AXA

13

min read

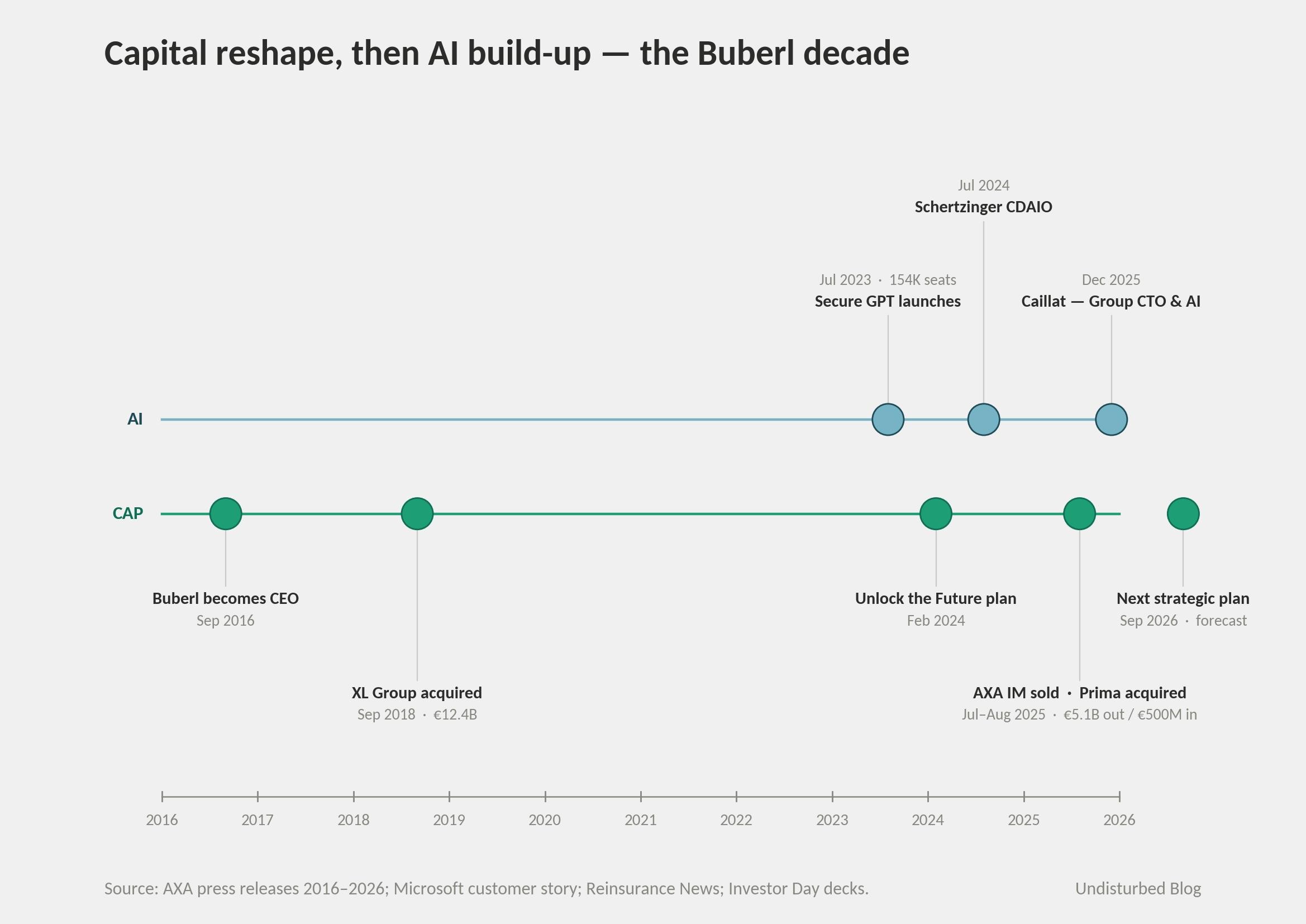

Between 2024 and 2026, AXA executed a sequence that read like four separate transactions and was in fact one architectural move. The group sold its asset manager AXA IM to BNP Paribas for €5.1 billion, bought 51% of the Italian direct insurer Prima for €500 million, scaled an in-house LLM platform to 154,000 employees, ran roughly 400 AI use cases in production across more than sixty countries, and — on December 1, 2025 — invented a new C-suite seat (Group Chief Technology & AI Officer) reporting into a combined Finance, Underwriting, Risk and Technology super-portfolio. The combined ratio moved from 91.0% to 90.6%. The publicly disclosed AI productivity target is roughly 10% over three years.

