Kering

13

min read

On April 16, 2026, Kering walked the analyst community in Florence through a deck called ReconKering and described, in some detail, a "Group Platform" of five hubs — a unified client base, a tech foundation built on cloud-native systems and agentic AI, an industry hub, a sustainability hub, a support layer. The deck was the first major public artifact from Luca de Meo, the ex-Renault CEO who had arrived seven months earlier as the first non-Pinault to run the group. It described, with unusual frankness, the data substrate the group does not yet have but intends to build.

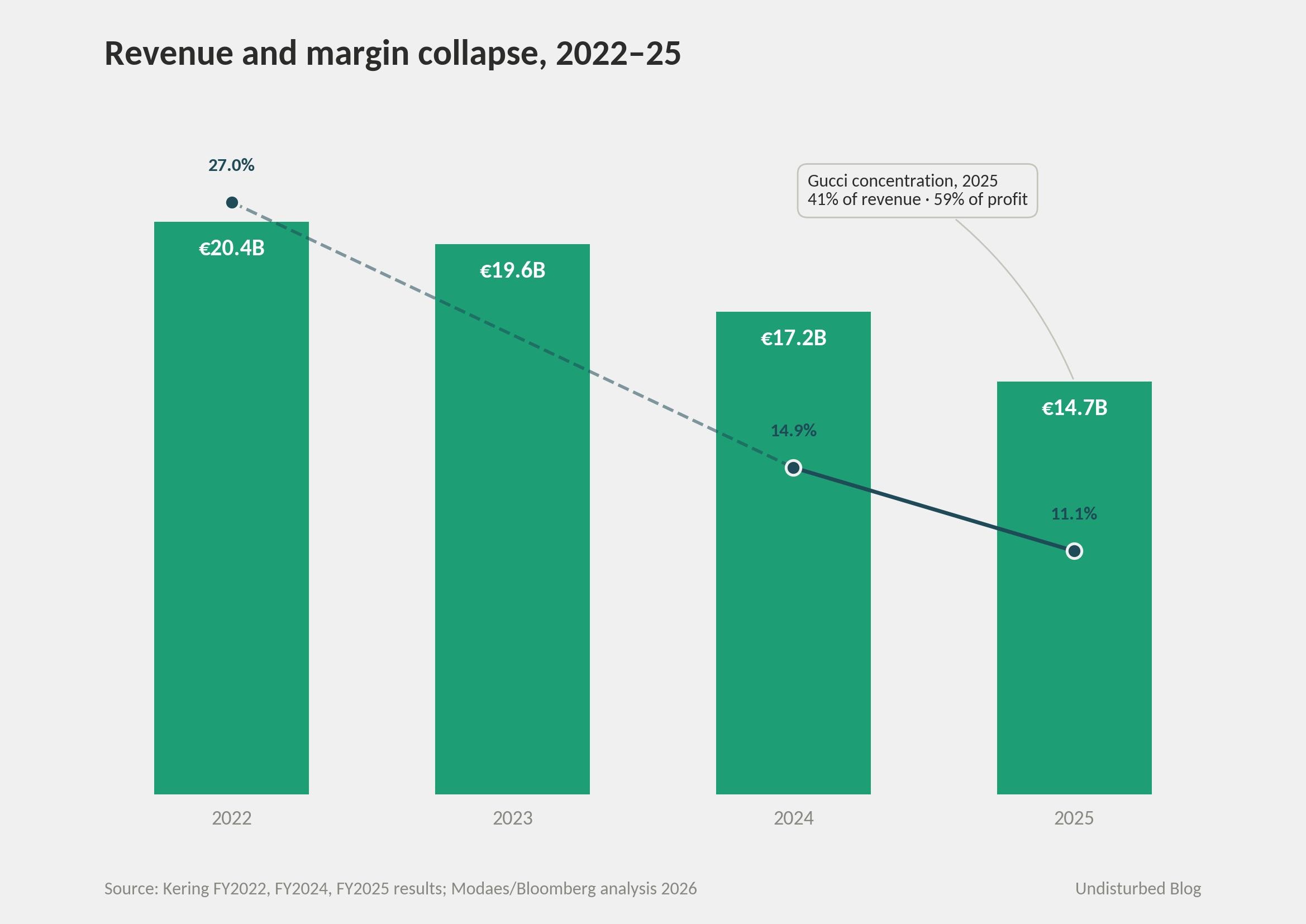

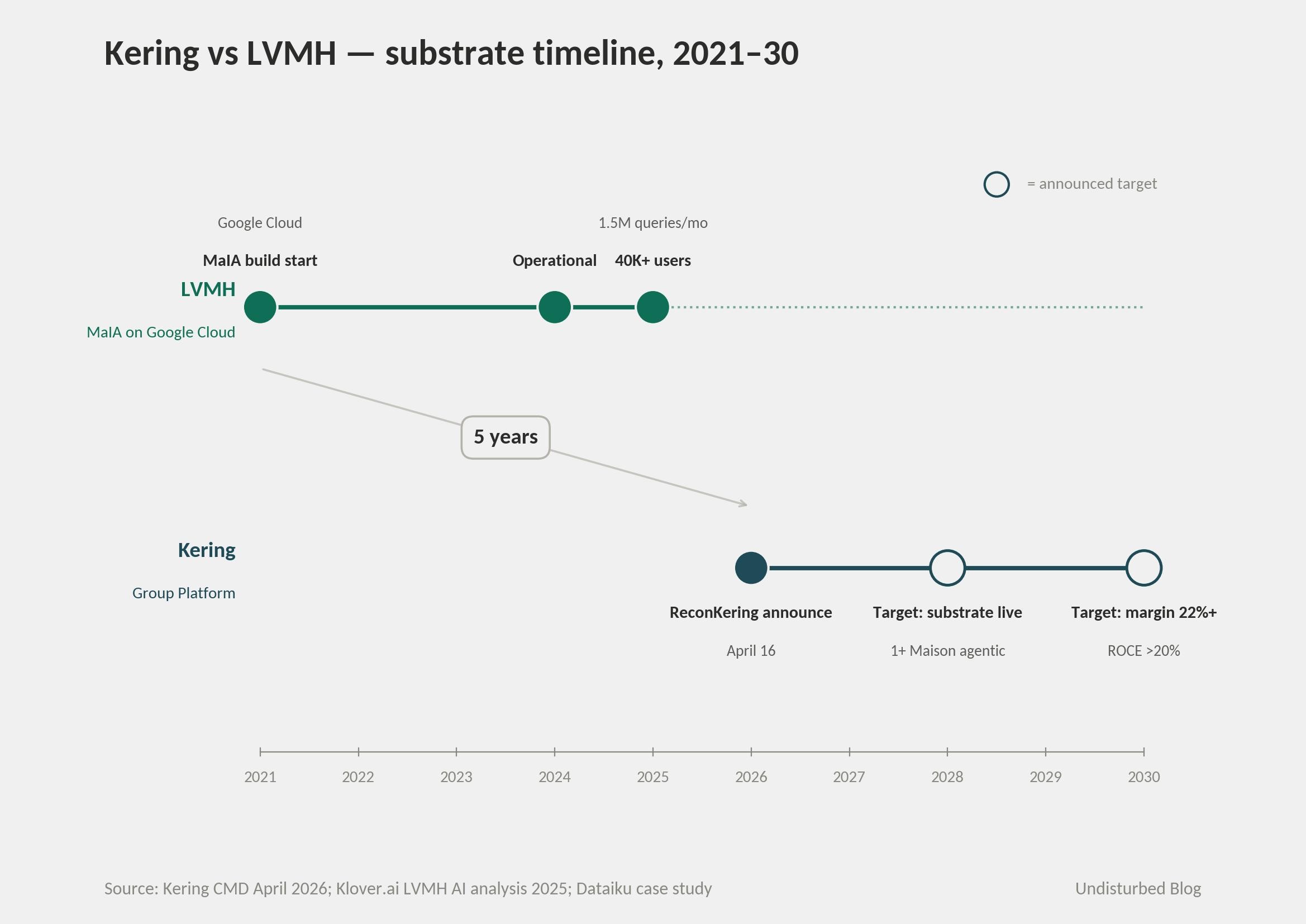

Kering closed 2025 with €14.7B in revenue, down 13% year-on-year and roughly 28% from the 2022 peak. Gucci accounted for 41% of revenue and 59% of operating profit. The group's data function — about 200 specialists in a workforce of 43,731 — has no publicly named Chief AI Officer and no group-wide internal AI assistant disclosure. LVMH, the comparable peer, started building its MaIA assistant on Google Cloud in 2021 and by 2025 was serving over 40,000 employees with more than 1.5 million queries a month. The architecture Kering is announcing in 2026 is the architecture LVMH has been operating since 2024 — Kering is roughly five years behind, and the deck says so openly.

The pattern is straightforward to name. Architecture must precede AI. Substrate lag compounds: once a peer has five years of unified-data flywheel, no amount of AI tooling closes the gap. Only a rebuild does. Kering is doing the rebuild, in public, from behind.

The Substrate Built Late

The pattern at issue here is the one where brand, legal, data, and doctrine move together as a single substrate before AI workloads land on top. DHL is the canonical example — a logistics group that consolidated its data layer first, then let AI pricing, routing, and customer-service work compound on top. The pattern's whole insight is sequencing: get the substrate consolidated, then build.

The same pattern run on a five-year delay looks identical in architecture but different in consequence. The work is the same. The peer comparison is the problem.

