Munich Re

14

min read

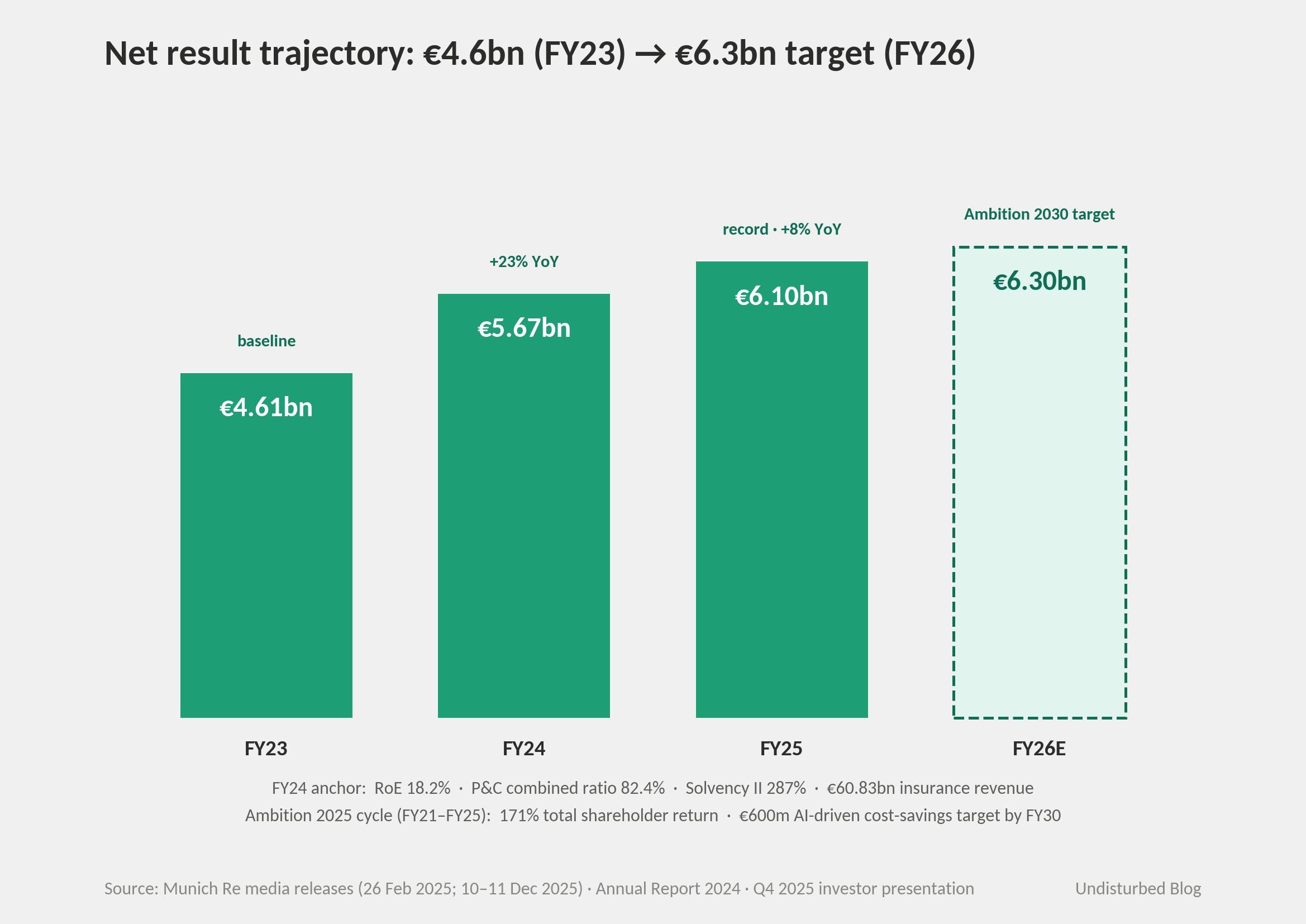

A 145-year-old German reinsurer, founded in 1880 to write what others could not, began writing insurance on AI models themselves in 2018 — six years before "AI risk" became a board-level phrase. In 2024, CEO Joachim Wenning told shareholders the Group had "identified, launched or already implemented over 300 AI use cases." Insurance revenue reached €60.8bn, net income €5.7bn, the Solvency II ratio 287%. The Ambition 2030 strategy unveiled in December 2025 names a €600m AI-driven cost target and — separately — confirms ERGO will shed roughly 1,000 jobs by 2030 as AI absorbs them. Munich Re is a founding partner in Google Cloud's Risk Protection Program. In August 2025, for the first time in its history, the company created a Chief Technology Officer seat at Board level.