The conventional reading of this sequence is "AXA is investing heavily in AI." The structural reading is different. AXA is the case study for what happens when a company runs in more than sixty regulated jurisdictions and concludes that the answer to unify the data substrate is no. The answer is to keep the substrate federated, separate four layers by clock speed — capital, data, intelligence, interface — and propagate AI through a thin shared layer plus a lead-entity model. The strategy is the separation, not the unification.

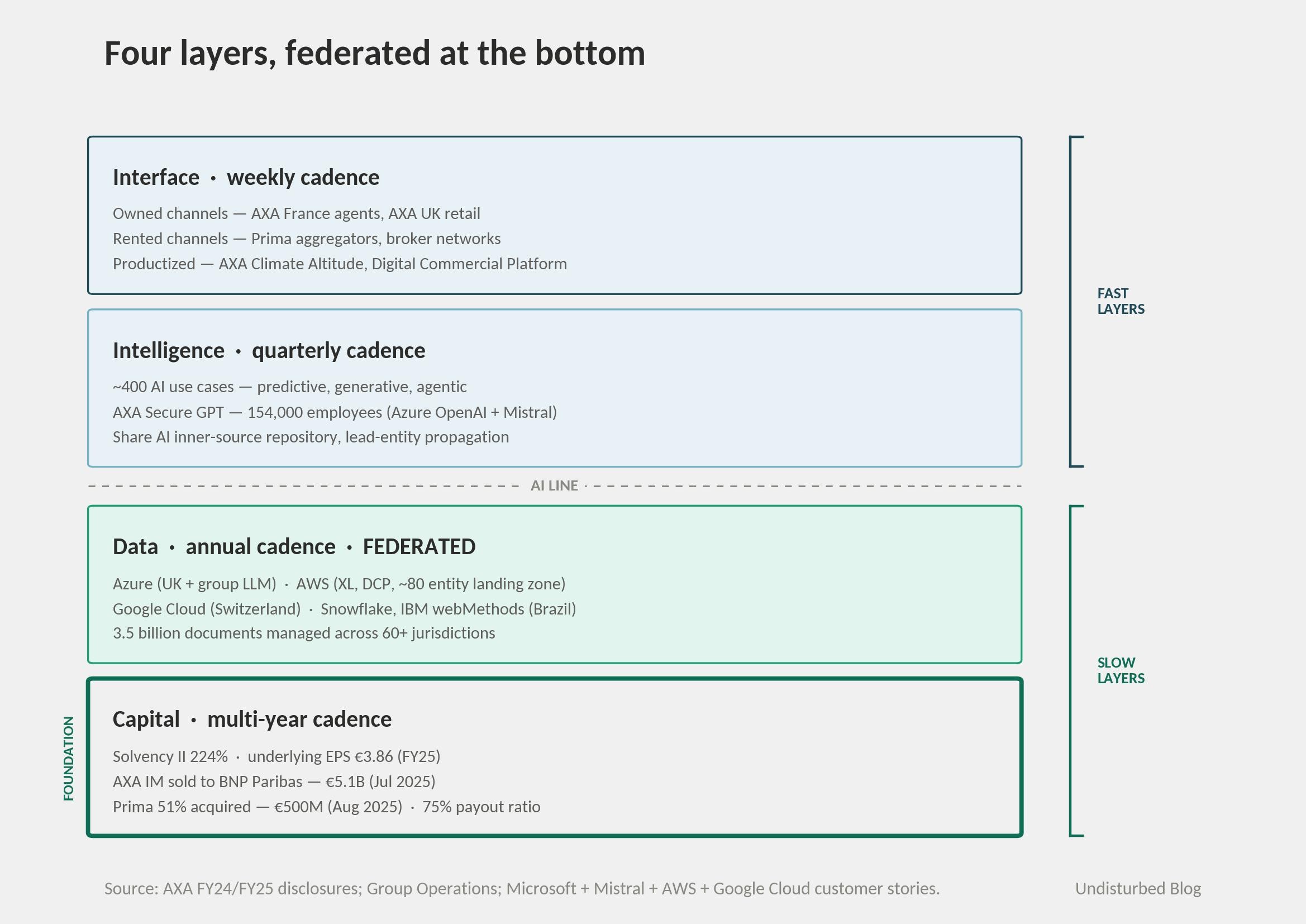

The Four-Layer Pattern, Federated

A useful way to read large companies in 2026 is to separate them into four operating layers that run on different clocks. The physical and data layers move slowly. The intelligence and interface layers move quickly. The horizontal line between the slow layers and the fast layers is the AI line, and the strategic question is how those layers connect.

FedEx is the canonical case — planes and hubs underneath, AI and customer interfaces above, a single data substrate (Dataworks) running the connection. JPMorgan is the asset-light financial-services variant of the same pattern — capital where FedEx has planes, the Athena platform where FedEx has Dataworks. Both companies have a single data substrate underneath the AI line. Athena is one platform. Dataworks is one platform.

AXA is the variant where the data substrate refuses to be one platform.

This is not a failure to integrate. It is the structural reality of insurance. AXA operates in more than sixty countries. France, Germany, Switzerland, the UK, Italy, Spain, Belgium, Japan, Hong Kong, Mexico, Saudi Arabia — each has its own solvency regulator, its own data residency rules, its own consumer protection law, its own claim adjudication culture. The Kingdom of Saudi Arabia restricts cross-border data flows. The EU has GDPR plus the AI Act. Switzerland is not in the EU but acts like it. None of this transfers cleanly onto a single substrate.