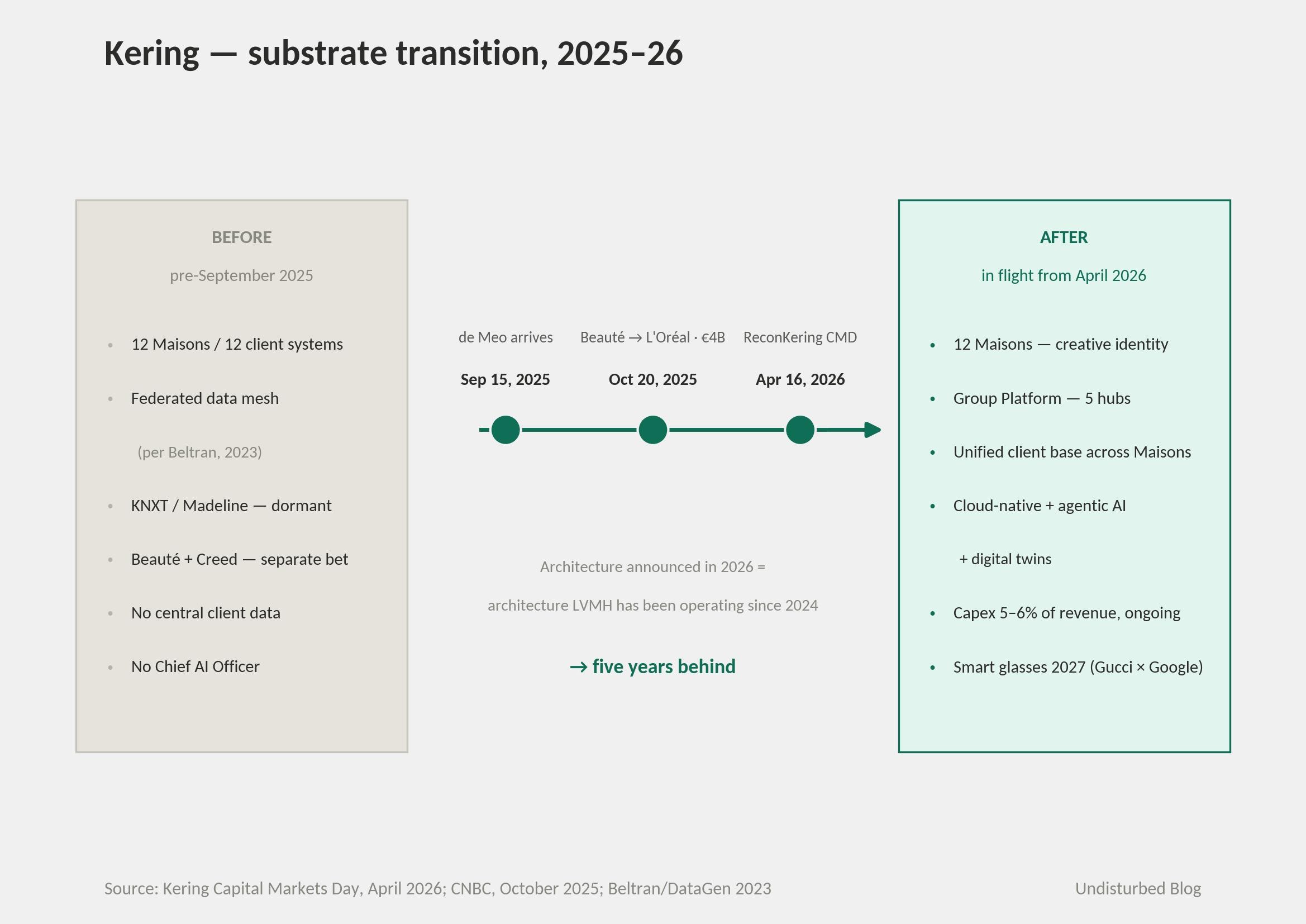

That is what makes Kering interesting in 2026. The Capital Markets Day deck describes a Group Platform of five hubs, two of which read almost as a checklist of what LVMH built between 2021 and 2024: a unified client base "consolidating proprietary and external data," and a tech foundation "powered by cloud-native systems, agentic AI and next-generation digital twins." None of the four layers run yet. This is substrate work happening in 2026, in the open, with the press deck as the timestamp.

The honest claim is not that Kering is doing AI. Kering is building the substrate that AI will eventually run on, and is doing it from behind.

It is worth being precise about why this is a substrate-build case rather than a four-layer-architecture case. Kering's announced architecture is shaped like the four-layer pattern — five hubs running on different clocks, agentic interface on top, physical and supply substrate at the bottom. But the four-layer pattern, as it shows up at FedEx and JPMorgan, depends on the bottom layers already being there as data. Kering's data layer is mid-pour. ReconKering reverses Kering's own 2023 doctrine of a federated data mesh and replaces it with consolidation. That is the substrate move, not the four-layer move. The four-layer architecture is where Kering wants to be in 2030. The work in 2026 is the substrate.

The Strategy in One Picture

The transition has a date and a name. September 15, 2025: de Meo, ex-Renault, arrived as the first non-Pinault CEO and the first time chair and CEO had been split since the family took control. October 20, 2025: the Kering Beauté experiment — bought as a vertical-integration platform in February 2023, anchored by the €3.5B Creed acquisition that July — was sold whole to L'Oréal for €4B. By the April 16 Capital Markets Day, the brand and legal layer had been simplified, and the substrate work could begin.

What is striking is what was missing before. There was no Chief Data Officer. There was no shared client identity across Maisons. The 2023 architecture, articulated by Yannick Beltran on a French data-engineering podcast, was an explicit data mesh — federated by design, each Maison owning its own data products, with a small central team of around 200 in a workforce of 47,000. That was a defensible architecture for an autonomous-Maison group. It is not the architecture an agentic-AI consumer interface will run on.

How It Actually Works — Three Loops

A substrate-lag case requires honesty about where AI runs today, not where it will run in 2030. Three loops at Kering are real enough to describe. Two predate the substrate work. One depends on it.

Loop one: EP&L → sourcing → production.