AI doesn't run on substrate. AI is substrate-dependent — and the substrate it most lacks is not compute, not data, not regulation. It is the right to fail in regulated industries without ruining the company that deployed it. Munich Re has spent 145 years building exactly that substrate for fire, earthquakes, satellites, cyber, and now models. The product the market eventually pays for is not the algorithm or the data — it is the balance sheet × actuarial trust × regulator standing that makes AI deployment underwritable. Call it fiduciary sovereignty.

The pattern

Munich Re is one instance of a broader strategy pattern: operational substrate as sovereign product. A company spends decades or centuries building infrastructure that, in its original framing, was simply the cost of being in business — and then, when external demand for that infrastructure crystallizes, the substrate gets productized while the original business continues as captive anchor demand. The pattern wins because jurisdictional or regulatory constraints make the substrate non-substitutable, and the internal anchor funds the build long before any external customer appears.

A useful parallel sits in retail. Schwarz Gruppe, the German owner of Lidl and Kaufland, built STACKIT — a cloud productizing EU data residency — on top of the data infrastructure it had to run for its own stores. The substrate is hard to substitute because hyperscalers cannot credibly offer it; the anchor demand was already in the building. Schwarz Gruppe productizes data sovereignty: where can this dataset legally live? Munich Re productizes fiduciary sovereignty: whose balance sheet can legally carry this risk? Both forms of sovereignty are jurisdictionally constrained. Both require an anchor that pre-dates the productization. Both compete with hyperscalers and Wall Street capital that should, on paper, be able to muscle in. Neither has been displaced.

The honest counter-reading is that Munich Re looks like a data company — NatCatSERVICE has collected catastrophe loss records since 1974 — or a software company — REALYTIX ZERO, alitheia, and CatAI are productized algorithms sold to other insurers. The right test is the same one used for Schwarz Gruppe: what would this company sell if you stripped away the substrate? For Schwarz Gruppe minus EU data residency, STACKIT is just another mid-tier cloud. For Munich Re minus its AA-rated balance sheet and 145 years of regulator trust, NatCatSERVICE is a dataset, REALYTIX is a SaaS, aiSure is a press release. The data and the algorithms are inputs that price the substrate. The substrate is what gets sold.

A pure-play loss-data company like RMS or Verisk doesn't capture the same rent Munich Re does, because it doesn't carry the risk. A pure-play AI-underwriting SaaS like Sixfold or Armilla doesn't either — it relies on someone else's balance sheet to pay claims. What Munich Re uniquely sells is the right to transfer risk onto a regulator-trusted, AA-rated, jurisdiction-bound balance sheet. The 51-year NatCatSERVICE record and the 7-year aiSure loss book are pricing inputs to that sovereign-substrate product.