So AXA built something else. A federated substrate — Azure for the UK and the group LLM, AWS for AXA XL and the Digital Commercial Platform, Google Cloud for Switzerland, Snowflake on top in places, IBM webMethods middleware in Brazil. A thin shared coordination layer in AXA Group Operations, the shared services GIE that runs Secure GPT. And an inner-sourcing repository called "Share AI" where one entity's solution gets adapted by the next.

Four-layer separation, but the bottom layer is not one cloud. It is sixty.

It is tempting to read AXA's multi-cloud, multi-vendor stack as a backlog of unfinished integration. That reading misses what regulation forces. In an industry where a single solvency calculation has to satisfy a French regulator, a German regulator and a Hong Kong regulator simultaneously, putting all the data on one substrate is not just hard — it can be illegal. The right comparison for AXA is not JPMorgan's Athena. It is the federated computing pattern academic researchers describe for multi-jurisdictional finance: many substrates, one coordination layer, propagation through use cases rather than centralization through schema.

The Strategy in One Diagram

AXA itself does not draw it this way. Group Operations talks about "harmonization," not separation. But read the FY25 disclosures and the December 2025 leadership reshuffle together and the four layers are visible. The capital layer moves on three-year strategic plan cycles. The data layer moves with annual cloud-migration roadmaps. The intelligence layer ships use cases quarterly. The interface layer iterates weekly — agents adopt new tools, the Prima aggregator changes pricing in seconds.

The horizontal line between intelligence and data is the AI line. Above it: Secure GPT, Share AI, the roughly 400 use cases. Below: the federated substrate that feeds them and the capital structure that funds them.

How It Actually Works — Three Closed Loops

Loop 1: Underwriter RAG and the post-XL document moat

AXA manages 3.5 billion documents globally. After the 2018 XL Group acquisition (€12.4 billion), AXA became the world's number-one commercial P&C insurer, which means decades of niche-line loss data sitting in PDFs, broker emails, claim notes and engineering reports.