Kering has run an Environmental Profit & Loss account since 2011, longer than any luxury peer. The methodology was open-sourced in 2015 and continually expanded; it covers raw materials, manufacturing, retail, product use, and end-of-life, and quantifies impact in monetary terms. By 2021, Marie-Claire Daveu, the Chief Sustainability Officer, was describing AI pilots inside the EP&L for raw-material optimization and circularity. The loop is real and closes: sourcing decisions feed back into the next year's EP&L numbers. But it is supply-chain-only. It does not touch the customer. It does not touch the creative tier. And — interestingly — Kering gives the methodology away for free, which keeps the loop honest but caps its strategic value.

Loop two: Salesforce → clienteling → reorder, at Gucci.

Since 2022, Gucci has run client services and clienteling on Salesforce, with Vasilis Dimitropoulos as the named program owner — VP Global Client Services & Product Care. Agentforce came in later. In parallel, the Boutté-era clienteling app Luce is cited by the Business of Fashion / McKinsey State of Fashion 2025 report as having boosted average order values by 15–20%. The loop closes: store associate sees client history, makes a recommendation, the system measures whether the recommendation worked, the next recommendation gets better. But the loop is narrow — it runs at Gucci, not group-wide, and the data does not yet flow back to a Maison-shared client base.

Loop three: Client hub → S&OP → inventory.

This is the announced loop, and the one that requires the substrate. Carlo Mocci, the new Chief Client Officer (effective May 4, 2026, ex-Amazon Europe), owns the Client hub. The hub will consolidate client data across Maisons, feed it into sales-and-operations planning, and target a €1B inventory reduction by year-end 2026 with stock at less than 20% of sales. None of this works without the unified client base the deck announces. The honest statement is that this loop is not closed yet. It cannot be — the substrate is mid-build.

The pattern across the three loops is what matters. The mature loops are pre-substrate and narrow. The substrate-required loop is the prize. The activation problem is the gap between them.

The Numbers

The numbers are the engine. They tell two stories at once: Kering's collapse, and why the substrate became unavoidable.

Revenue trajectory: €20.4B in 2022, the all-time peak. €19.6B in 2023. €17.2B in 2024. €14.7B in 2025, down 13% year-on-year and roughly 28% from peak. Recurring operating margin: 27% in 2022, 14.9% in 2024, 11.1% in 2025. Net income: a thin €72M, after Beauté disposal adjustments — effectively a wash year. The CMD target is to more than double the 11.1% margin "mid-term."

Gucci is the concentration risk. 41% of group revenue, 59% of group operating profit in 2025. The brand's revenue went from a 2022 peak near €10.5B to €5.99B in 2025, a 22% YoY decline on top of a 23% decline the year before. Gucci's recurring operating income fell from roughly €3.7B at peak to €966M in 2025 — a 74% drop in three years.

It is tempting to read 41/59 as a Gucci problem that AI can solve. The numbers do not say that. They say the group's profit pool is one Maison's success or failure away from disappearing entirely, and that no other Maison has been built up enough to absorb the volatility. The substrate question is not "can AI fix Gucci." It is whether a unified data layer can let the other 11 Maisons learn from Gucci faster than Gucci can decline. That is a different problem. It is also the one ReconKering is actually trying to solve.

The data infrastructure numbers explain why the substrate work is happening in the open. About 200 data experts across the group, in a workforce that closed 2025 at 43,731 employees (down from roughly 47,000 in 2023). No publicly named Chief AI Officer. No publicly named Chief Data Officer at the executive committee level. No internal AI assistant disclosure comparable to LVMH's MaIA, which serves 40,000+ users with over 1.5M queries per month. The only named program owner with a public role is at the Maison, not the group: Vasilis Dimitropoulos at Gucci, on Salesforce. There is no group-level equivalent to point to.

Two forward numbers anchor the substrate bet. Capex stepping to 5–6% of revenue, ongoing — roughly double the historical luxury norm of 1% R&D, although not earmarked specifically as AI spend. And Gucci-Google smart glasses launching in 2027 through Kering Eyewear's May 2025 Android XR partnership, putting Kering directly against EssilorLuxottica/Meta Ray-Ban in the most-watched AI-consumer-device category.