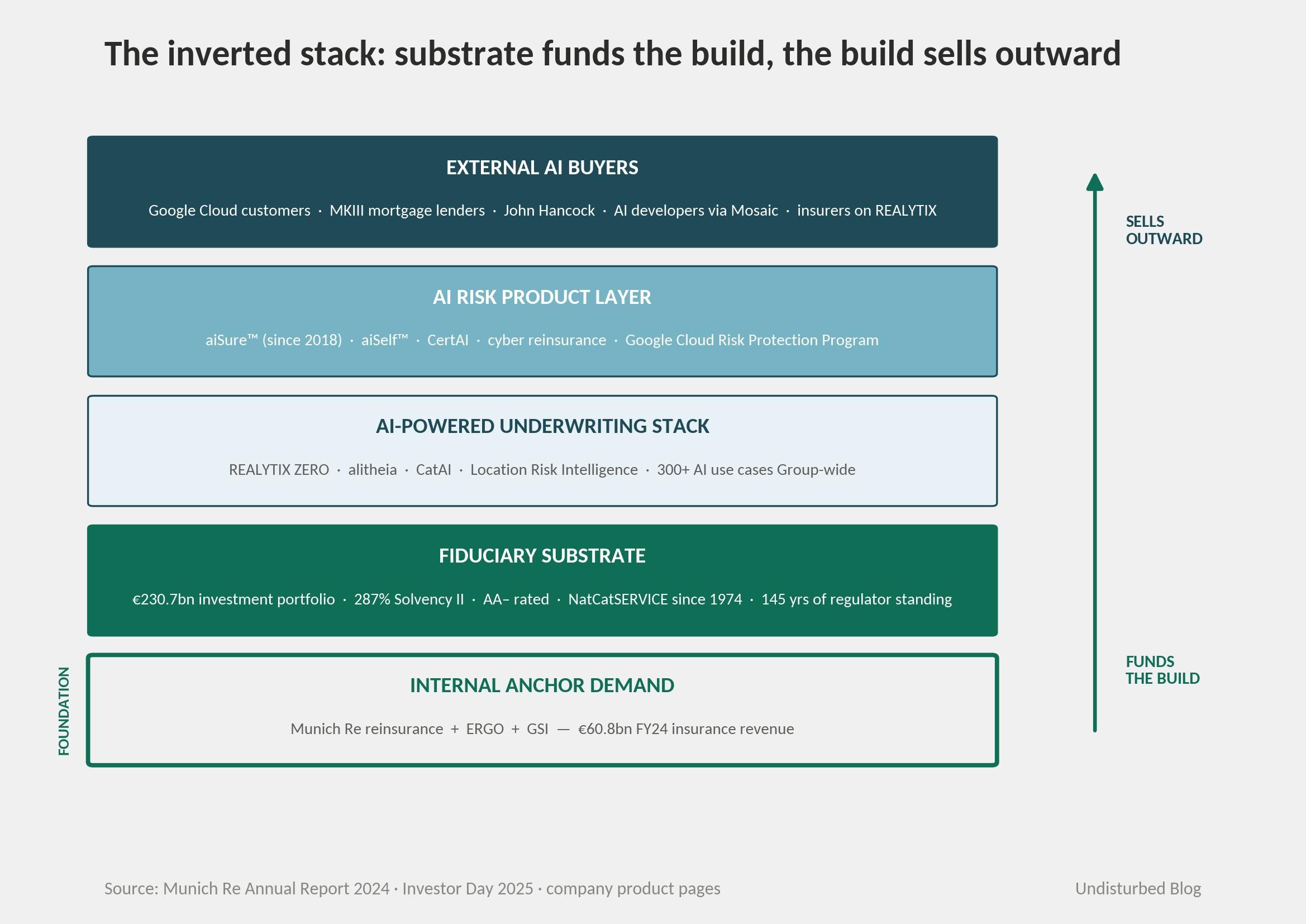

The strategy in one picture

The thing to notice is the direction of the arrows. Most fintech sells AI tools to enterprises. Most reinsurers sell capacity to primary insurers. Munich Re built the AI underwriting stack to price its own book first — and the same stack now sells policies on AI itself to enterprises deploying models in regulated environments. The internal anchor funded the substrate. What was built for internal use is now what the market buys. The inversion is the strategy.

How it actually works — three closed loops

Stack one layer on the next and what binds them are three closed loops. Each loop has the property that data flowing one way produces decisions flowing back the other way — without humans sitting in the middle of every transaction.

Loop 1: The internal-AI loop

Munich Re's underwriters submit risks into REALYTIX ZERO — a cloud-based, no-code/low-code platform now used by 50+ clients across 15+ countries with 4,000+ users on 25+ insurance products. The platform's generative AI CoPilot is Munich Re's self-described first production GenAI deployment. For life and health, alitheia delivers binding underwriting decisions within 48 hours in 75% of cases, pulling automated medical record summaries through Clareto. For catastrophe response, CatAI ingests post-disaster aerial imagery via a Google Cloud–co-developed pipeline that Google reports runs at nearly 19× the cost-to-performance of traditional methods. Every decision these systems make is also a labeled training example for the next decision. The closed loop is that loss data Munich Re generates from its own underwriting is precisely the signal that prices its next underwriting cycle.

