Richemont

13

min read

On 23 April 2025, Richemont closed the sale of YOOX NET-A-PORTER to Mytheresa, accepting a 33% stake in the renamed LuxExperience and a roughly €1.0bn final loss from discontinued operations. The exit ended a fifteen-year experiment in operating a multibrand digital platform alongside its twenty-plus Maisons. What it left visible was a quieter pattern that had been there all along: a federated holding in which Cartier, Van Cleef & Arpels, IWC, Vacheron Constantin, Jaeger-LeCoultre and the rest each run their own commercial logic on top of shared scaffolding the group provides — Salesforce-and-Google-Cloud clienteling (the ELEVATE program, around 10,000 users in 45 markets), AWS for enterprise IT (about 5,000 virtual machines and 120 SAP instances migrated), an "Agent 42" internal LLM for roughly 45,000 employees, and the new R:Tech Lisbon hub targeting 400 technologists by 2028. AI is deliberately back-office, never customer-facing. By H1 FY26, the holding was generating €10.6bn in half-year revenue at a 22.2% operating margin with €6.5bn in net cash, Jewellery Maisons growing +14% at constant rates against a sector slowdown.

In a federated holding, value comes from clarifying which layers to share, which to leave to operating units, and which not to operate at all. The substrate is connective, not central; restraint is enforced where the brand contract demands it. The YNAP exit is what it cost Richemont to make the constitutional rule of its holding visible to itself.

The pattern, in its federated form

This is the substrate-first move, but in a form that is the structural inverse of the form most associated with the canonical case.

The question the pattern asks is what comes first, the substrate or the AI? The answer is the substrate, every time. AI workloads land on top of a unified data layer that already exists; if you reverse the sequence, the workloads land on data swamps and the algorithms reflect the swamp.

Richemont answers the same question — substrate first — but the substrate it builds is shaped differently. There are at least two recognizable forms a substrate-first answer can take. One form centralizes the substrate at the infrastructure layer and partitions the data inside it on a per-business-unit basis. The center owns the platform; the units share the rails but not the data. The other form, which is the one Richemont runs, distributes the substrate at the operating layer and shares only the connective scaffolding between units. Each Maison runs on its own commercial stack; the group provides a thin connective layer underneath — clienteling rails, cloud, identity and provenance, an internal LLM gateway. Both forms are substrate-first. The federated form keeps the substrate question intact while flipping the answer about where centralization happens.