Whether AI Has Become a Norm at Kering

The standard test for whether a pattern has become a norm is whether it survives executive succession, shows up in how people work, and has shared doctrine. The Kering answer to that test has to be written in the negative. AI is not yet a norm at Kering. That is the honest read of where the substrate work stands.

The evidence is consistent. KNXT, the Web3 sandbox that briefly launched Madeline in April 2023 as "the first AI personal shopper" powered by ChatGPT, went into indefinite "maintenance" by 2024. There was no announcement. There was no follow-on. A norm-forming program leaves a trail; KNXT left a maintenance page. Kering's 2023 articulated data architecture was a federated mesh — the right call for autonomous Maisons in 2023, the wrong call for an agentic-AI interface in 2026. ReconKering is a deck dated April 16, 2026. The hubs do not yet have public heads. The Technology hub, which the deck describes as "powered by cloud-native systems, agentic AI and next-generation digital twins," has no announced CTO as of May 2026.

The comparison to LVMH is unflattering and useful. LVMH started building MaIA on Google Cloud in 2021. By 2025 it served 40,000+ employees with 1.5M+ monthly queries. MaIA is not just a tool — it is the artifact that proves AI is a norm. Kering does not have one yet, and is not pretending it does.

The succession question — whether the pattern survives the CEO who started it — is harder than usual at Kering, because the pattern just started, and de Meo's previous AI bet at Renault is a cautionary tale.

At Renault, de Meo hired Luc Julia (the Siri co-creator) as Chief Scientific Officer for AI, ran Software République, and spun up Ampere as an EV-and-software pure-play with himself as CEO from June 2023. The Ampere IPO was abandoned in early 2024. His successor, François Provost, folded Ampere back into Renault in January 2026 — within six months of de Meo's exit. The architecture survived 18 months, then unbuilt itself. ReconKering is doctrinally one CEO's bet. The activation question is whether the Pinault family's patient capital, not de Meo's tenure, becomes the thing that carries it. Architecture transfers to successors. Activation energy mostly does not.

Why This Answer, Why Now, Why This Group

The interesting question is not why Kering is doing this. Every luxury group will eventually do something like this. The interesting question is why now, why this group, and why this CEO.

The why-now is straightforward and brutal. Gucci's collapse forced the architectural conversation. Without the 2023–25 revenue decline, Kering could have continued its data-mesh doctrine indefinitely. The collapse made the absence of a unified client base into a board-level liability. The L'Oréal Beauté exit in October 2025 — €4B for a 2.5-year-old vertical-integration experiment, with L'Oréal becoming the long-term licensee for 50 years — cleared the brand-and-legal layer that Kering needed simpler before pouring substrate. By April 2026 the path was open.

The why-this-group is consistency of doctrine. Kering's signature is the Pinault patient-capital structure, with Artémis holding roughly 42% across generations, and a multi-decade pattern of simplification. The 2018 Puma demerger crystallized "100% luxury." The 2025 Beauté sale crystallized "luxury fashion and goods, not licensing platforms." ReconKering crystallizes "centralized substrate, autonomous creative." The Pinault doctrine has always been: simplify the structure to fund the next bet. The substrate is the next bet.

The why-this-CEO is the most honest part. De Meo at Renault was the most explicitly tech-forward auto CEO in Europe — Luc Julia, Software République, Ampere. He arrives at Kering with a "tech-company-with-luxury-houses" mantra openly modeled on his "tech-company-with-cars" mantra at Renault. Whether that translates is the open question.

There is a final piece, and it is the EP&L. Since 2011, Kering has been the only luxury group running a continuously updated, methodology-published, supply-chain-deep environmental account. The EP&L is not AI. It is a 14-year discipline of treating supply-chain data as a first-class asset. The closest analog among comparable groups is Tesco's Clubcard discipline — a long-running data culture that the AI era could productize on top of. Kering's EP&L did not productize externally; it was given away. But it built the only group-wide data muscle Kering currently has. ReconKering, read charitably, is an attempt to extend that muscle from supply chain to client.