Loop 2: The AI-as-product loop

Since 2018 — well before "LLM" entered mainstream business conversation — Munich Re has written performance guarantees on AI models themselves through aiSure™. The first cover for a Large Language Model went out in 2019. The structure is closer to a parametric contract than to traditional indemnity: policies trigger on measurable model-performance deviations (error rates above thresholds, hallucinations, calibration drift, fairness violations). Head of Insure AI Michael Berger has been explicit about the methodology — the math is reinsurance math, transferred. The team applies "the fluctuation of the loss-ratio based on the pricing or risk assessment of the primary insurer" and extends that framework to AI models. The closed loop here is the one Berger keeps emphasizing: each AI policy generates loss data that prices the next one — and because the train/test paradigm lets Munich Re infer error distributions before claims materialize, the loop closes faster than for any traditional line.

Loop 3: The partner-ecosystem loop

In April 2025, Google Cloud expanded its Risk Protection Program — for which Munich Re has been a founding partner since launch — into more than 30 EMEA markets, adding Beazley and Chubb. The program embeds insurance into Google Cloud's customer journey: enterprises moving regulated workloads onto Google Cloud can get tailored cyber and Affirmative AI coverage as part of the platform's go-to-market. Mosaic Insurance distributes aiSure to AI developers at limits up to $15m initial. Sixfold integrated its agentic AI underwriting workflow into REALYTIX ZERO in April 2026. The closed loop: the partner channel produces real-world AI deployment data — which Munich Re uses both to price its own AI policies and to pre-empt accumulation risk on foundation models the partners themselves rely on.

What ties the three loops together is something that doesn't appear on any architecture diagram: the underwriters who design the systems are the same underwriters who price the book. REALYTIX ZERO's product head Florian Niklas describes the platform as by underwriters, for underwriters. The platform code is replicable. The bilingual culture is not.

The numbers

FY 2024 insurance revenue: €60.83bn (up from €57.88bn). Net result: €5.67bn (+23% year-over-year). Return on equity: 18.2%. Property-casualty reinsurance combined ratio: 82.4% — and on AM Best's normalized non-life basis, 77.3%, the best in the global top five. Solvency II ratio: 287% including transitionals. Investment portfolio carrying amount: €230.7bn. FY 2025 closed at a record €6.1bn net result. Total shareholder return over the Ambition 2025 cycle (2021–2025): 171%.

For comparison, Swiss Re overtook Munich Re for the #1 IFRS-17 spot in 2024 ($43.1bn vs $42.8bn gross premiums written). The interesting reading is not the rank — it is that Munich Re consciously cut premium volume by roughly 8% at January 2025 renewals while delivering the cycle's best combined ratio. The discipline is the signal.

The program owner for the AI strategy is on the record: Wenning's 2024 letter to shareholders cites "over 300 AI use cases" identified, launched, or implemented Group-wide. ERGO GPT had reached 28,000 employees and 1.5 million prompts by May 2024, with €130m of cumulative spend on the generative AI platform planned by 2030. REALYTIX ZERO: 50+ clients, 15+ countries, 4,000+ users. alitheia: under 48 hours in 75% of cases. NatCatSERVICE: 37,000 records, 1,000 events ingested per year, since 1974. Location Risk Intelligence: more than 50 million risk assessments per year.

On the AI risk product line — and this is where the article has to be honest — the publicly disclosed numbers are thin. The Mosaic-aiSure facility lists $15m initial per developer. The Financial Times reports MKIII mortgage AI cover at "millions in premium for tens of millions of cover, enabling hundreds of millions in home loans" — but with no precise figure. Munich Re does not publish aiSure premium volume or loss ratio.

A reader trained on SaaS ARR will look at the aiSure line, see no disclosed premium, and conclude the product is immaterial. That misreads the strategy. aiSure's commercial role is not to generate premium volume — it is to be the trust signal that allows hundreds of billions of customer-facing AI revenue to be underwritten elsewhere in the Group's book. Munich Re collects rent through three channels: AI-exposed cyber line cession (cyber is a $15.3bn global market today, projected $32bn+ by 2030), Location Risk Intelligence subscription revenue (50m+ assessments/yr), and REALYTIX ZERO platform fees. The aiSure policy is the passport that lets clients sit on Munich Re's substrate. The right metric is the implicit cession from AI-exposed lines into the reinsurance book — which the company has, very deliberately, not broken out.