In AXA UK & Ireland, a single query to the underwriting guides used to take about 10 minutes. With RAG running on the proprietary corpus, that dropped to under 3 minutes. 86% of users rate the tool 8/10 or better, per Cali Wood, who runs Data and AI Strategy and Culture for UK & I. The system reads from AXA's documents, surfaces an answer, and the underwriter accepts or rejects it. Each accepted answer becomes a new datapoint about which retrieved chunks were actually useful, which goes back into ranking.

Algorithm reads from substrate. Substrate writes back from algorithm. The reason this works at AXA and not at a startup is that no startup has 3.5 billion underwriting documents.

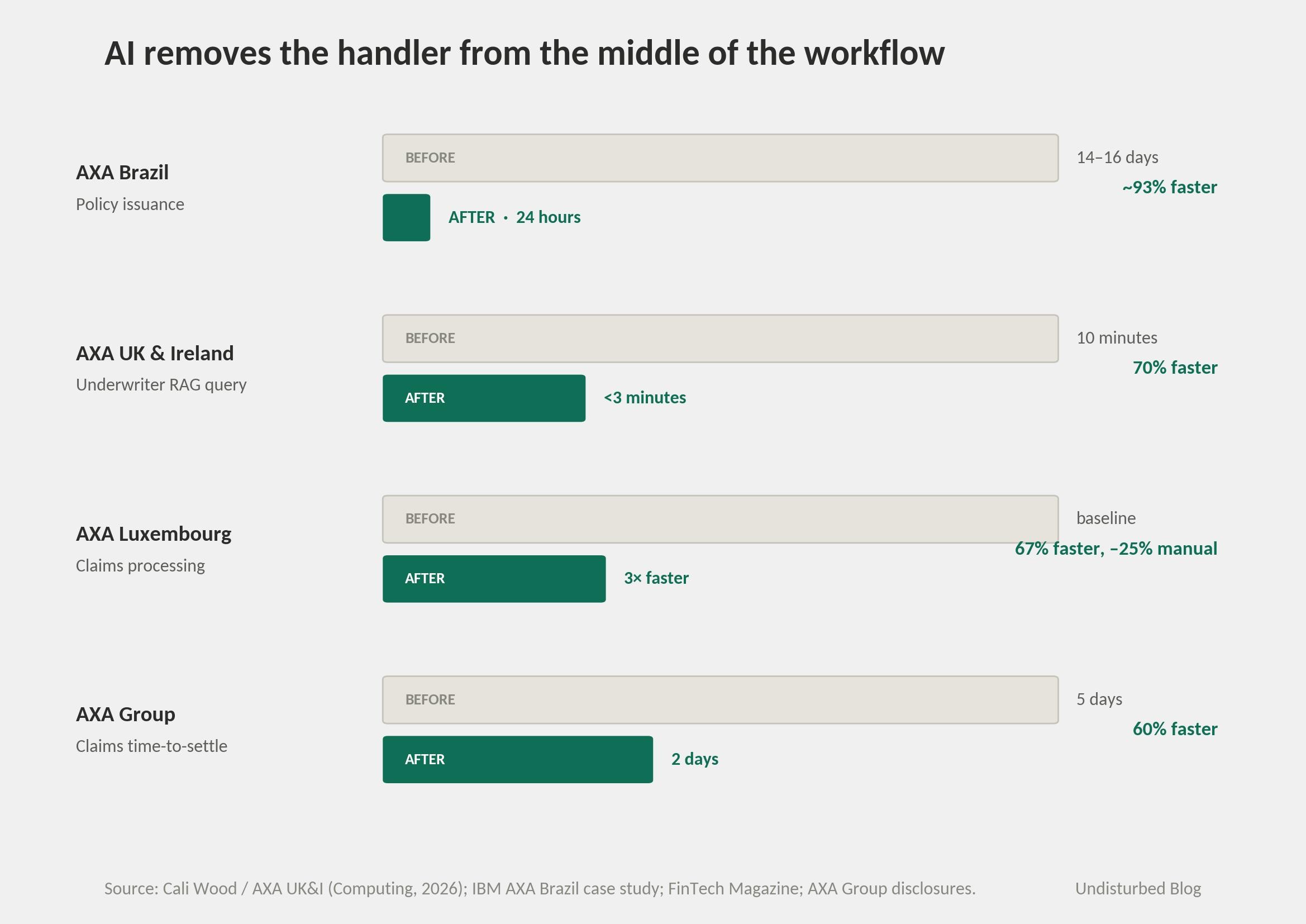

Loop 2: Claims time-to-settle, with humans in retreat from the middle

AXA Luxembourg cut claims processing 3x with a Born Digital and MuleSoft stack; manual work dropped 25%. AXA Brazil moved policy issuance from 14-16 days to 24 hours using AI plus RPA on top of IBM webMethods middleware. AXA Switzerland turned complex actuarial queries from "a whole weekend" into seconds on Google Cloud BigQuery. The group-level claims pipeline reports time-to-settle improvement from 5 days to 2 days, with instant payment in some lines.

In every one of these, AI does not replace the claims handler — it removes the handler from the middle of the workflow. The handler sets exceptions and reviews edge cases. The closed loop runs without them.

Loop 3: Wildfire risk and the prevention flywheel

In January 2025, wildfires destroyed thousands of structures in Los Angeles. AXA's Digital Commercial Platform — launched in 2022 under Pierre du Rostu — runs a tool called Wildfire AI that combines satellite imagery, AI and geospatial analytics to give up to 48 hours of advance warning. AXA used it during the LA fires not just to pay claims but to prevent them at insured commercial sites.

