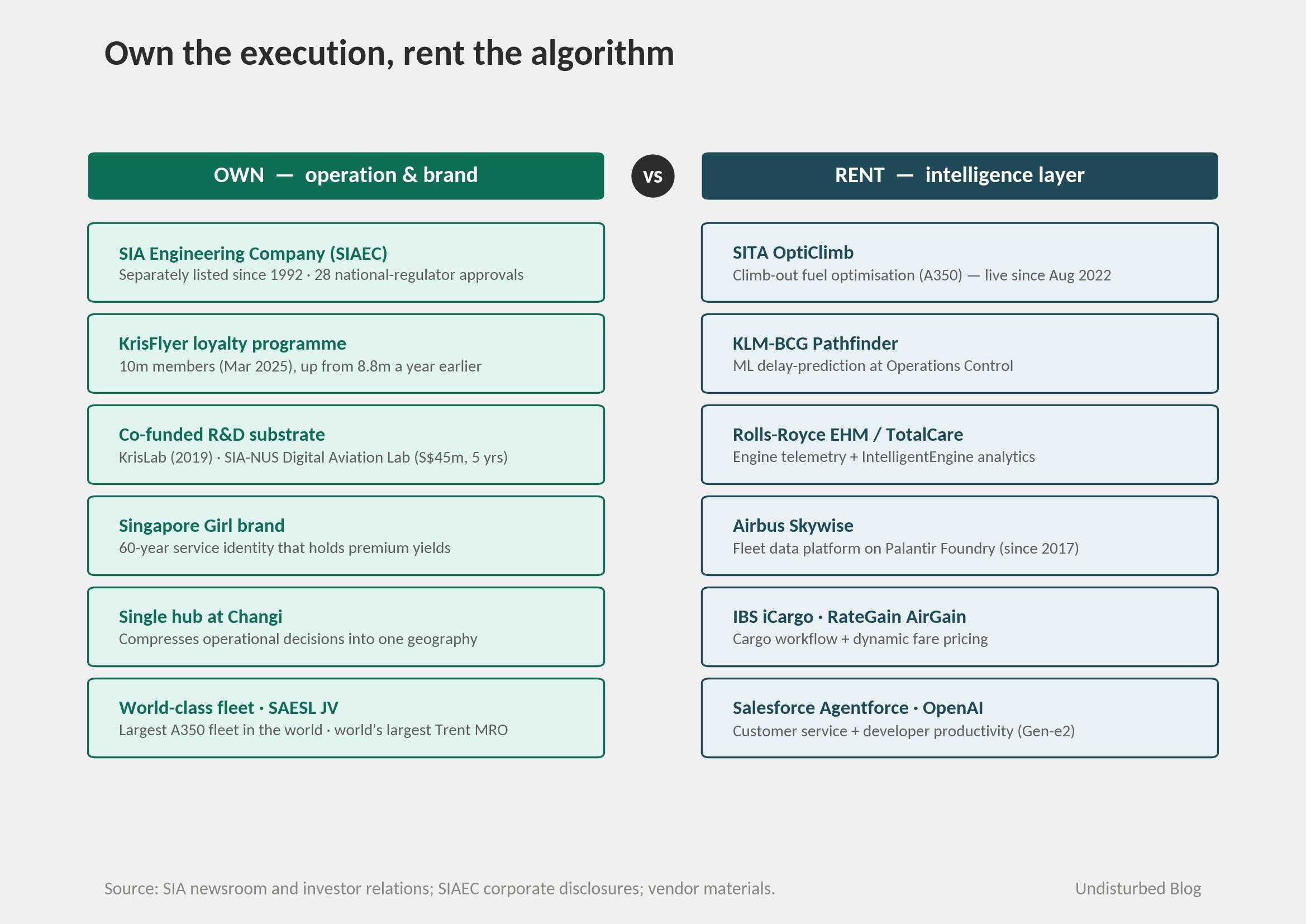

Three multi-decade facts about SIA make this rented-intelligence approach the natural fit.

The first is the operational excellence DNA. SIA's brand sits on the Singapore Girl, but the underlying organization has always run tight: launch customer for the A380 and the 787-10, operator of the longest commercial route in the world (Singapore-Newark on the A350-900ULR), operator of the world's largest A350 fleet today. A culture that obsesses over operational variance is exactly the culture that converts vendor algorithms into actual savings. OptiClimb's 5% climb-out savings are theoretical without disciplined pilot adoption; Pathfinder's recommendations are theoretical without an OCC that acts on them.

The second is the make-versus-buy pattern. SIA owns the things that travel with its brand and its operations: SIAEC has been separately listed since 1992; KrisFlyer is in-house; KrisLab and the NUS Lab are co-funded with state institutions. SIA buys the things that are commodity execution layers above the operations: aircraft from Boeing and Airbus, engines from Rolls-Royce and GE, AI optimization tools from SITA, KLM-BCG, IBS, RateGain, Salesforce, OpenAI. The pattern is consistent across decades — own the physical execution and the customer-facing brand; rent the algorithmic layer; co-invest in research with state partners, enabling a shift from buyer to co-developer when the algorithm starts to actually matter.

The third is Singapore. Temasek holds roughly 51-56% of SIA voting stock (the figure varies by snapshot; the state's "golden share" exists but is described as non-interventionist). The Civil Aviation Authority of Singapore, the Economic Development Board, A*STAR, the National Research Foundation, and NUS form an unusually tight national R&D substrate around the airline. The S$45 million SIA-NUS Digital Aviation Corporate Lab is the 19th such corporate lab in Singapore, the 7th at NUS — this is industrial policy, not a corporate science project. Singapore's National AI Strategy 2.0 names SIA as a sectoral champion. No competitor airline in the region has this kind of state-aligned R&D infrastructure.