The Ambition 2030 strategy (10–11 December 2025) targets €600m of cost savings by 2030, of which €200m by 2026, with AI explicitly named as the primary lever. Insurance revenue target for 2026: €64bn. Net profit target for 2026: €6.3bn. Group RoE through 2030: above 18%. The program owners are now named at the top — Christoph Jurecka took over as CEO on 1 January 2026, Andrew Buchanan became CFO, and Robin Johnson was appointed to a newly created Chief Technology Officer Board seat on 1 August 2025 — the first time in the company's 145 years that technology sits at Board level.

Is AI a norm inside Munich Re?

The cheap version of this test counts use cases. Munich Re passes that test trivially — 300+ Group-wide, by the CEO's own attestation in the annual report. The harder version asks whether AI has been absorbed into the capital model itself — whether the actuarial functions that drive Solvency II reporting now treat AI-derived inputs as canonical. The evidence is that they do. alitheia issues binding underwriting decisions. REALYTIX ZERO writes policies without manual review. CatAI feeds directly into post-disaster claims triage. These are not pilots in a sandbox; they are production systems whose outputs feed regulatory disclosure.

Three structural facts are worth pulling out, because each is the kind of move a company makes when it has decided AI is permanent rather than experimental.

The first is the Board-level CTO seat. Wenning's successor team — Jurecka as CEO, Buchanan as CFO, Johnson as CTO — was assembled in July 2025, well before the Ambition 2030 announcement. Until that point, technology had reported into the CFO or sat under regional CIOs. Creating a Group CTO position is the kind of decision that signals AI is no longer a project but a function. Johnson's foreword to the 2026 Tech Trend Radar puts it cleanly: "Technology creates value only when embedded in strong governance, clear accountability and ethical frameworks." The mantra is institutional, not personal.

The second is that Wenning's exit was not a disruption to the AI agenda. Ambition 2030 was launched jointly by Wenning and Jurecka, with AI named in the strategy document rather than in CEO-personal commentary. The €600m savings target sits in the strategy itself. Jurecka's framing line — "we will reduce complexity and combine our market-leading know-how with artificial intelligence to boost our speed" — is now the official voice. The agenda is institution-owned.

The third is harder. ERGO — Munich Re's primary insurance arm, roughly 37,000 of the Group's 44,000 employees — announced in February 2026 that it will reduce headcount by roughly 1,000 jobs by 2030, almost entirely via AI absorption. The mechanism is voluntary: about 200 departures per year through attrition, no forced layoffs, and a 500-person Reskilling Academy for employees whose roles dissolve. This is not Munich Re-specific — Allianz Partners announced 1,800 job cuts (~8% of staff) in November 2025 via similar automation. But it is what AI normalization actually costs at scale. The Group's official framing is that the savings flow through to ROE and shareholder returns. The unofficial framing is that 1,000 ERGO households absorb the cost.

The operational-substrate pattern has a social-cost dimension that strategy decks mostly suppress: when the substrate gets productized, the labor that previously served as the substrate's interface gets restructured. The 1,000 ERGO jobs are the version Munich Re has chosen to be transparent about. The harder question — for any company adopting this pattern — is whether the Reskilling Academy is a serious institution or a press release. The honest answer is probably we will know in 2028. Either way, the social cost is part of the pattern, not a side effect to be quietly netted out.

Why this answer fits Munich Re

A few things had to be true at the same time for this pattern to work — and the things that had to be true are not things competitors can put in next quarter's plan.