The wider pattern worth naming here is that France produces strategic architectures at a higher rate than it activates them. The Software République is one example. The CMA CGM "AI factory" announcement in 2024 is another. The Mistral national-champion narrative is a third. Kering's ReconKering deck is doctrinally excellent — the five hubs are correctly named, the clocks are correctly separated, the comparable peer is correctly identified as LVMH. None of that is the activation. Activation is a Chief AI Officer with a budget, an internal MaIA-equivalent that 40,000 people open every morning, and a successor who will not unbuild it. Architecture transfers across borders. Activation energy mostly stays where it was generated.

Where It Goes Next

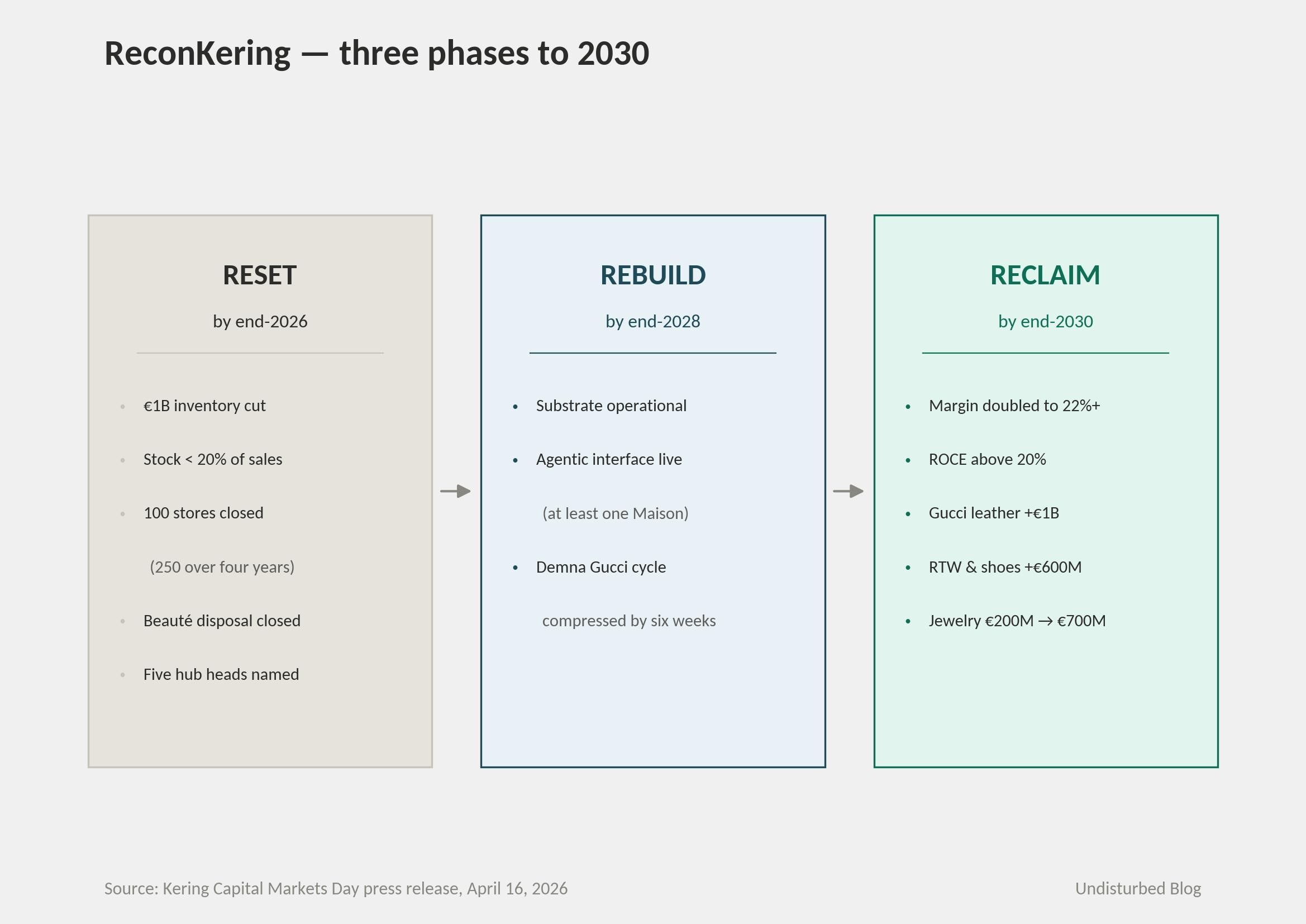

ReconKering names three phases. Reset, by the end of 2026: €1B inventory cut, 100 stores closed (250 over four years), Beauté disposal closed, hub heads named. Rebuild, by the end of 2028: substrate operational, agentic interface live for at least one Maison, Demna's Gucci collection cycle compressed by six weeks already evident in sell-through. Reclaim, by the end of 2030: margin doubled from 11.1%, return on capital employed above 20%, Gucci leather goods +€1B, ready-to-wear and shoes +€600M, jewelry from €200M to €700M.

Three forward bets are worth watching specifically because they tell the activation story. The Gucci-Google smart glasses, launching 2027, are the clearest test of whether the Eyewear-plus-Android-XR partnership becomes a brand-layer-on-rented-OS move — owning the brand layer while renting the operating system. The "House of Dreams" investment vehicle, trademarked in France in October 2025 and structurally echoing de Meo's Renault "Mobilize" arm, is positioned to take stakes in emerging brands and culture-led luxury concepts in China and India; it is a venture-portfolio answer to over-concentration on Gucci. The HModa industrial joint venture announced at CMD is the proof-of-concept for the Industry hub — vertical capacity for Italian leather goods manufacturing, structured so Kering's Maisons share the substrate without sharing the creative.