The flywheel: DCP collects loss prevention data from commercial clients, feeds it into AXA's underwriting models, prices accordingly, and pushes prevention services back to clients. Du Rostu's line is direct: "The best loss is the loss that does not happen." Reduce a motor portfolio's claims by 30% through prevention services, and the ratio improves without needing to raise prices.

The same logic runs at AXA Climate, founded in 2019, where 250 employees sell parametric insurance, training, consulting and the Altitude SaaS platform — which lets non-AXA customers run climate risk assessments at 30-meter resolution. Underwriting intelligence flowing outbound.

The Numbers

Metric | FY23 | FY24 | FY25 |

|---|---|---|---|

Gross revenues | €102.7B | €110.3B | €116B |

Underlying earnings | €7.6B | €8.1B | €8.4B |

Underlying EPS | €3.31 | €3.59 | €3.86 |

Combined ratio (P&C) | 91.0% | 90.6% | 90.6% |

Solvency II | 227% | 216% | 224% |

Net income | €7.2B | €7.9B | €9.8B |

AI-specific figures, from group disclosures and from Andreas Schertzinger (Group Chief Data, AI & Innovation Officer since July 2024):

~400 AI use cases in production across predictive, generative and agentic

~20 use cases scaled globally as "lead entity" solutions

60+ agentic use cases in testing or partial deployment

154,000 employees with access to AXA Secure GPT (launched July 27, 2023, built on Azure OpenAI in three months)

900+ data scientists and data engineers recruited in recent months (Guillaume Borie, FY25 call)

100+ department-specific prompts in the Secure GPT prompt library

~50% engagement rate in the AXA Data & AI Academy among in-scope UK & I employees

The AXA–Shift Technology partnership runs across 15 countries — fraud, claims, underwriting — renewed for five years on March 5, 2026, and Shift won AXA's Delivering @ Scale Supplier Award in 2025.