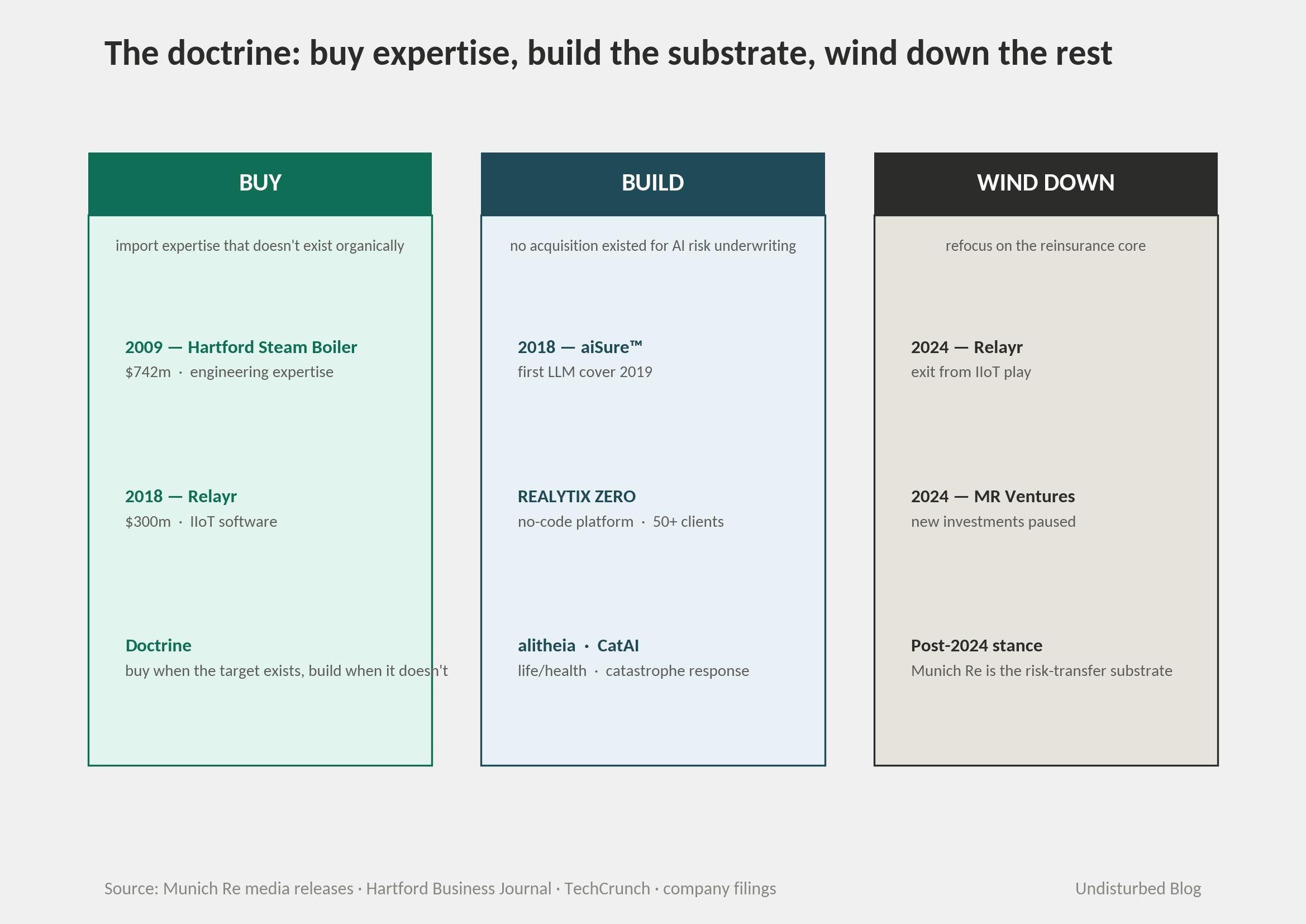

The actuarial DNA. Munich Re was founded on 3 April 1880 by Carl Thieme, Wilhelm von Finck, and Theodor von Cramer-Klett to be the world's first independent reinsurer — separate from primary insurers, internationally diversified by design. The company paid claims while competitors defaulted on the 1906 San Francisco earthquake. It founded a Geo Risks Research department and the NatCatSERVICE database in 1974, recognizing climate change as a strategic risk before the IPCC existed. The "writing what others won't" doctrine is older than the modern category of reinsurance itself. The line from 1906 to 2018 — when aiSure shipped — is one continuous methodology.

The make-or-buy doctrine. Munich Re acquired Hartford Steam Boiler in 2009 for $742m to import engineering expertise it didn't have organically. It bought Relayr in 2018 for $300m to import IIoT software. It built REALYTIX ZERO, alitheia, CatAI, and aiSure internally — because no acquisition target existed for "AI risk underwriting" in 2018. Then, in 2024–2025, Munich Re did something interesting: it wound down Relayr, paused new Munich Re Ventures investments, and refocused on the reinsurance core. The post-2024 stance is unambiguous — Munich Re is no longer hedging its identity as a tech/IoT play. It has resolved to be the risk-transfer substrate and to outsource the tech stack to partners.