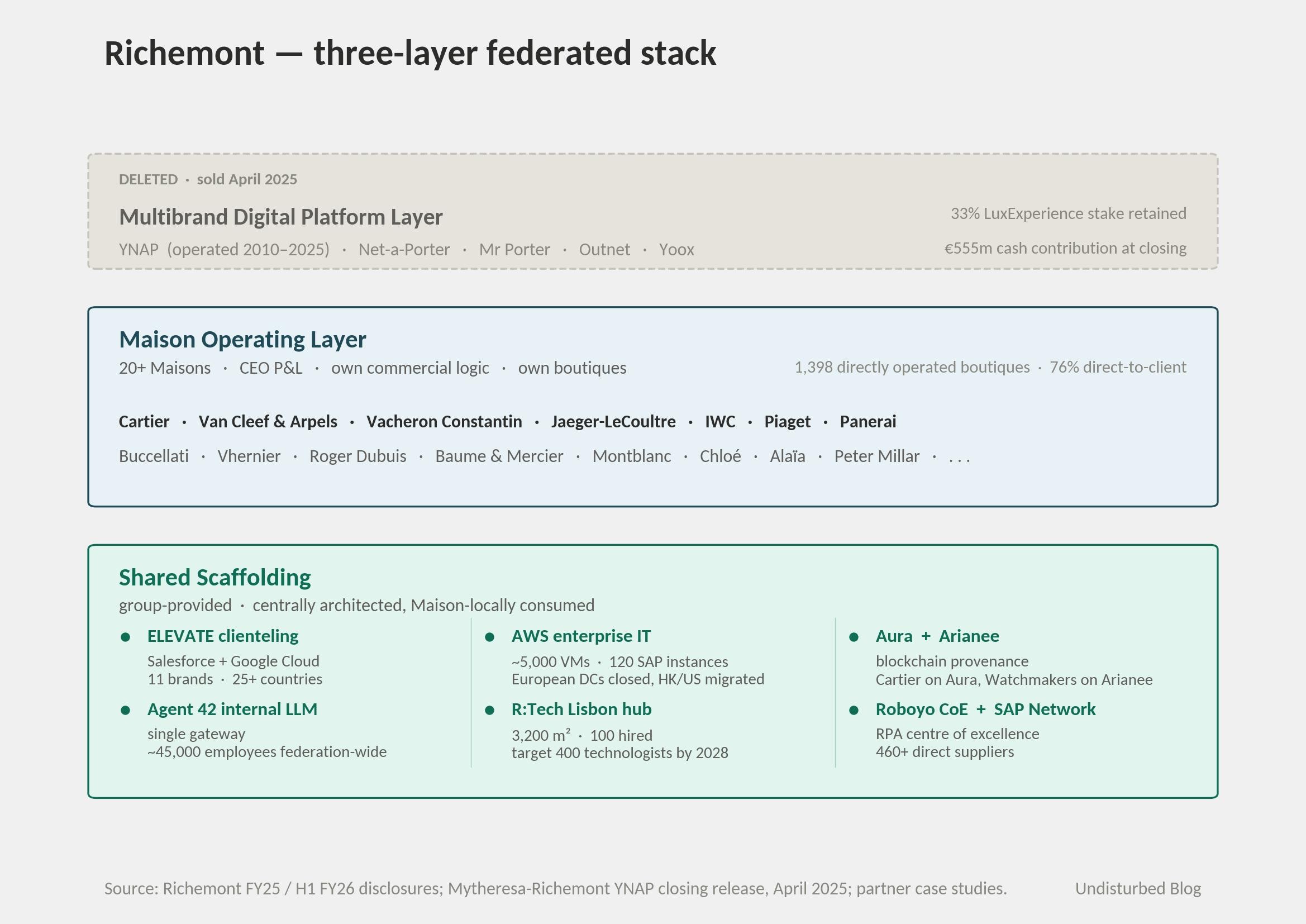

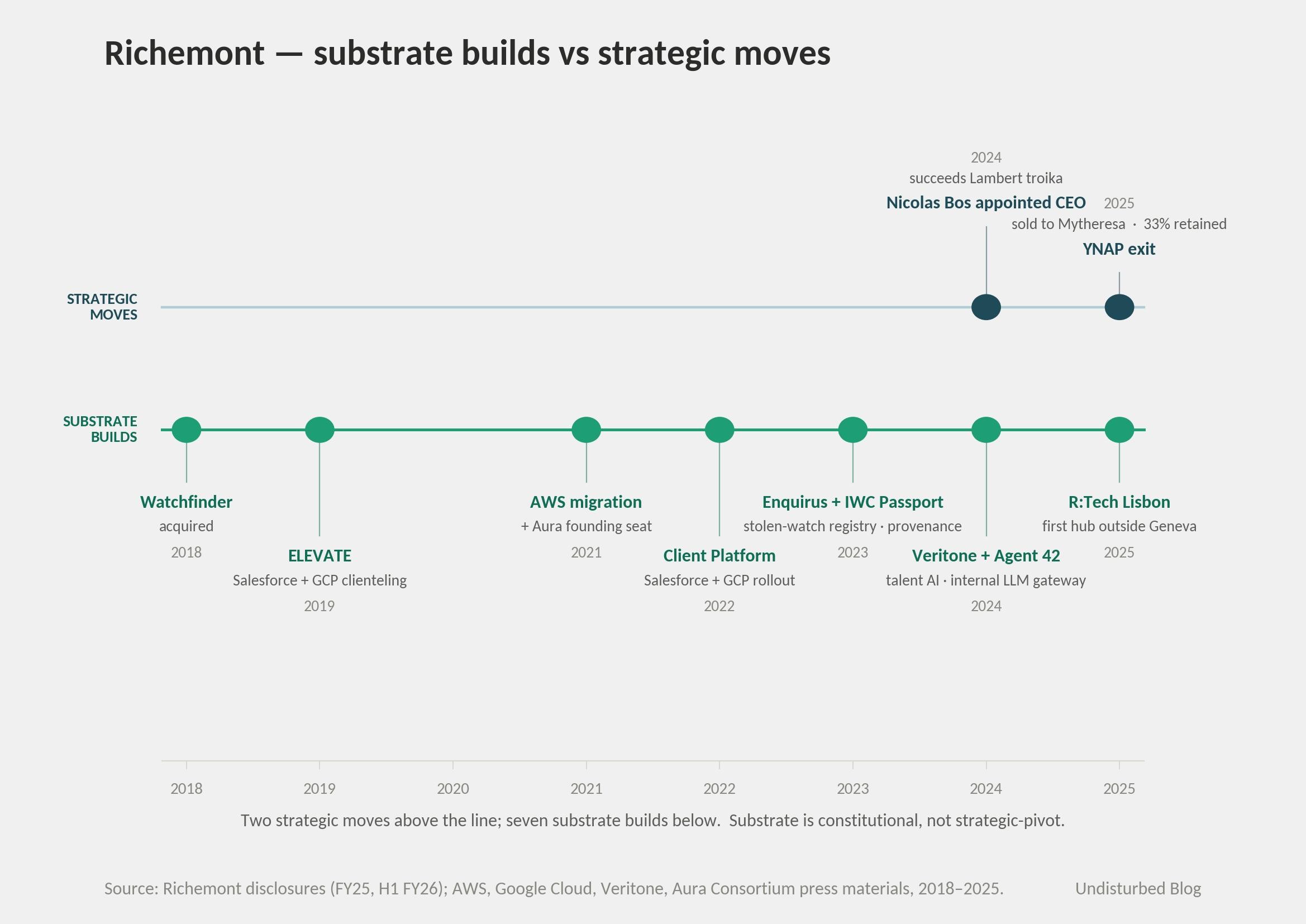

The federated form is harder to draw cleanly because it requires you to also draw what is not there. Richemont's stack has a deleted layer at the top — the multibrand digital platform layer it tried to operate from 2010 through 2025 (Net-a-Porter, then YNAP). That layer was the place a holding might centralize its commercial reach across Maisons. Richemont sold it. The deletion is not a failure footnote; it is the strategic move that completes the variant.

The federated form satisfies the substrate-first thesis on the timeline that matters: ELEVATE in 2019, the AWS migration in 2021, the Salesforce-and-Google-Cloud client platform in 2022, the Lisbon hub in 2025 all predate any disclosed customer-facing AI ambition. What changes from the textbook form is where the substrate sits. In the textbook case, beneath one organization. Here, beneath twenty-plus, and therefore necessarily thinner and more connective. The pattern still works, but the moat is the coherence of the connective scaffolding rather than the depth of any single substrate. Architecture transfers; the activation energy — the family-trust governance that lets a holding refuse vertical integration — does not.

The strategy in one picture

Three layers, top to bottom. Read the deleted layer first.

The reader's eye should land on the deletion first, then on the federation, then on the connective rails underneath. The diagram has two distinguishing features against the standard substrate picture: the operating layer is plural rather than singular, and the layer above it is explicitly absent.