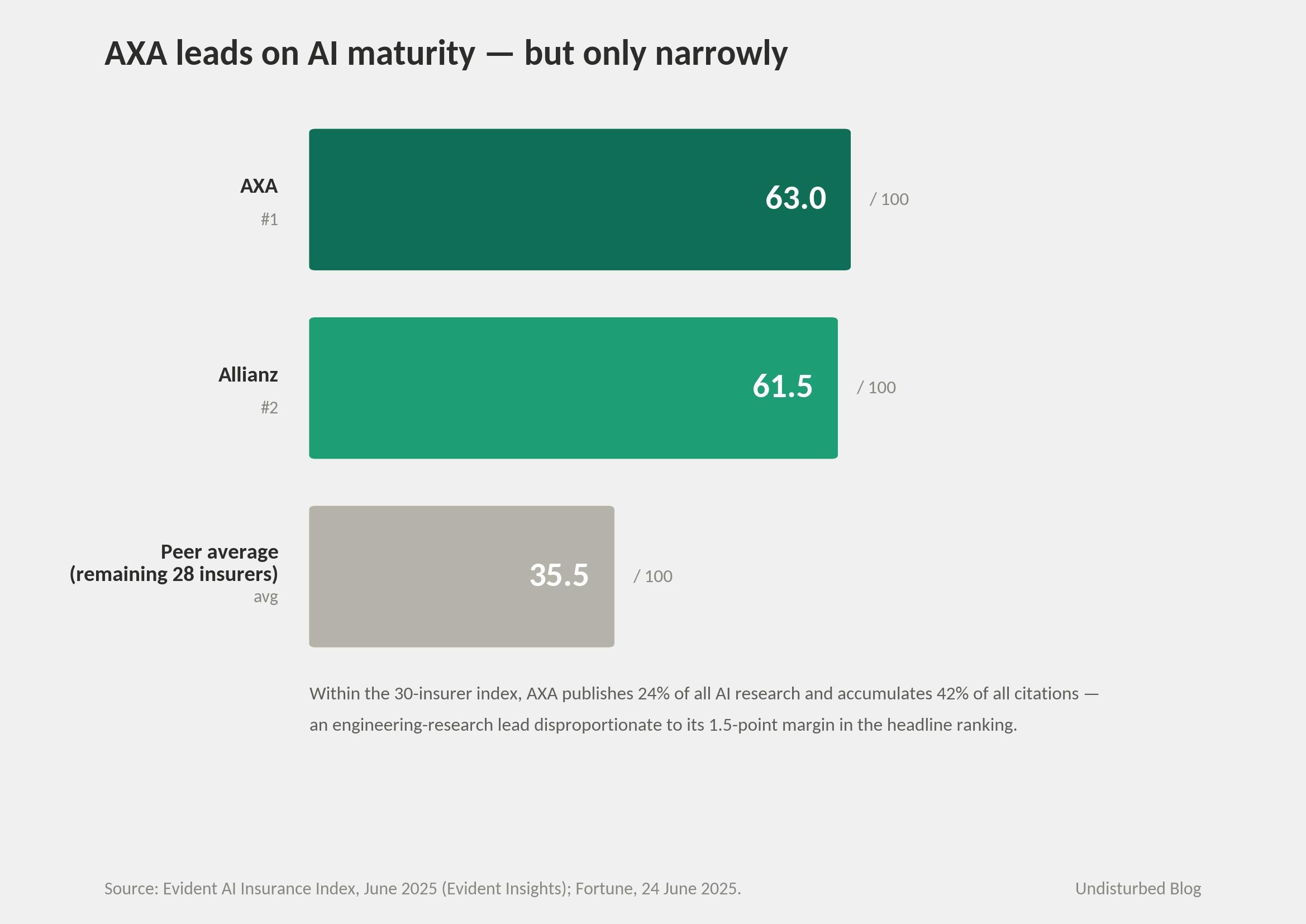

In June 2025, the Evident AI Insurance Index ranked AXA first out of thirty top global insurers at 63/100, edging Allianz at 61.5, with the peer average at 35.5. AXA produces 24% of all AI research publications among the thirty insurers and 42% of all citations. Evident co-CEO Alexandra Mousavizadeh told Fortune the lead comes from "an engineering culture. Axa and Allianz have been doing this for a very long time."

The strange disclosure here is the 10% productivity target. AXA leads on every AI maturity benchmark, though the gap with Allianz is narrow. So why does the Unlock the Future 2024–2026 strategic plan commit to only roughly 10% productivity gains over three years? Two readings are available. The first: AXA is sandbagging, and the real number is higher. The second: AXA's AI is genuinely defensive — a moat against insurtech challengers and a cost floor against margin compression, not an offensive cost weapon like Intact Financial's disclosed $150M annualized AI ROI. The combined-ratio path (91.0% → 90.6% → 90.6%) supports the second reading. AI here is keeping the business insurable, not transforming it. That distinction matters when reading what AXA actually believes about AI.