Why other reinsurers can't simply copy this. Swiss Re is pursuing a Palantir-anchored agentic platform under its "Built to Lead" strategy. Hannover Re is pursuing a platform/marketplace approach. Both are coherent. Neither has assembled the simultaneous combination of (1) a vertically integrated AI underwriting platform, (2) an externally facing AI risk product dating to 2018, (3) a hyperscaler channel partnership, (4) a cyber + AI loss data warehouse, and (5) the best non-life combined ratio in the top five — all anchored by AA- capital. The pieces are individually replicable. The stack is not.

The architecture is transferable. The activation energy is not. Cloud-based no-code underwriting platforms, parametric AI performance contracts, agentic-AI submission intake — these are all replicable in eighteen months by any well-capitalized reinsurer. What another reinsurer cannot replicate in any planning horizon is 145 years of continuous regulator standing, 51 years of NatCatSERVICE data cited in IPCC reports, the AA- rating that lets clients lean tens of billions of regulated AI exposure onto your balance sheet, and the cultural fluency of underwriters who can price both a cat bond and a hallucination policy. The architecture is the build. The activation energy is the company. Munich Re's strategy works because the company was already in place when the strategy showed up.

Where it goes next

Three vectors and three risks.

The first vector is agentic AI. In a joint 2025 statement with Chubb, Munich Re warned that autonomous AI fundamentally alters the cyber threat surface — collapsing time-to-compromise to minutes. Berger's framing from the National Insurance Conference of Canada 2025 is operative: "When AI has a real-world impact, it comes with real-world risk." If agents take real-world actions on behalf of companies, agents become insurable entities in their own right — not subsets of existing E&O. Munich Re is positioned to be the underwriter of record for that category before it has a name.

The second is foundation-model accumulation. Berger has been candid that this is the structural concern — a single GPT- or Claude-class model update could simultaneously degrade thousands of downstream applications. Munich Re's stated approach is to limit aggregate exposure on individual foundation models and diversify across providers. The Google Cloud partnership is the most advanced public example; the test in 2026–2028 is whether similar partnerships emerge with the AWS or Azure equivalents.

The third is climate × AI. NatCatSERVICE meeting AI-enhanced wildfire and flood models is the natural extension — Wildfire HD Edition already delivers 30-meter-resolution risk maps; the LA wildfires of January 2025 cost the Group ~€1.2bn and the industry an estimated $40bn insured.

The risks are real. Hyperscalers have the balance sheets to self-insure AI errors at scale, and the Google RPP partnership is double-edged — it could evolve toward Google as substrate, Munich Re as commodity capacity. ILS securitization of AI risk would shrink reinsurer rent — Beazley already issued a $510m cyber cat bond program. And U.S. state regulators have approved most carrier requests to exclude AI losses from standard policies, which is enabling for Munich Re today but could shift if regulators decide AI risk is systemically uninsurable. Munich Re itself doesn't draw the strategy as "operational substrate as sovereign product." The article does. But the company's own Ambition 2030 language is closer than a reader might expect: "first-in-class, AI-supported expertise to seize business opportunities." The product, in the company's own words, is the expertise — and the expertise is what sits on the substrate.

Conditions under which the pattern replicates

The Munich Re case looks idiosyncratic at first read — 145 years of actuarial DNA do not transfer. But the structure underneath generalizes. Companies that successfully productize an operational substrate tend to share four conditions, and the absence of any one of them is usually fatal.

A unified internal substrate, not ten fragmented stacks. The pattern does not work without internal consolidation first. Munich Re built one underwriting platform that prices its own book before that platform sold a single external policy. Most companies operate ten platforms and have no substrate; the productization conversation is premature.

A measurable cost or revenue number tied to AI, defensible to a CFO. Munich Re's €600m AI-driven 2030 cost-savings target was published with a date attached. Rent is collected through three channels — cyber cession, Location Risk Intelligence subscriptions, REALYTIX licensing — none of which require explaining what AI is. Crisp means a number a skeptic can audit. Companies whose AI line item lives inside "digital transformation" cannot pass this test.

AI as a permanent function, not a project. The diagnostic is the count of board-level seats a company has created for it, and whether the strategy document names AI as a line item or hides it inside broader transformation language. Munich Re created a CTO seat after 145 years of operation — that decision is not made for a project that might fail next year.

DNA, doctrine, and inflection point in alignment. The pattern only works when the operating culture, the make-or-buy doctrine, and the regulatory moment all line up at the same time. Munich Re's three did. Most companies' three do not. The interesting diagnostic question is not whether they line up today but which of the three the company can actually move.

References