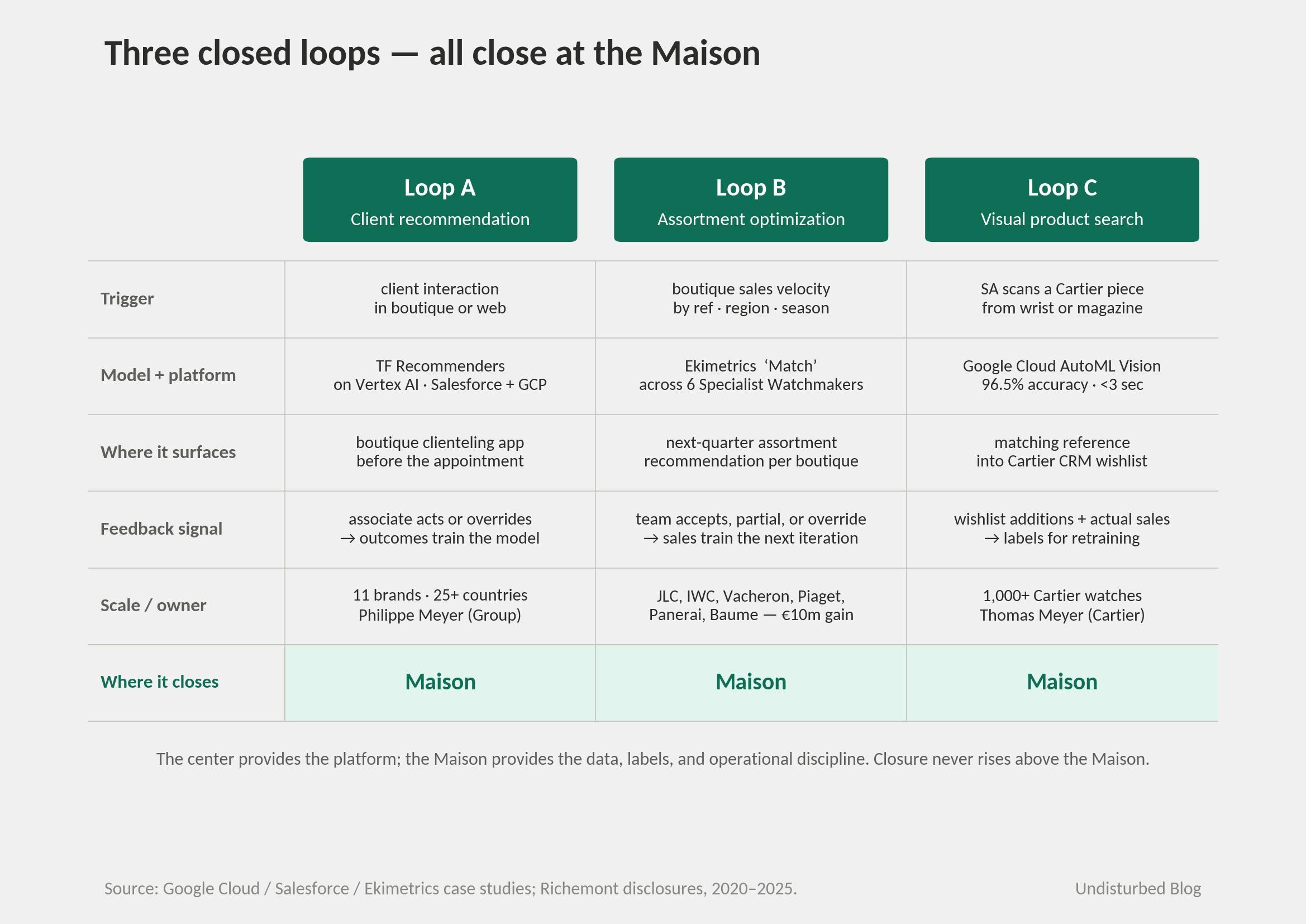

How it actually works — three closed loops

Three loops on the shared scaffolding, each with the property that a Maison's outputs feed back into the same substrate that produced its inputs. The loops are AI loops, not just data loops, because the closing involves model retraining at each turn.

Loop A — Client recommendation.

The ELEVATE program runs on Salesforce Marketing Cloud integrated with Google Cloud's BigQuery and Vertex AI. A client interaction in any Maison's boutique or website is captured to the Maison's slice of the unified client database. A propensity model — TensorFlow Recommenders running on Vertex AI — scores the client's likely next product and timing. The score surfaces in the boutique sales associate's clienteling app before the client arrives for a private appointment. The associate either acts on the recommendation or overrides it; both outcomes feed back into the model's training set. Group Client Marketing Director Philippe Meyer describes the operational core of ELEVATE as "one unified global database, one marketing automation platform, one measurement framework." Eleven brands use it across more than 25 countries.

Loop B — Assortment optimization in Specialist Watchmakers.