Is AI a Norm Inside AXA?

The 154,000-employee Secure GPT rollout is the surface number. The deeper test is whether AI is a norm — embedded in how decisions get made, not a department initiative.

A few markers. The AXA Data & AI Academy is a formal training institution built on four pillars: capability, literacy, collaboration, talent strategy. Around 50% of AXA UK & Ireland's in-scope ~8,000 employees engaged with it. AXA partners with Stanford HAI, Sorbonne and EPFL Lausanne on research. AXA built and published the Fairness Compass, a decision-tree tool for selecting fairness measures in AI systems.

The Group Emerging Technologies & Data team inside AXA Group Operations does not dictate stacks — it "co-creates" with entities. That phrasing matters. The norm AXA is building is not "use the central platform." It is "find a use case, adapt one from Share AI, propagate to other entities."

The October 2025 leadership announcement makes this explicit. Frédéric Caillat is appointed Group Chief Technology & AI Officer with the mandate to "drive the Group's technology and AI transformation with the required speed and focus." Guillaume Borie, his superior, runs the combined Finance, Underwriting, Risk and Technology super-portfolio. Schertzinger, already in place, becomes the senior AI-specific operator inside Caillat's org.

70% of AXA employees, per the internal barometer Buberl referenced on the FY25 call, "are optimistic when it comes to the future benefits coming from AI." That is a culture marker, not a deployment metric.

The harder test of normalization is succession. Thomas Buberl has been Group CEO since September 2016 and will eventually leave. The question for AXA's AI strategy is not whether Buberl believes in it — clearly he does — but whether the architecture survives a CEO who doesn't. The December 2025 reshuffle answers this. By creating a permanent Group CTO & AI Officer seat and routing it through a Finance super-role rather than a peripheral innovation office, AXA has structurally embedded AI in the org chart. A future CEO who wanted to deprioritize AI would have to physically dismantle a C-suite seat. That is what normalization looks like — not the use case count, but the irreversibility of the org chart.

Why This Answer Fits AXA

AXA was built by acquisition. Claude Bébéar started from a mutual in Normandy in 1985 and built AXA through Equitable, GRE, Winterthur, XL, Laya, GACM España, Prima. Each acquisition came with its own systems, its own regulators, its own loss data, its own broker relationships.

The architecture problem AXA inherited is not "we never built one substrate." It is "we built sixty substrates, each tied to a local license, and we are not allowed to throw them away." Four-layer separation with a federated bottom layer is the only structure that fits this history.

Buberl's "Unlock the Future" sequence — sell AXA IM for €5.1B (closed July 2025), buy Prima for €500M (August 2025), reshuffle the C-suite (December 2025) — is the capital-layer move that makes the intelligence-layer move possible. AXA is now roughly 85% insurance versus 15% financial-market-sensitive, compared to roughly the inverse in 2008. Buberl told markets this was "one of the last steps" in reshaping the portfolio. The capital is being concentrated on the layers where AI compounds: P&C loss data (XL), health underwriting data (Laya), motor pricing data (Prima).

Prima is the interesting one. AXA did not buy a French insurtech — it bought an Italian aggregator-native direct insurer with 5 million customers, a 90% combined ratio, and 400+ software engineers and data scientists on a 1,100-person headcount. AXA bought a digital-native pricing and distribution stack. The architecture says: leave Prima's substrate alone, plug it into Share AI, let it become a lead entity for direct distribution patterns the rest of AXA can adopt.

This is the move other insurers can read, but most cannot copy. Allianz could in theory. Generali could in theory. Zurich could in theory. The architecture transfers — four-layer separation, federated substrate, thin shared coordination, lead-entity propagation. What does not transfer is the activation energy. AXA spent 2016–2024 reshaping the portfolio: divesting AXA Equitable, selling AXA IM, integrating XL, killing minor business lines, and earning the right to spend on AI from a position of capital strength. Most insurers are still in the "what do we sell first" phase.