The "why now" inflection is concrete. COVID drove SIA's all-international model to roughly 3% of pre-pandemic capacity in April 2020 and forced a S$15 billion Temasek-underwritten recapitalization. Recovery into FY2023/24 and FY2024/25 — both record-net-profit years — funded reinvestment. Skywise (launched 2017 by Airbus on Palantir Foundry) and Rolls-Royce IntelligentEngine made airline-side AI feasible without massive in-house data engineering. The Air India / Vistara merger of November 2024 gave SIA a 25.1% stake in enlarged Air India and a second sensor footprint in the world's fastest-growing aviation market. And from October 2026, Singapore mandates a 1% Sustainable Aviation Fuel blend on departing flights with a passenger levy — every kilogram of fuel saved by AI now carries a higher economic value, by regulation.

The architecture at SIA is, in principle, copyable. Any major airline with Skywise access can buy SITA OptiClimb. Any operator running Trent engines can sit inside TotalCare. KLM-BCG sells Pathfinder to anyone, and Cathay Pacific has bought it. What is not copyable is the activation energy. Temasek-backed S$45 million corporate labs, A*STAR co-development, an NRF-funded research pipeline of 70-plus PhDs over five years, a single hub that compresses operational decision-making into one geography, and a 30-year operational-excellence brand that holds premium yields while the algorithms run underneath — these do not transplant. The architecture is the part executives in other airlines should study. The activation energy is the part they should resist trying to recreate from scratch.

Where It Goes Next

Three forces will shape the next eighteen months at SIA.

The first is the SAF mandate. From October 2026, all flights departing Singapore must include a 1% Sustainable Aviation Fuel blend, with a passenger levy from April 2026 and a target of 3-5% blend by 2030. SAF is multiple times more expensive than conventional jet fuel; SIA Group has already begun layering procurement (1,000 tonnes of neat SAF from Neste in May 2024, 2,000 tonnes of CORSIA-eligible book-and-claim from World Energy). The economic logic of the OptiClimb-class tools changes overnight when the marginal kilogram of fuel is more valuable. Expect deeper integration of fuel optimization into the cruise phase, not just climb-out — most likely through OEM platforms rather than in-house build.

The second is the generative AI scale-out. The PALO IT Gen-e2 program is moving from PoC to roughly 700 SIA developers. The OpenAI partnership announced in April 2025 explicitly calls out integration into "existing tools" for "complex tasks such as flight crew scheduling" — a partial bleed from customer-facing AI into operational scope. The Salesforce Agentforce relationship is co-developing airline-specific patterns through Salesforce's AI Research hub in Singapore. The interesting question is whether the GenAI initiatives compound into something architectural — a shared SIA platform layer — or remain a portfolio of vendor integrations. The current pattern suggests the latter, with the SIA-NUS Lab acting as the slow-clock R&D anchor.

The third is the multi-hub topology. The Air India 25.1% stake gives SIA a second large operational dataset and a second hub geography. If the integration runs through any of SIA's existing platforms — SIAEC for MRO, KrisFlyer for loyalty, the Pathfinder/OCC stack for operations — it converts a financial investment into a structural data advantage. If it runs as parallel infrastructure, the strategic value is more limited. Watch the operational integration disclosures over the next four quarters.

The architectural risk is concentrated, by design, in the intelligence layer. SIA's current model assumes that Skywise, TotalCare, KLM-BCG, SITA, and the rest will remain available on commercial terms. If any of those vendors moves toward vertical integration with operators or substantially repriced subscriptions, SIA's defensible position narrows. The SIA-NUS Lab and the A*STAR joint project are the partial hedge — research-grade today, potentially production-grade in the next architecture refresh.

Where the Pattern Actually Works

The architecture translates as a self-diagnosis, not a checklist. Four conditions separate companies where the rented-intelligence pattern compounds from companies where it stalls.

Substrate access. In companies where the pattern works, the people who actually make operational decisions have unified access to the data they need, on a single substrate, without re-keying or chasing IT. At SIA, pilots get OptiClimb recommendations as setpoints they can enter directly into the flight management system, and OCC controllers see Pathfinder recommendations alongside live operational data. The substrate is doing the work of integration. Where the pattern stalls, AI tools live in dashboards that operational decision-makers do not log into.

Defensible numbers. In companies where the pattern works, the value figures from AI initiatives are crisp enough to defend in a board meeting — specific savings, specific ROI, specific named programs and named owners. SIA's published numbers are uneven, but where they are crisp (15,000 tonnes CO₂ on A350, 44% time saving on Gen-e2 PoC, 250 use cases across the group), they survive scrutiny. Where the pattern stalls, the numbers stay at the "transformation" altitude.

Organizational reflex, not special project. In companies where the pattern works, AI use cases come from line operations rather than from a central lab, and procurement velocity for AI tools compresses from months to weeks. SIA passes both tests — line-VP-owned loops, the PALO IT decision compressing from a months-long discussion into a fast yes. The harder test, which SIA has not yet faced, is whether the agenda survives a CEO succession. Where the pattern stalls, AI lives inside an innovation team that the rest of the company can ignore.

Industry-specific timing. In companies where the pattern works, the company's DNA, its operating doctrine, and the inflection point in its industry are aligned. At SIA the alignment is unusually tight — operational excellence DNA, a make/buy doctrine that owns physical execution and rents intelligence, and an SAF mandate that raises the value of every kilogram of fuel saved. Where the pattern stalls, the AI investment program runs faster than the organization can absorb it.

References