The Ekimetrics platform "Match" runs across Jaeger-LeCoultre, IWC, Vacheron Constantin, Piaget, Panerai, and Baume & Mercier — six of the eight Specialist Watchmakers. A boutique's sales velocity by reference, by region, by season feeds the model; the model recommends an assortment for the next quarter; the boutique team accepts, partially accepts, or overrides; the resulting sales feed the model's next iteration. JLC Business Development Manager Arthur Le Pan Faberes and IWC Assortment Manager Annabel Wunder are the named owners on the Maison side. Reported benefits include roughly +1 percentage point of productivity (around €10m gains across the group's watchmakers using the platform) and 50+ working days per month saved in assortment creation.

Loop C — Visual product search at Cartier.

A boutique sales associate sees a Cartier piece on a client's wrist or in a magazine clipping. The associate scans it through a mobile application built on Google Cloud's AutoML Vision; the model returns the matching reference from a catalog of more than a thousand Cartier watches in under three seconds with 96.5% accuracy. The match flows into the client's wishlist within the Cartier CRM. Wishlist additions and the actual sales that follow are the labels the model is retrained against. Cartier Data Officer Thomas Meyer described it as the path to making Google Cloud the core of a global data platform for Cartier — the language of substrate, not of feature.

What unifies the three loops is that none of them operate above the Maison layer. The center provides the platform, the model code, and the cloud bill. The Maison provides the data, the labels, and the operational discipline that decides whether the model's recommendation is acted on. Closure happens at the Maison level. The center never sees the client recommendation that ELEVATE serves to a specific Cartier client; the center only sees that ELEVATE is improving its precision month over month across the federation.

The numbers

Direct-to-client revenue: 76% of FY25 sales, generated through 2,400+ monobrand boutiques and Maison-direct online channels. By H1 FY26, 1,398 directly operated boutiques produced 70% of group sales. The federated form requires owned distribution because the Maison is the operating unit and only the Maison can run the brand contract.

Cloud and platform footprint: around 5,000 virtual machines and 120 SAP instances migrated to AWS by end-2022, with the closure of European data centers and the migration of Hong Kong and US data centers. ELEVATE deployment across 45 markets; Client Platform deployed across 11 brands in over 25 countries. Approximately 45,000 employees on the Agent 42 internal LLM gateway.

Technology talent: R:Tech Lisbon inaugurated July 2025, 3,200 m² in Parque das Nações; target of 400 technologists by 2028; 100 hired to date, 80% Portuguese; first international tech hub outside Geneva. Capgemini named as implementation partner.

Talent acquisition AI: Veritone three-year contract signed October 2024 for AI-powered job distribution across 2,000+ job boards in 180 countries, integrated with Workday. Pedro Guarita is the named program owner on the Richemont side.

Provenance: 50+ million luxury products registered to the Aura Blockchain Consortium as of August 2025 across 50+ luxury brands. Cartier holds Richemont's seat on Aura. The Specialist Watchmakers run a parallel track on Arianee, with Vacheron Constantin (since 2019, full rollout end-2021), IWC (My IWC Passport from October 2023), Roger Dubuis, and Panerai active.

YNAP exit: total ~€1.0bn final loss from discontinued operations in FY25 (refined from €1.3bn previously communicated). Richemont retains a 33% stake in LuxExperience and wired a €555m cash contribution to the company at closing.

The €1.0bn loss is the wrong number to anchor on. The right numbers are the retained 33% stake and the €555m cash contribution — together they say Richemont is not exiting the multibrand digital channel; it is exiting operating it. The financial exposure remains; the operating responsibility transfers to a focused operator. This is the cleanest expression of the doctrine — the holding wants the optionality of the layer above its Maisons but not the responsibility for it. The write-down is what it cost to learn that distinction. The number that compounds from here is the LuxExperience stake's mark-to-market over the next 24-36 months.