What cannot yet be said is whether activation matches architecture. The Group Platform deck dates from mid-April 2026. The Technology hub does not have a public head. The Chief AI Officer position has not been created. The capex commitment is real but not earmarked. The standard against which all of this will be judged is LVMH's MaIA — not because LVMH is the only model, but because LVMH is the comparable, and the comparable already exists.

Kering's 2030 case is that five years of disciplined substrate work, plus EP&L DNA, plus Pinault patient capital, plus de Meo's tech-company instincts, will compound faster than LVMH's lead. Kering's 2030 risk is that the lag itself is the strategic problem, that activation energy stays in Renault (where it built and unbuilt), and that the patient capital starts running out of patience.

Four Diagnostic Questions This Case Raises

The point of the substrate-lag case is not to prescribe what Kering should have done. It is to surface the four diagnostic questions that distinguish a group that has built a substrate from one that is mid-pour.

The first is whether a group's data is actually on a unified substrate, or whether the AI strategy is running on a federated mesh that the organization has stopped questioning. Federated was the right answer in 2018. It is not the right answer for an agentic interface in 2026.

The second is whether AI surfaces in the bottom line as a company-owned number rather than a third-party consulting estimate. Programs whose only quotable result was sourced from a McKinsey or BCG report tend not to be what the executive team thinks they are.

The third is whether there is a named owner of AI at the group level, with a budget and a roadmap that will survive the CEO who hired them. Where the answer is "the CEO," the pattern has not yet become a norm — it remains a personal bet, with the activation horizon bounded by the CEO's tenure.

The fourth is the why-now question. Substrate work is expensive and it requires the brand-and-legal layer to be simplified first. Groups that pour substrate without first clearing acquisitions, divestitures, and legacy commitments end up rebuilding the substrate twice. The case-shaped answer to why-now is "we waited for the architecture to clarify and the legacy commitments to clear." The activation-shaped answer is a date, a budget, and a hire.

These are the questions Kering's case puts on the table. Whether Kering itself answers them in the affirmative by 2030 is the open bet ReconKering takes.

References