The four-layer separation is a diagram. Any large insurer can draw it. The diagram tells nothing about whether the company can act on it. AXA could act because by the time the LLMs landed, Buberl had already manufactured €5.1 billion of free cash by selling the asset manager — a decision he announced in August 2024, before AI was the explanation for anything. Most insurance CEOs do not have €5.1B of decisions like that already executed. They will read about this architecture, sketch the four layers, and discover that they have the diagram without the cash. The willingness to sell a profitable business to fund a structural bet is the hard part. The diagram is the easy part.

Where It Goes Next

The 2027–2029 strategic plan unveils in September 2026. Three things to watch.

First, whether AXA discloses a hard AI ROI number. Intact Financial put $150M annualized on the board. Zurich has hinted at numbers under its $2B AI investment plan through 2026. AXA has not. If the September 2026 plan includes an AI-attributable cost-savings or revenue figure, the pattern thesis shifts — AI moves from defensive moat to offensive weapon. If it doesn't, AXA remains the company that is best at AI without using it to publicly underwrite a number.

Second, what happens to Prima. The put/call on the remaining 49% triggers in 2029–2030. If Prima's stack becomes AXA's default direct-distribution platform across multiple geographies, the substrate consolidation thesis becomes live for the first time. Federation by national entity could give way to platform-led pricing engines deployed across countries.

Third, agentic AI. Caillat and Schertzinger both flag agentic deployment as the next-clock acceleration — 60+ use cases in test today, scaled across contact centers, underwriting, claims. Agentic systems break the "human in the middle" pattern in a way RAG and classifier models do not. If the next plan commits to agentic-first claims handling at scale, the intelligence layer starts moving on a monthly cadence and the clock-speed mismatch with the data layer grows. That is the four-layer pattern intensifying, not weakening.

The harder version of that bet: agentic AI may not respect federation. Agents that orchestrate across underwriting, claims and pricing want a unified context. A federated substrate that worked beautifully for predictive and generative AI may become a tax in an agentic architecture — sixty contexts to stitch together when one would do. AXA's pattern protects regulatory reality. It does not automatically protect against the next paradigm.

The pattern only works if the layers stay separated. The risk is not federation. The risk is the temptation, once 400 use cases compound, to declare victory and try to force a single substrate from the top. Buberl has so far resisted. The next CEO might not.

Four Diagnostic Markers

AXA's structure suggests four diagnostic markers worth applying to any large company claiming a serious AI strategy.

Is federation accidental or intentional? Most large companies with multi-country operations have a federated data layer. AXA's distinguishing move is to admit it, name it and build a thin coordination layer on top instead of forcing centralization. The diagnostic: when federation exists, is it being solved as a problem, or used as architecture?

Does breadth back the headline? AXA has roughly 400 use cases, 154,000 Secure GPT seats and 86% user satisfaction on underwriter RAG. None of those is a single ROI number, but together they show breadth. The diagnostic: a single impressive headline number with nothing under it tends to be a demo. A hundred small numbers with no headline tends to be real but unscaled. The shape that compounds is breadth plus disclosed friction.

Is AI in the org chart, or in an innovation office? AXA created a C-suite seat (Group CTO & AI Officer) under a Finance super-role. A future CEO who wanted to deprioritize AI would have to dismantle that seat. The diagnostic: where AI sits in the org chart predicts what happens at the next CEO transition. Innovation-office AI is reversible. C-suite AI under a core business function is not.

Has the capital layer earned the right? Buberl spent 2016–2024 reshaping AXA's portfolio specifically to free up capital and attention for AI. The €5.1 billion AXA IM sale wasn't an AI move on paper. It was the capital-layer move that made the intelligence-layer move possible. The diagnostic: AI programs funded by genuine portfolio reshaping behave differently from AI programs funded by hoping the existing business produces enough cash flow to spare.

References