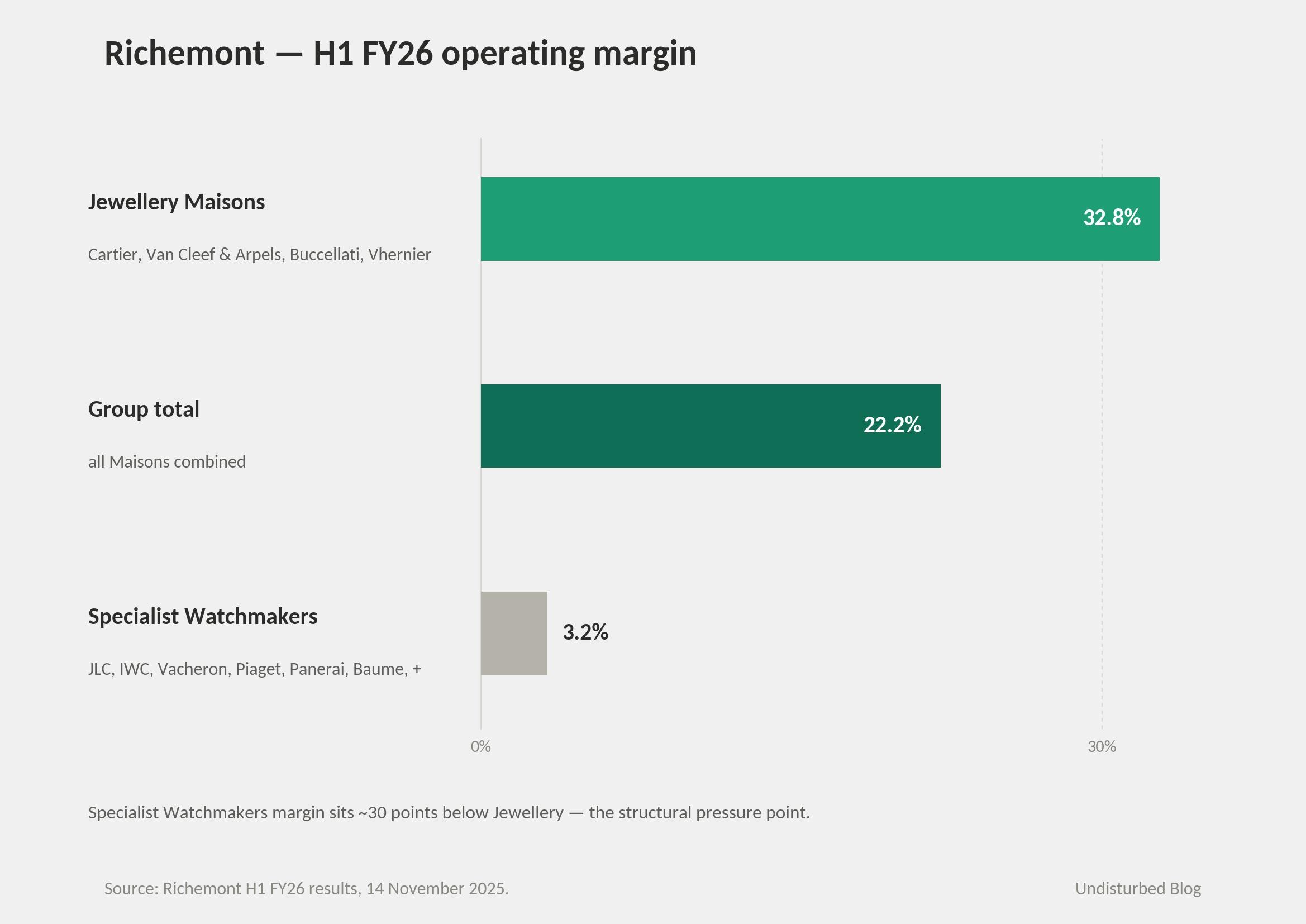

The financial counter-narrative is the holding's continuing-operations strength: FY25 revenue €21.4bn, operating profit €4.5bn, net cash €8.3bn; H1 FY26 revenue €10.6bn (+10% constant rates), operating profit €2.4bn at 22.2% margin, net cash €6.5bn; nine-month FY26 sales €17.0bn (+10% constant). Jewellery Maisons +14% at constant rates in H1 FY26 with a 32.8% operating margin; Specialist Watchmakers margin 3.2%, the structural pressure point.

What the holding has not disclosed is itself a number. There is no standalone IT, AI, or data spend line item; no headcount target for AI specifically; no quantum for a named AI program of the kind peers have begun to lead earnings narratives with. The 400-headcount R:Tech target is the most concrete public commitment, and it is "technology" not "AI." The absence follows the doctrine: AI sits below the disclosure line because it sits below the customer-facing brand line.

Is AI a norm inside Richemont?

The honest answer is that it is becoming a norm, but Richemont is unusually disciplined about not making the norm visible.

There is no Group Chief AI Officer. There is no Chief Data Officer at the Senior Executive Committee level. The closest analogs are Group CIO Kim Hartlev (since 2019), Group CTO Eduardo Grilo, Group Chief Transformation Officer Frank Vivier, and Group Chief Platforms Officer Renaud Litré. CEO Nicolas Bos, who succeeded the prior troika in June 2024, has not made AI the headline of any earnings narrative in his first six quarters; the FY25 results press release in May 2025 led with jewellery growth, distribution, and craftsmanship investment. The H1 FY26 release in November 2025 did the same.

What does exist, below the disclosure line, is operational diffusion. A Roboyo Center of Excellence governs RPA across the federation in a centralized yet flexible model — central enough to keep the architecture coherent, flexible enough to respect the Maisons' creative and commercial autonomy. The same posture extends to AI: ELEVATE is centrally architected, Maison-locally consumed; Agent 42 is a single LLM gateway available to ~45,000 employees across the federation; the FY25 Non-Financial Report mentions new guidelines on data and AI security and governance accompanied by mandatory eLearning. Cartier runs Aura; the Watchmakers run Arianee. Maisons choose. The center makes the choosing possible.

The succession test for normalization usually asks: would the doctrine survive if the CEO changed? In Richemont's case the test was already run. The June 2024 transition from Jérôme Lambert's COO-led arrangement to Nicolas Bos as singular CEO did not change ELEVATE, the AWS commitment, the Lisbon hub plan, or the Agent 42 rollout. The doctrine is structurally older than any individual leader because it lives inside the holding's constitution: 20-plus Maison CEOs with their own P&Ls, the group as central support and shared services. AI cannot become a customer-facing flagship inside that constitution because the customer-facing flagship is always the Maison's brand, and the brand contract is older than any AI capability.

The harder test in luxury is succession-of-aesthetic. Would the AI doctrine survive a generational creative-director turnover, the kind that already roiled peer holdings in 2024-2025? The architecture inside Richemont survives because it sits beneath the Maison commercial layer and never appears on a runway. A new creative director at Cartier or Van Cleef & Arpels would inherit ELEVATE, Aura, and the visual product search application without changing them; they affect the next collection and the boutique experience but not the data substrate that supports either. The willingness to be invisible to creative succession is what makes a luxury AI program a norm rather than an ornament.

Why this answer fits Richemont

Three pieces of multi-decade DNA pre-shape the answer.

First, the constitution of the holding. Richemont was assembled by Johann Rupert from the early 1990s as a federation of acquired Maisons rather than a brand-extension play. Each Maison kept its CEO, its workshop, its narrative; the holding never positioned itself as an operator of the Maisons' commercial logic. Cartier runs Cartier; the holding does not run Cartier. The shared services that grew up alongside this constitution — IT, finance, distribution, real estate, group HR — were always configured as central support, not central operation. The AI scaffolding that has accumulated since 2019 — ELEVATE in 2019, the AWS migration in 2021, the Salesforce-and-Google-Cloud client platform in 2022, the Lisbon hub in 2025 — sits in exactly that posture. It is constitutional, not strategic-pivot.

Second, the make-or-buy pattern across the past two decades. Richemont built specialty platforms when the operating layer demanded it (Watchfinder for pre-owned watches, acquired 2018; Enquirus for stolen-watch registry, launched 2023; the Aura founding seat 2021), and it bought platform technology when the technology was the buy (AWS, Google Cloud, Salesforce, Veritone, Ekimetrics). It did not try to build a horizontal platform layer from scratch — except for YNAP, which was acquired then re-acquired then exited. The make-or-buy pattern teaches that Richemont knows the difference between scaffolding that supports the Maisons and platforms that try to replace the Maisons in the customer relationship. The exit clarified the rule.

Third, the family-trust governance. Johann Rupert's controlling stake through Compagnie Financière Rupert and his lifetime tenure as Chairman buys the holding the patience to refuse public-market pressure for AI productivity announcements. The 2025 quarterly cycle in luxury demanded that holdings show their AI hand; Richemont chose silence. This requires governance that does not punish silence. Most public companies do not have it.

The transferable architecture is straightforward: build a thin connective scaffolding underneath autonomous operating units; resist vertical integration into platforms with operating logic incompatible with the units' core; treat AI as plumbing, not as flagship. A federated software conglomerate, a multi-vertical industrial holding, a hospital network — all could run it. The non-transferable activation energy is the constitutional commitment, written into the holding's structure two decades before AI was the question, that the center cannot operate the units. Without that pre-commitment, the architecture invites a CEO to centralize when the next downturn arrives. With it, the architecture survives leadership change. Architecture travels easily; the activation energy is what most companies cannot manufacture in time.

Where it goes next

The federation has three open questions over the next 24-36 months.

The most concrete is the Specialist Watchmakers margin pressure — 3.2% in H1 FY26, structurally squeezed by Asia-Pacific weakness and the secondary-market overhang. The shared scaffolding (ELEVATE, Match, Aura/Arianee, Watchfinder + Enquirus together) is the holding's bet that substrate-led demand intelligence can lift assortment precision and pricing discipline faster than the cyclical pressure compounds. If the Watchmakers margin recovers through FY26-27 with ELEVATE and Match disclosed as contributing levers, the variant earns a stronger validation than the YNAP exit alone provided.

The second is the provenance-stack maturation. The dual track of Cartier-on-Aura and Watchmakers-on-Arianee will likely converge under EU Digital Product Passport regulation expected to phase in from 2026-27. Either Aura subsumes Arianee, or the holding maintains the dual track as a feature of Maison choice. The first outcome is more efficient; the second is more constitutional. The federated doctrine predicts the second.

The third is the LuxExperience stake's eventual disposition. The 33% holding is a financial bet that Mytheresa-with-YNAP can return to profitability under focused operating leadership. If LuxExperience executes through 2027, Richemont harvests a quiet capital return. If not, the holding absorbs another mark-to-market and the lesson about not operating multibrand digital platforms gets re-paid. Either way the operating doctrine does not change.

A fourth question, less immediate, is whether agentic AI distribution surfaces — the kind that have begun to reorder consumer-facing commerce in adjacent industries — eventually pull luxury into a stance Richemont has so far declined. The federation's response would not be a customer-facing chatbot; it would be a slow, Maison-by-Maison API exposure of catalog and provenance to whichever distribution surface gains durable consumer adoption, with the brand contract preserved in each integration. The architecture supports that trajectory; the question is the timing.

Four diagnostic frames

Richemont's answer resolves into four frames a reader can carry into a different holding.

The first is substrate location. The diagnostic question is where the substrate sits — centralized at the infrastructure layer, distributed at the operating layer, or partially built in both places without a clear answer. Holdings that have not resolved the question land their AI workloads on contested ground regardless of how well the workloads themselves are designed.

The second is the metric that compounds. Most disclosed AI numbers are vanity metrics. The number that matters is usually the one nobody asks about on the call: a margin point that quietly held when the cycle turned, a working-day count that fell when the assortment improved, a recommendation acceptance rate that crept up across the federation. Holdings whose AI is real have such a number even if they do not name it.

The third is visibility posture. Whether AI is configured as a customer-facing flagship or as a shared-scaffolding layer determines what kind of brand contract the architecture must respect. A flagship configuration requires brand permission to be visible; a scaffolding configuration requires the discipline to compound across operating units while staying invisible to them. Richemont's variant is the second.

The fourth is constitutional fit. The doctrine that fits is usually the one a holding's multi-decade DNA already implies. The doctrine that betrays is usually the one the market is loudest about right now. Holdings that copy a peer's AI doctrine without first reading their own constitution import the architecture but not the activation energy that makes it survive a leadership change. Architecture without activation energy reverts under pressure.

References